Many or all of the products featured here are from our partners who compensate us. This may influence which products we write about and where and how the product appears on a page. However, this does not influence our evaluations.

A fair credit score ranges between 580 to 669 for FICO® Scores and 601 to 660 for VantageScore®.

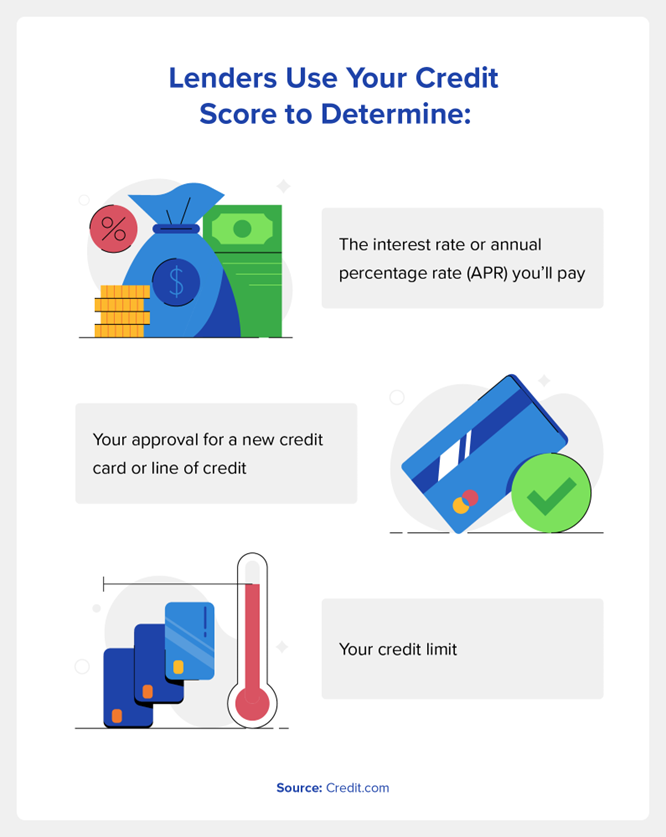

How often do you think about your credit score? Perhaps only when it’s time to make a big financial decision like applying for a mortgage, a car loan, or a new credit card. At this point, your credit score can have major implications for your wallet.

A fair credit score means your creditworthiness is somewhere in the middle. It’s better than poor, but it can cost you higher interest rates and worse terms for any loans and credit cards for which you are approved. It could also mean not getting approved for loans or credit cards altogether.

While we’ll explain what you can expect with fair credit, the gain or loss of a few points on your fair score can make a world of difference in your personal finances. To help you get the best terms possible, we’ll also offer tips on what you can do to improve your credit score.

The most commonly used VantageScore® 3.0 and FICO® score models use a credit score range of 300 to 850. For each model, 300 is the lowest credit score, and 850 is the highest. A fair credit score is considered between 650 to 699 for VantageScore 3.0 and 580 to 699 for FICO scoring models.

Here is a full breakdown of scores for the VantageScore and FICO scoring models:

VantageScore®

Rating

FICO® Score

Rating

781-850

Excellent

800-850

Exceptional

661-780

Good

740-799

Very Good

601-660

Fair

670-739

Good

500-600

Poor

580-669

Fair

300-499

Very Poor

300-579

Poor

These models use similar criteria to determine credit scores, but they weigh each factor differently. Your score may vary depending on the model you use as a result.

FICO scores consider five major factors when determining your credit score:

Payment history (35%) is the biggest factor in determining your score. Your credit report card shows any missed and late payments and consistent on-time payments.

Debt usage (30%)—or credit utilization ratio—also makes up a big chunk of your score. Using your credit cards near their limits increases your ratio and card debt, which makes you a higher credit risk for lenders and issuers.

Credit age or credit history (15%)—includes your oldest accounts and closed accounts. The longer you’ve had credit, the better.

Credit mix (10%)—lenders like to see a combination of installment loans and revolving credit accounts (lines of credit such as credit cards) on your credit file.

New credit inquiries (10%)—hard inquiry requests from lenders or card issuers show up on your credit report and can hurt your score.

VantageScores use similar categories but don’t assign percentages. Instead, your credit score considers the “level of influence” of each category:

Payment history (extremely influential)

Credit utilization (highly influential)

Credit history and credit account mix (highly influential)

Debt owed (moderately influential)

Recent credit behavior (less influential)

Available credit (less influential)

Is a Fair Credit Score Average?

A fair credit score falls in the middle of credit scoring ranges and could be considered “average” credit. However, your score is below average if you have a fair credit rating.

What can you get with a fair credit score? A lot, actually. There are many different credit cards for fair credit, including rewards cards with lower rates. Remember, cards with the lowest annual percentage rates (APRs) may be out of your reach, but you can expect credit card rates around 22%.

Based on their APRs, fees, rewards, and other features, our top recommended credit cards for people with fair credit include:

No credit check to apply. Zero credit risk to apply!

Looking to build or rebuild your credit? 2/3 of cardholders receive a 48+ point improvement after making 3 on-time payments

Extend your $200 credit line by getting considered for an unsecured credit line increase after 6 months, no additional deposit required!

Get free monthly access to your FICO score in our mobile application

Build your credit history across 3 major credit reporting agencies: Experian, Equifax, and Transunion

Add to your mobile wallet and make purchases using Apple Pay, Samsung Pay and Google Pay

Fund your card with a low $200 refundable security deposit to get a $200 credit line

Apply in less than 5 minutes with our mobile first application

Choose the due date that fits your schedule with flexible payment dates

Join over 1.2 million cardholders who’ve used OpenSky to build their credit

Card Details +

Your Loan Options with Fair Credit

With a fair credit score, you’ll likely qualify for an auto loan but should expect pay between 10 to 18% in interest. On the plus side, there’s no need to limit your car shopping to a “buy here, pay here” type of car lot.

You should also qualify for most mortgages, where the minimum credit score required is 620. If you have a fair FICO score between 600 and 649, you can qualify for a loan through the Federal Housing Administration (FHA). These loans feature lower fees and interest rates to help those struggling to purchase homes.

To get an FHA loan, you need a minimum FICO score of 500, but that loan would come with a large down payment of 10%. If your credit score is 580 or higher, the minimum down payment is 3.5%.

Why Is a Good Credit Score Important?

As far as credit score guidelines go, the lower your credit score, the less access you have to credit. Alternatively, the higher your credit score, the lower your interest rate for credit card offers and loans.

Compared to 22% credit card rates for fair credit scores, good credit scores give you access to cards with rates around 20%. Credit card interest rates are around 14% for those with excellent credit.

The biggest benefit of a good credit score is access to lower interest rates on loans. If you want an auto loan, for example, raising your score to the good or excellent range might help you qualify for lower rates.

Similarly, mortgage interest rates decrease as your credit score increases.

How to Improve Fair Credit

Improving your credit from fair to good is a worthwhile investment. Here are a few ways you can start building your credit score.

Pay on time.Payment history accounts for 35% of your credit score. Late or missed payments can have a severe impact, but consistently paying your mortgage, auto loan, or credit card bills on time will lift your score.

Keep a low credit utilization. Keeping credit card balances lower than your credit limit also benefits your score. If you keep your purchases minimal and your payments steady on your credit cards, you should see your credit score improve.

Nurture your credit history. If you’re new to credit, your best bet is to wait it out. Still, keeping a few accounts open for a long time gradually benefits your credit score, and it may launch you into the good credit tier.

To find out where you stand with your credit rating, sign up on Credit.com to see your Experian Vantage 3.0 credit score for free. Checking your credit score will not negatively impact your credit, and you’ll also get a free credit report card that summarizes which credit factors you can improve to boost your credit score.