Buying a cellphone today means buying data. That’s not easy: consumers must make judgments about how reliable the data service is where they will most likely use it, and on how much data they will use. For the most part, consumers are woefully under-informed on those two critical criteria. Before you go out and get a smartphone for your kids or yourself this Christmas, make sure you understand the complete price tag on your purchase.

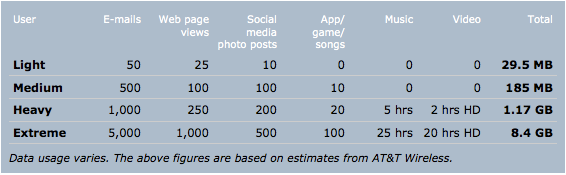

Because service can vary city by city, and even block by block, there’s really only one way to know if a cellphone’s data service will work for you – ask a friend who lives and works near you. But there are some ways to rough out how much data you have to buy, thanks to charts like the one below, from the Citizens Utility Board of Illinois.

Citizens Utility Board of Illinois

If this chart seems overwhelming, here’s a simpler set of guidelines.

What Kind of Data User Are You?

Some of you don’t use data at all. A minority of Americans — 35%, according to Pew — still have “dumb” or “feature” phones. That crowd is best served by simple prepaid plans. There are plenty: Here’s a nice chart, courtesy of Best Buy. If you want to stay traditional, the top carriers all have $40-$50 monthly call-and-text plans.

For the rest of you, I think it’s helpful to put yourself in one of three categories: light, medium or heavy data user. I’m not suggesting this is foolproof: most folks move from less to more, as they discover apps that they can’t resist (mine is my SlingBox — I have to watch my hockey games away from home!). But it’s a start.

Light users who promise to never watch video on their phones can get away with 1 or 2 GB. Medium users who might watch one or two TV shows or games per month, or download a lot of emails with attachments, need about 5 GB. I (and my hockey games), and my frequent use of tethering to get my laptop online, need 10 GB. Beyond that, you should really use Wi-Fi more often.

Once you’ve selected a category, you’ll have a much easier time selecting a plan.

The Big 4: Best for Data Hogs

- T-Mobile has the cheapest data-hoarder plans of the large carriers. For $70 (plus fees) you get unlimited phone surfing, and you can tether (capped at 2.5 GB). For $60 (plus fees), you get 2.5 GB on the phone. For either price, you’ll also have to buy a phone or finance one for $100-$200 upfront and another $20-$30 monthly.

- Verizon, which tends to have the best coverage, has the most expensive plan. You can’t really get a working Verizon smartphone plan for under $100 monthly. All Verizon smartphones now require a poorly-named “share-everything” plan, even if you are sharing the data only with yourself. The Verizon guys charge $40 per device, and $60 for 2 GB, for a total of $100 (plus fees). A 10 GB plan and phone costs $140.

- AT&T’s plans are a pinch cheaper than Verizon’s. For example, a 2 GB plan costs $45 for the phone and $50 for data, or $95 total (plus taxes). A 10 GB plan costs $30 for the device plus $100 for data, or $130.

- Sprint was the cheapest service until T-Mobile began offering a new set of plans. Sprint gets credit for simpler pricing models. Unlimited data costs $80, and you can add 5 GB of tethering for a total of $110.

(Note: These terms are subject to change.)

Alternative Carriers

If you have done your time with one of the big four, you are out of your contract, and you now own a 4G phone you like, you are in luck. You can “bring your own device” to smaller carriers like Straight Talk, sold at Walmart, and probably cut your bill in half. T-Mobile offers a competitive BYOD plan, too. Most 4G smartphones are good enough for most consumers to read email on the go, browse the Web and use basic apps. No need to get a fancy new gadget and get stuck in another long contract. Once you’ve finished paying your contract dues, you are a free agent. Stay that way. Go month to month with a smaller carrier.

Non-contract carriers – also known as prepaid carriers, or in the industry as MVNOs, or mobile virtual network operators – are also a good option for low data users. Some have plans as low as $30 per month for a drizzle of data use. If you only plan to use your smartphone for the bare minimum, such as an emergency email here or there, the Big 4 don’t really want to deal with you. Even if you have to buy a cheap 4G smartphone, carriers like Net 10 or Virgin Wireless offer real value at lower usage levels.

But note: These alternative carriers all ride along the networks owned by the big four, so the service is only as good as the coverage in your area. Also, while you will see ads hawking “unlimited service,” these can be confusing: Straight Talk, for example, throttles users down to painful 2G speeds if they use more than 2.5 GB in a month.

Image: petrunjela

You Might Also Like

With two stimulus checks under our belts, planning is curren... Read More

March 11, 2021

Personal Finance

The COVID-19 pandemic has taken a financial toll on nearly all of... Read More

March 1, 2021

Personal Finance

The following is a guest post by Orion Talmay, of Orion’s M... Read More

February 18, 2021

Personal Finance