The largest auto insurers often charge higher premiums to safe drivers with low to moderate incomes than they do higher-income drivers who recently caused an accident, shows an analysis from the Consumer Federation of America released Monday.

The CFA report “The High Price of Mandatory Auto Insurance for Lower Income Households” looked at income data and insurance premiums for consumers in 8,222 ZIP codes making up 50 urban areas across the country (though income data was not available for some ZIP codes). It focused on premiums for drivers residing in ZIP codes with a high concentration of low- to medium-income (LMI) households, and it found a trend of high auto insurance premiums among drivers in LMI areas, in comparison to higher-income areas.

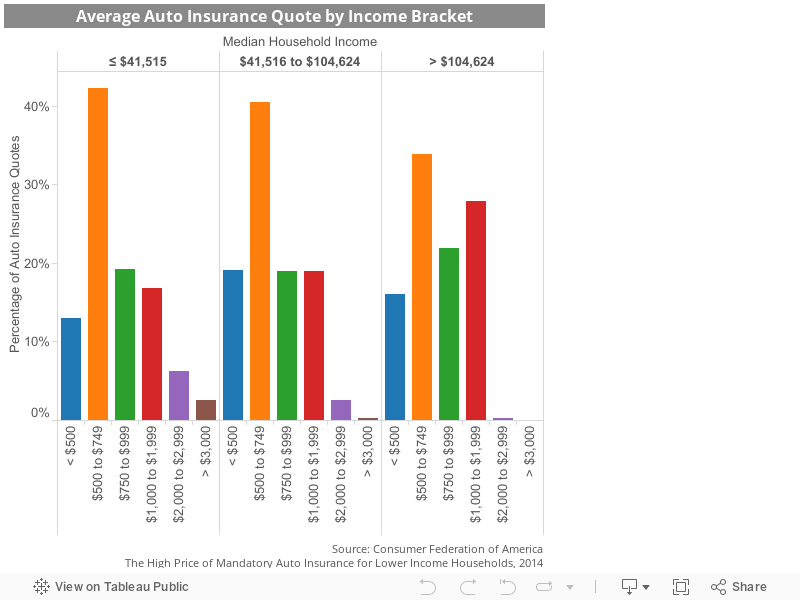

The analysis is based on January 2014 quote data from 207 insurance companies and affiliates, including the five largest insurance companies by national market share: Allstate, Farmers, GEICO, Progressive and State Farm. All quotes were based on the same driver profile:

The Driver

- Sex: female

- Age: 30

- Years driving: 14

- Education: high school diploma

- Occupation: clerical worker

- Credit rating: fair

- Vehicle: 2000 Honda Civic EX

- Auto use: drives 20 miles round-trip to work 5 days a week and logs 10,000 miles a year

- Other information: no accidents, moving violations or licenses suspensions; no group discounts; no lapse in coverage; 10-year home-rental history

The quote is for state-minimum auto insurance (every state but New Hampshire requires drivers to purchase accident-liability insurance).

Among drivers with that profile living in a ZIP code where the median household income was equal to or less than $41,515, the average premium exceeded $500 for 87% of them (so 13% had access to an insurance premium less than $500). Conversely, more drivers (19.1%) living in an area where the median household income is between $41,516 and $104,624 received premium quotes for less than $500. Even in affluent ZIP codes, where the median household income is greater than $104,624, 16% of drivers received premium quotes for less than $500.

Perhaps most notable: In nine of the 50 urban areas (as determined by the Census Bureau), drivers in low- to medium-income ZIP codes would have no access to premiums less than $500.

Another noteworthy aspect of this study is a nationally representative survey CFA conducted in 2013, asking consumers: “For, say, a 30-year-old woman with a modest income and ten years of driving experience with no accidents or moving violations, what do you think is a fair annual cost for the required minimum level of this liability insurance?” Here’s how those answers played out:

“A fair annual premium should be…”

- less than $500 (76%)

- $500 to $749 (10%)

- $750 to $1,000 (4%)

- $1,000 (5%)

- don’t know (5%)

Based on these analyses, public sentiment is severely at odds with the realities of auto-insurance pricing. For consumers with low incomes, budgeting for an expensive auto-insurance premium can take quite a toll on family finances, as having a car is a huge part of employability for many occupations in much of the country, so it’s often an inflexible expense.

Given this reality, it’s important for consumers to control what they can, beyond practicing safe driving: Shop around for your best available insurance rates, take advantage of discounts when possible and keep your credit standing in good shape, because credit can have a significant impact on what you pay for car insurance, depending on where you live. Pull your annual free credit reports from the three major credit reporting agencies for errors or other problems that need your attention, and look at your credit scores regularly to see where you stand. You can use a resource like Credit.com to see your credit scores for free.

More on Auto Loans:

- Are There Car Loans for People With Bad Credit?

- What to Do If You Can’t Make Your Car Payments

- Top 5 Worst Car Buying Mistakes

Image: monkeybusinessimages

You Might Also Like

Find out if your rent and utility payments are reported on your c... Read More

April 11, 2023

Uncategorized

Becoming an authorized user is a common tip for individuals tryin... Read More

September 13, 2021

Uncategorized

Long-term unemployment can really hurt—and not just financially... Read More

August 4, 2021

Uncategorized