You don’t need a chart to tell you it’s expensive to buy a home in most large U.S. cities. You’ll probably be surprised to learn that average salaries don’t come close to paying for average homes in most places, however. You might be really surprised at how affordable some places are. But above all, you’ll almost certainly be shocked at just how much difference geography makes in the price of a home.

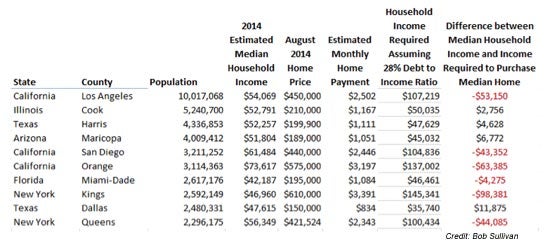

Monthly mortgage payments required to afford a median-priced home in the 10 most populous counties in the U.S. range wildly — from $834 in Dallas County, Texas, to $3,391 in Kings County, N.Y., according to data provided to Credit.com by RealtyTrac. Harris County, Texas, where Houston is located, was almost as inexpensive, costing $1,111 monthly. Maricopa County, Ariz., at $1,051 monthly, and Miami-Dade County, Florida, at $1,084, also enjoy low-cost home ownership. On the other side of the spectrum, Queens, N.Y., costs $2,343, while Los Angeles County costs $2,502 and Orange County, Calif. Costs $3,197.

The monthly estimates are derived from RealtyTrac’s data of sold properties in August, and include property taxes and homeowners’ insurance, assume a 30-year fixed rate mortgage at 4.2%, and the ability to put down 10% of the purchase price and pay for closing costs out of pocket. Costs would be higher for buyers with less than perfect credit or smaller down payments.

Housing Affordability in the Biggest U.S. Counties

The biggest impact on monthly payment, of course, is the price of homes. In Dallas, the median-priced home for sale in August was only $150,000. That price tag probably sounds painful to a house hunter in Orange County, where price tags in the middle of the market was an eye-popping $575,000, or in Kings County N.Y., where the median price was $610,000.

Roughly 40 million Americans live in these top 10 most populous counties, or about 13% of the nation’s population.

Of course, housings costs don’t exist in a vacuum. What really matters is the relationship between income and costs. Who cares if homes are cheap in a part of the country where there are no jobs? Again, with the help of RealtyTrac, we developed a measure to see where median-priced homes were affordable to families with median incomes — presuming that affordability meant mortgage payments should not eat up more than 28% of a household’s income. By that measure, housing costs in the nation’s top 10 counties are decidedly mixed.

Which Big Counties Are the Least Affordable?

In six counties, costs far outpaced incomes, creating a kind of perpetual economic stress on residents. But in four other counties, costs were downright reasonable.

In L.A. County, where 10 million Americans live, median income was $54,000 and median home price was $450,000, requiring a monthly home payment of $2,502, or $30,024 annually, eating up more than half of that income. That’s a recipe for disaster. In Cook County, which includes Chicago, incomes are $52,791 but median prices drop to $210,000 for a much more affordable monthly cost of $1,167, comfortably about one-quarter of household income. And in Harris County, Texas, households are apparently living large, earning $52,257 but paying only $13,332 annually for a median-priced home, leaving plenty of disposable income.

Changing the debt-to-income ratio required to buy a home – increasing the amount of monthly income that’s safe to put toward a house payment – makes cities in the list look more affordable. But even if 43% of income is devoted to the house payment, in five of the 10 markets, a median income still couldn’t afford a median-priced home.

The wide range of costs is having a real influence on Americans’ life choices, says Daren Blomquist, vice president at RealtyTrac.

“One of the reasons we see a state like Texas with three of the five fastest growing cities in the nation is because of much more affordable homes to buy,” he said. “I think people have heard that said, but when it’s broken down into a monthly payment, the reality of how big the difference is really stands out.”

Having money left over at the end of the month, after housing costs, has a life-altering impact on spending choices for families, Blomquist said.

“The hundreds or even thousands of dollars a month a homeowner in the more affordable markets is not spending on housing can be spent on other items, or saved,” he said. “That gives homeowners in those more affordable markets much more control over building their wealth over the long term, rather than putting all their wealth building eggs in the one basket of home price appreciation — which is what many homeowners in the high-end markets are doing.”

More on Mortgages and Homebuying:

- Why You Should Check Your Credit Before Buying a Home

- How to Get a Loan Fully Approved

- How to Search for Your Next Home

Image: SeanPavonePhoto

You Might Also Like

Learn more about credit union mortgage options. Use this credit u... Read More

December 13, 2023

Mortgages