Do you know if there are errors on your credit report? Have you even looked to find out?

If you’re like nearly one-quarter of respondents in a recent survey, the answer is that you have no idea.

According to the survey, conducted in September by Qualtrics on behalf of our partner CreditRepair.com, 23.59% of respondents didn’t know if there was an error on their credit report; 24.02% knew there was at least one item they felt was in error; and 52.39% said there were no errors.

Checking your credit report is an important first step in taking control of your financial life. Of course, looking at your credit report is one thing — understanding it is another. (Here’s a cheat sheet on how to read your credit reports.) One of the biggest reasons to review your credit reports is to watch out for errors, because an inaccurate credit report can hurt your credit scores and, in turn, cost you a lot of money.

According to a 2012 report from the Federal Trade Commission, one in five people have flawed credit reports. Not all of these mistakes hurt credit scores, but many do. According to the same study, one in eight people have lower credit scores because of these mistakes.

Since your credit score typically determines what interest rate you pay on your debt, an artificially low credit score means you might pay higher interest than you otherwise should.

Keep in mind that even a tiny point penalty could cost you big. If your score just misses the next highest bracket because of those errors, you could be stuck in a lower-rated group and that means higher interest rates.

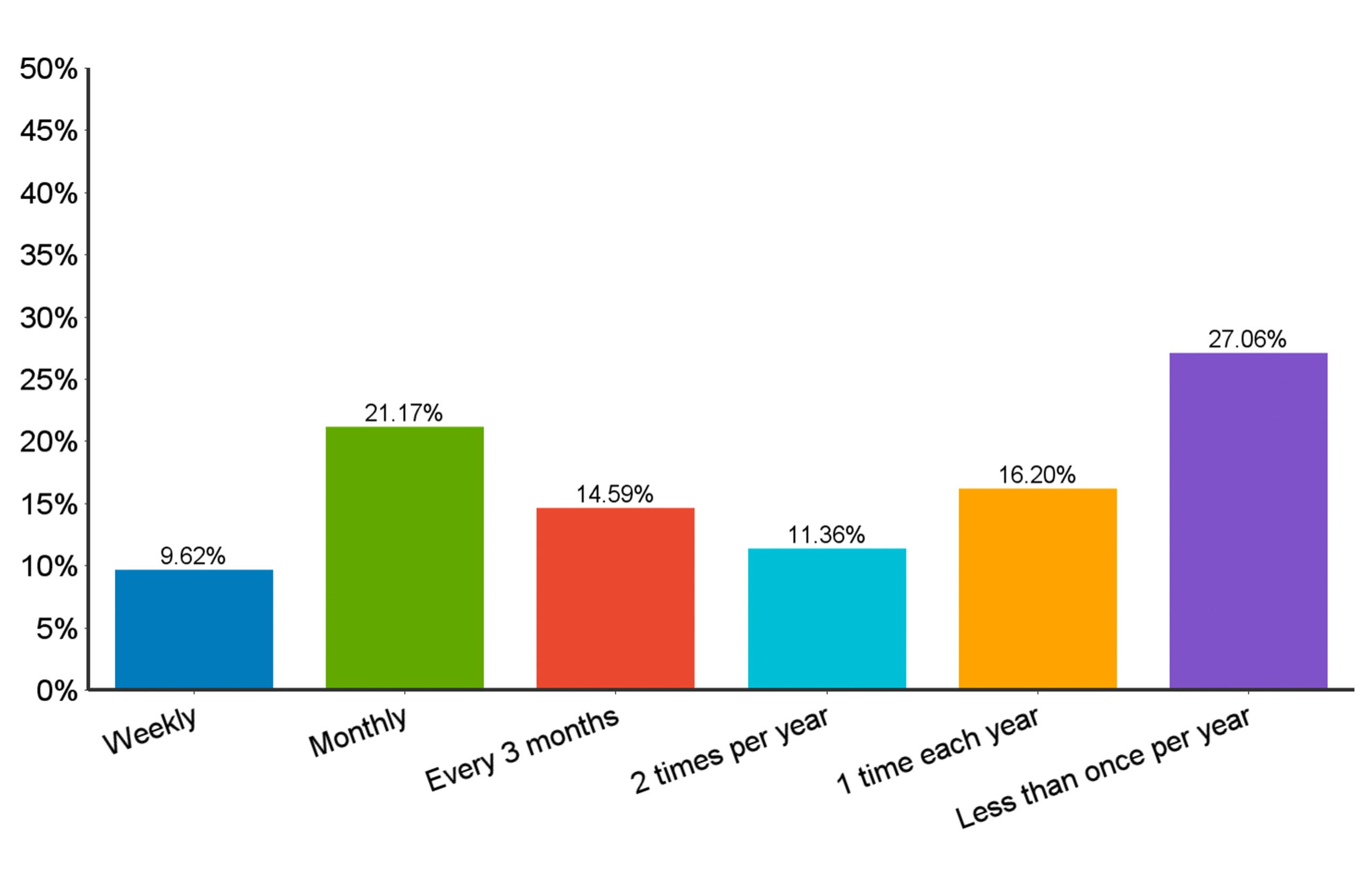

How Often Do You Check Your Credit Report or Score?

Of the 1,611 respondents to the CreditRepair.com survey, 27.06% said they check their credit report or credit score less than once a year, and 9.62% said they check weekly.

Of the 1,611 respondents to the CreditRepair.com survey, 27.06% said they check their credit report or credit score less than once a year, and 9.62% said they check weekly.

You can get your credit reports for free once annually from each of the three major credit reporting agencies at AnnualCreditReport.com. Look for any items that are clearly reported in error, but don’t stop there. By law, creditors and credit bureaus must correct or remove items if they are inaccurate, unverifiable or incomplete.

Checking your credit score regularly is also a good way to get a heads-up that there might be an error impacting your credit. (You can get a free monthly credit report summary from Credit.com to help you spot changes along the way.)

More on Credit Reports & Credit Scores:

- How to Get Your Free Annual Credit Report

- How Do I Dispute an Error on My Credit Report?

- How Credit Impacts Your Day-to-Day Life

Image: iStock; Chart Courtesy of CreditRepair.com

You Might Also Like

Experian is a credit reporting agency. It also offers consumer cr... Read More

March 7, 2023

Credit Score

Do you keep a close eye on your personal finances? Or maybe you�... Read More

January 4, 2021

Credit Score

If you’re serious about your credit score, you need to pay your... Read More

September 29, 2020

Credit Score