There is much discussion about the inability of young people to buy homes — let alone move out of their parents’ homes — and how the lack of first-time buyers is hurting the entire housing market.

Plenty of charts and data, including stories we’ve run on Credit.com, show how unaffordable many big U.S. cities can be.

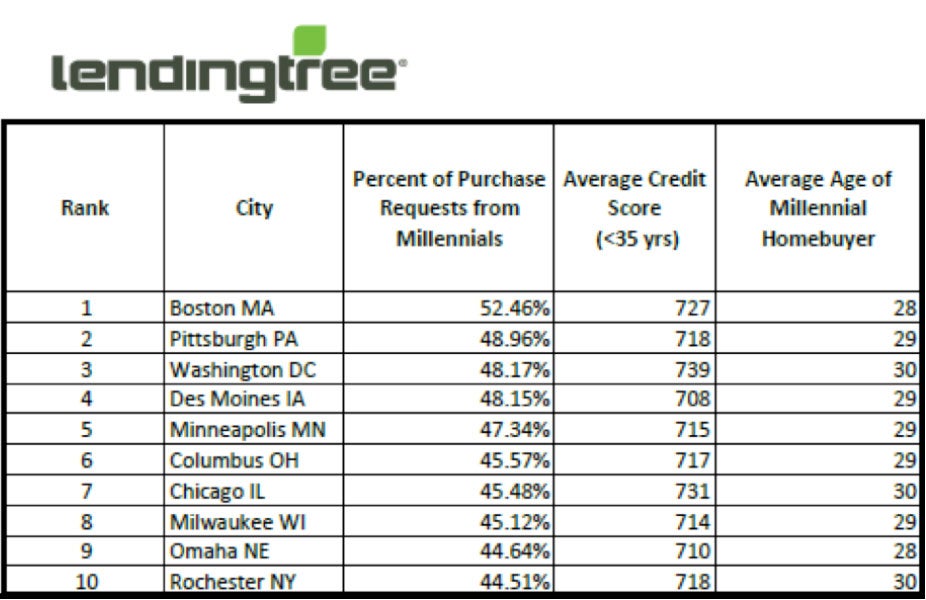

But a new study by LendingTree claims millennials are looking for home loans in many places. In fact, the 34-and-under crowd made up nearly half the mortgage requests that flowed through LendingTree during the past 12 months for cities like Boston, Pittsburgh and Washington, D.C., LendingTree said. Cities like Des Moines, Iowa, Minneapolis and Omaha, Neb., weren’t far behind.

“The under-35 crowd had been, for some years, hesitant to enter the housing market, but we’re seeing that start to shift,” said Doug Lebda, CEO of LendingTree. “The data all points to the fact that millennials are increasingly eager to own rather than rent, and even the incredibly high real estate prices in some markets don’t necessarily deter them.”

The LendingTree data comes with some caveats; it only represents requests for information made through the site, so the sample studied might skew tech-heavy. But the data is consistent with other studies.

RealtyTrac, a housing analyst firm, recently crunched the numbers on affordable markets and came up with similar results.

“Many of the same markets mentioned in the study … are on this list,” said Daren Blomquist, RealtyTrac senior vice president. “When filtering for affordability, the markets most likely to see an increase in millennial ownership are those with the combination of an increase in the millennial share of the population and relatively affordable homes to buy.”

Getting millennials to buy homes is incredibly important to generating a sustainable housing market recovery. First-time homebuyers are needed to help generate market activity— without them, homeowners cannot trade up into larger homes.

“The millennial generation is the key to a sustained real estate recovery and boomers who are downsizing are helping open the door for many first-time homebuyers while also driving demand for purchases and rentals in the markets where they are moving,” Blomquist said.

Numbering 43.5 million, the older group of millennials (aged 25 to 34) makes up 13.6% of the U.S. population but fully 30% of the current population of existing-home buyers, according to Realtor.com.

Millennials stuck at home also aren’t forming households, so they aren’t buying couches, lamps, refrigerators and other items associated with wider economic activity. The living-at-home phenomenon remains a big problem. In 2014, according to the Pew Research Center, 14.7% of those aged 25-34 lived with their parents, the highest percentage recorded since the Census Bureau started counting in 1960.

But LendingTree says there may be light at the end of the tunnel.

“Overall, we’ve seen a 28.5% increase in loan requests from millennials this past year over the prior one, evidence that the appeal of homeownership is strong — and growing — for young buyers,” said Lebda.

Ironically, at least some of that new demand might not be the result of better prospects for young people, but rather the punishing increases in rents, which is nudging young people towards mortgages.

That effect isn’t universal, however. In blistering-hot Portland, rents are rising faster than anywhere in the nation, according to ABODO.com.

Still, it ranked 50th of 50 markets in LendingTree’s study of places where young people are inquiring about mortgages (Only 38% of the market). Also near the bottom: San Jose, Calif., (also 38%), Aurora, Colo. (39%) and naturally, New York City (39%).

For its study, LendingTree examined request for mortgages (not mortgage applications) through its site.

“Fortunately, LendingTree’s data is typically representative of the entire U.S. population based on trends and demographics,” said spokeswoman Megan Grueling. “With that said, it is possible that it is slightly skewed, which is why we used the percentage of total requests from millennials versus other generations.”

If you want to get an idea of how much home you can buy, you can check out this home affordability calculator. (You can check your credit scores for free on Credit.com to see where you stand.) And if your credit score isn’t in good enough shape to consider buying, you can start improving your credit by checking your free annual credit report to see where you stand, and start correcting any errors you might find there.

More on Mortgages & Homebuying:

- Why You Should Check Your Credit Before Buying a Home

- How to Find & Choose a Mortgage Lender

- How to Refinance Your Home Loan With Bad Credit

Image: Anetlanda

You Might Also Like

Learn more about credit union mortgage options. Use this credit u... Read More

December 13, 2023

Mortgages