It turns out the gender pay gap affects more than just a woman’s ability to make as much as a man. Studies show it also has an impact on how much money women are able to save, and, most recently, how much value a woman’s home as a single buyer might have.

A new analysis by RealtyTrac shows that homes owned by single men are valued 10% more on average than those owned by single women. The men’s homes also have appreciated 16% more since purchase than those owned by women.

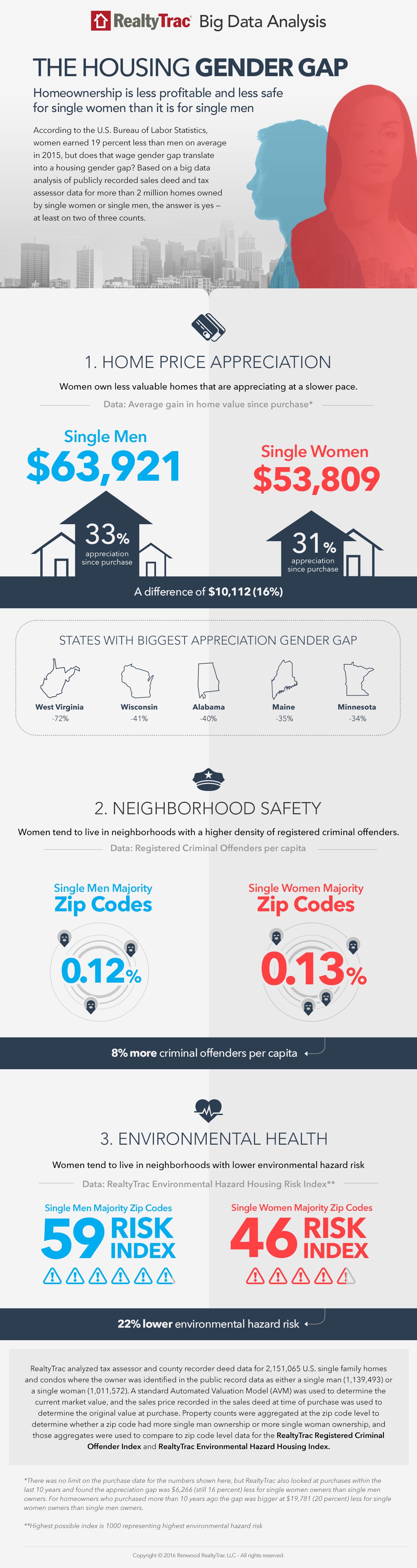

The analysis covered more than 2.1 million single family homes nationwide owned by either single men (1,139,493) or single women (1,011,572) based on public record tax assessor data collected by RealtyTrac.

The homes of single men had an average market value of $255,226, while those owned by single women had an average market value of $229,094.

The single men’s homes analyzed also had an average appreciation of $63,921 since purchase (33%), while the average single woman’s home value increased by $53,809 (31%).

Click on the infographic for a larger version.

“Women earn less than men on average — 19% less in 2015, according to the Bureau of Labor Statistics — giving them less purchasing power when it comes to buying a home,” said Daren Blomquist, senior vice president at RealtyTrac. “So it’s not surprising to see the 10% gender gap in average home values between single men and single women homeowners; however, the slower home price appreciation for homes owned by single women demonstrates that less purchasing power is also having a domino effect on their ability to build wealth through homeownership as quickly as single men.”

RealtyTrac’s analysis also found that, among homes owned for at least 15 years, those owned by single men on average had a current market value of $288,912 — 17% higher than the average current market value of homes owned by single women: $240,166.

Among these older homes, the men’s gained an average of $170,765 since purchase — a 145% return on purchase price. That’s an appreciation of $36,496 more over the average $134,269 gain since purchase seen by single women over that same time period.

Where the Housing Gender Gap Is Biggest

The analysis found that the average value of single men’s homes were highest compared to single women’s in the District of Columbia (14%), followed by Florida (12%), West Virginia (12%), Wisconsin (12%), Texas (10%), and Alabama (10%).

There were three states where the average values of homes owned by single women were higher than the average values of homes owned by single men: Massachusetts (11%), Kentucky (2%), and Kansas (1%).

Regardless of your gender, bad credit can keep you from owning your own home. Consumers with scores below 620 can have a tougher time securing financing. That’s a common credit score benchmark for government-backed loans (Federal Housing Administration, U.S. Department of Veterans Affairs and the U.S. Department of Agriculture), while conventional lenders might want a score that’s closer to 640 or 660.

Different lenders can have different credit score cutoffs, however. But even if you clear a lender’s baseline, working hard to improve your score may also help you nab a better interest rate. You can monitor your progress by getting your free credit report summary each month on Credit.com.

More on Mortgages & Homebuying:

- Why You Should Check Your Credit Before Buying a Home

- How to Find & Choose a Mortgage Lender

- How to Refinance Your Home Loan With Bad Credit

Image: knape

You Might Also Like

Learn more about credit union mortgage options. Use this credit u... Read More

December 13, 2023

Mortgages