It’s common knowledge that a car’s value begins to depreciate as soon as it leaves the sale lot. But did you know its color can affect its resale value as well?

According to a new study by iSeeCars.com, an automotive data and research company based in Boston, color plays a huge role in determining a car’s retained value.

To conduct the study, iSeeCars.com analyzed more than 1.6 million used 3-year-old cars (model year 2013) of all colors sold between June 1, 2015 and June 30, 2016. It then calculated each cars’ depreciation over three years by comparing the average listing price to the average MSRP (adjusted for inflation) for each car color and body style/target market. Any colors with fewer than 1,000 cars, as well as colors and body styles/target market segments with fewer than 30 cars were excluded.

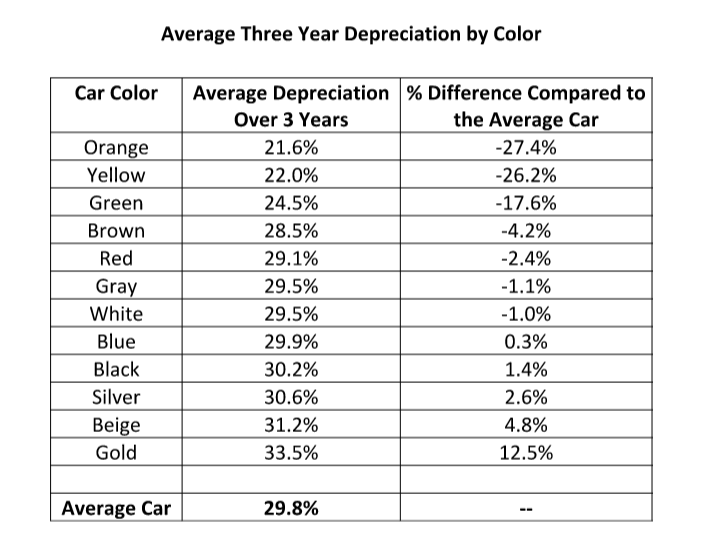

As iSeeCars found, the average car depreciated 29.8% over the first three years of ownership, while orange- and yellow-colored cars depreciated the least of any color (27.4% and 26.2% less than the average car, respectively). At the other end of the spectrum were beige- and gold-colored cars, which depreciated the most — 4.8% and 12.5% more than the average car, respectively.

You can see the average three-year depreciation rate for cars by color below.

Charts via iSeeCars.com

Apparently, popular car colors like white, gray and black depreciated closer to the average car. “Because buyers shopping for such colors have a lot more choices, sellers may not have as much pricing power,” Phong Ly, chief executive of iSeeCars.com, explained in a press release. Conversely, consumers with an orange, yellow or green car may have more luck because those are more unusual colors.

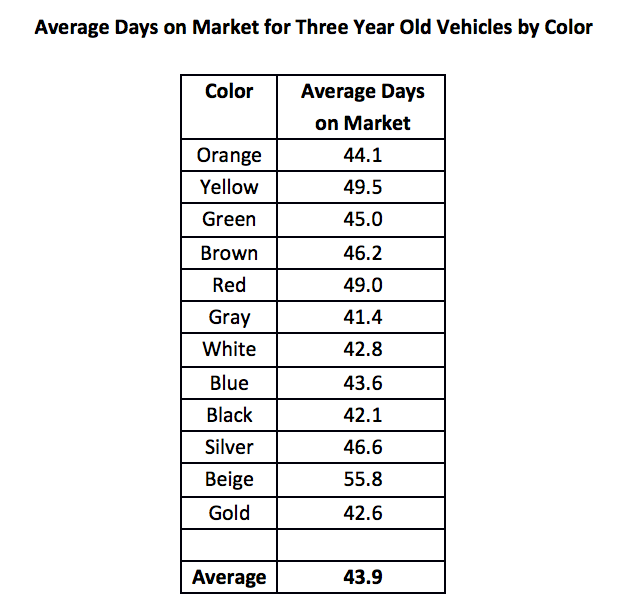

Interestingly, while the average 3-year-old car takes 43.9 days to sell, the average for orange cars is 44.1 days and 44.9 for green cars. “In fact,” according to the release, “cars of almost any colors except beige sell within 6 days of the average car.”

Need a Ride?

With new cars losing anywhere between $3,000 to $5,000 the moment they drive off the lot, it’s no wonder many people find buying a car to be such a hassle. Just think, if you’re financing the car with an auto loan, that depreciation could mean you’re suddenly “upside-down” on the loan, owing more than the car’s even worth.

Of course, there are ways to get around the problem. You can research online at sites like Kelley Blue Book and Edmunds, which offer free information on models, safety and prices, and you can comparison shop for cars in your price range. Once you’ve got the right car in mind, you can dig up its history online. (Just make sure to grab its VIN number beforehand.)

Remember, buying a car is one of the biggest purchases you’ll make, so take the time to do it right. It can take minutes to set your eyes on a set of wheels, but paying for it is a whole other story. Whether you choose to lease or finance, you’ll want to make sure your credit’s in tip-top condition before you apply, as this will determine what terms you may qualify for. You can view two of your credit scores, updated every 14 days, for free on Credit.com.

Image: Deklofenak

You Might Also Like

Find out if your rent and utility payments are reported on your c... Read More

April 11, 2023

Uncategorized

Becoming an authorized user is a common tip for individuals tryin... Read More

September 13, 2021

Uncategorized

Long-term unemployment can really hurt—and not just financially... Read More

August 4, 2021

Uncategorized