If buying a house is on your radar, you’re probably already browsing online listings and saving up for a down payment.

Well, there’s one more thing you need to add to your to-do list: improving your credit score.

Just like knowing the credit score you need for other big transactions, you should be aware of the three-digit number that’ll help you finance your dream home.

How your credit score plays into buying a house

When you start the homebuying process, you typically apply for a preapproval. It gives you a sense of how much you can borrow and also shows a home seller that you’re ready to move.

Before a lender tells you how much you can borrow, they’ll consider your full financial picture, not just your credit score. Your debt-to-income (DTI) ratio is another big factor they consider, for example.

But let’s focus on your credit score. After all, improving it is easier than finding a higher-paying job to lower your DTI ratio.

You might be wondering what makes for a good credit score. You can start to answer that question numerically. Here are ranges of credit scores by quality, according to Experian:

- 800 and above: Exceptional

- 740 to 799: Very good

- 670 to 739: Good

- 580 to 669: Fair

- 579 and below: Poor

Mortgage lenders typically review your credit scores from each of the three major credit bureaus — Experian, TransUnion, and Equifax.

The better your score, the lower your interest rate. This is a big deal because any slight difference in your mortgage rate can result in significant savings (or losses) over the length of your mortgage.

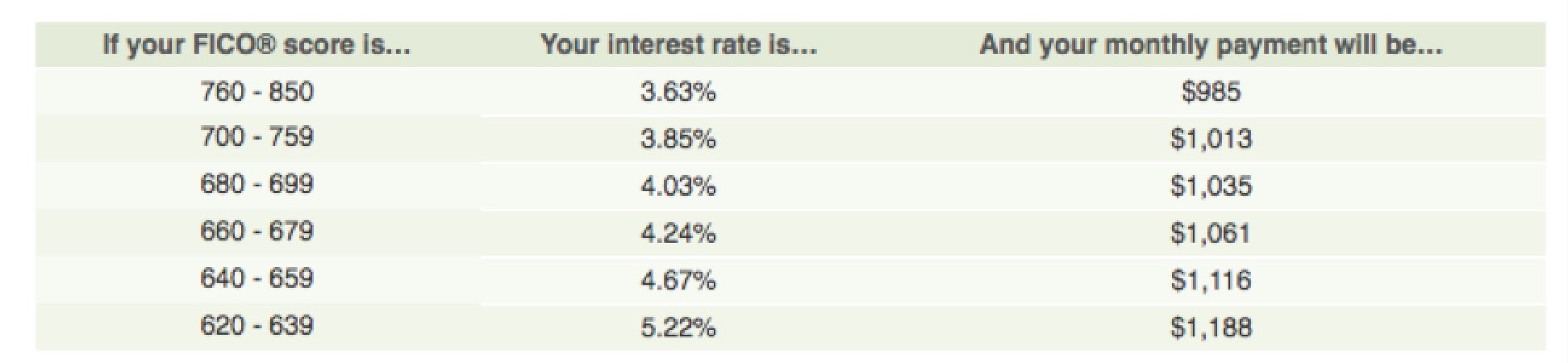

For example, consider how these national rate averages affect monthly payments on a 30-year, fixed-rate mortgage of $216,000:

Image credit: MyFico.com

Based on these December 2017 rates, a homebuyer with a score of 700 would pay $103 less per month than a homebuyer whose score is 640. Their superior credit score would save them $1,236 per year — or $37,080 over the life of their mortgage.

The consequences become more serious the lower your credit score. Having a score below 600, for example, would result in a subprime mortgage which would burden you with an even higher interest rate.

The credit score you need to buy a house

The credit score you need to buy a house depends on a host of factors. Chief among them is the cost of the house you’re looking to buy and the size of the down payment you’re prepared to make.

Say you won’t be making a down payment of 20 percent of the home’s cost (the threshold for avoiding private mortgage insurance, or PMI).

In this case, your credit score would also affect your PMI monthly dues. The higher your score, the less you’d have to pay your insurer.

You need a credit score of at least 620 to borrow a conventional home loan backed by Fannie Mae or Freddie Mac. Other types of home mortgages have other criteria:

- Military members: The U.S. Department of Veterans Affairs guarantees home loans to qualifying active or retired service people. Applicants must have satisfactory credit, but no minimum is set.

- First-time homebuyers: The Federal Housing Administration offers loans to people who have subpar credit and an inability to make a large down payment. Under the program, a borrower with a 580-or-higher credit score must pay 3.5 percent of the home’s cost upfront. A borrower with a credit score below 580 would have to make a down payment of 10 percent.

- Rural homebuyers: The U.S. Department of Agriculture has three homebuying programs to help families afford housing in eligible areas. The minimum credit score for each program is 620.

For aspiring homebuyers, there is another option: manually underwritten loans that require no credit check at all. To prove your ability to repay the loan, you’ll provide these alternative lenders with other examples of credit. You could show them your routine monthly bills plus your larger expenses like rent or tuition payments.

How to improve your credit score before buying a house

There are many possible reasons you’ll want to improve your credit score before buying a house. Maybe you have a good enough credit score for a conventional loan but want to lower your potential mortgage interest rate. It’s also possible you’re seeking to improve your score to meet a lending program’s minimum requirements.

Whatever the case, it’s wise to review how your credit score is built. Your score is comprised of five different factors, according to FICO:

- Payment history: 35 percent

- Amounts owed: 30 percent

- Length of credit history: 15 percent

- Credit mix: 10 percent

- New credit: 10 percent

For each of these categories, there are steps you can take to improve your score. You’ll want to prioritize the categories that make up the greatest portion of your score, starting with payment history and working your way down.

If you’re current on payments but have high balances, you might instead focus on paying down your debt. After all, the average American household has $6,662 in credit card debt.

Here are some steps you can take to work on each category:

- Payment history: Get up to speed on your monthly bills. Setting up payment reminders or automatic payments is a good way to ensure you stay current.

- Amounts owed: To improve your DTI ratio, keep your credit card balance as low as possible on a monthly basis.

- Length of credit history: Avoid opening new lines of credit. That’ll drop down the average age of your accounts.

- Credit mix: Instead of opening a new credit card, for example, focus on making progress on your existing credit card and loan payments.

- New credit: When applying for credit, shop rates in a short amount of time to lessen the impact of lenders’ credit checks.

Some categories are more doable than others. You might have an easier time becoming current on your student loan payments, for example, than paying them off. That effort would help in the “payment history” category even if your “amounts owed” doesn’t change all that much.

If you have student loans and hopes of making a down payment on a house, you’re not alone. More than 40 percent of borrowers said they felt loans were stopping them from buying a home, according to a 2017 survey on millennials’ money stressors. But improving your credit score makes buying a house with student loan debt even more possible.

Take your credit score into account when buying a home

The credit score you need to buy a house is different than the one your neighbor might need to buy theirs. It’s different for everyone, in fact, as no one’s financial picture is the same.

The universal truth is that the better your credit score, the better off you’ll be. So if you have a “fair” score now, see if you can work your way up to “good.” But no matter where you are on the ladder, reach for the next rung.

Because buying a home is not a quick and easy process, you should have all the time you need to hike your credit score as high as possible.

If you’re concerned about your credit, you can check your three credit reports for free once a year. To track your credit more regularly, Credit.com’s free Credit Report Card is an easy-to-understand breakdown of your credit report information that uses letter grades—plus you get a free credit score updated every 14 days.

You can also carry on the conversation on our social media platforms. Like and follow us on Facebook and leave us a tweet on Twitter.

I

mage: iStock

You Might Also Like

Learn more about credit union mortgage options. Use this credit u... Read More

December 13, 2023

Mortgages