You take your money and your credit rating seriously. You probably know a thing or two about credit and how it works too. You may think that the savings of your finances—like your savings account, your certificate of deposit (CD) and your other assets—doesn’t affect your credit. For the most part, you’re right. But, does opening a CD affect your credit? The answer is that it actually might.

What Credit Bureaus Use to Determine Your Credit

Your credit score and your credit file are based on how you handle debt. Credit bureaus, such as Experian, TransUnion and Equifax, keep a file on your debt activities. The information on that file is used to calculate your credit score by analyzing how you repay money you borrow, including installment loans and revolving lines of credits, AKA credit cards.

The credit reporting agencies to give you a score by using credit scoring models that look at your payment history, credit utilization ratio (how much of your available credit limit you’ve used), your credit age or credit history, your mix of accounts and how many credit inquiries you have on your file. Lenders and credit card issuers look at that score and sometimes your entire file to determine whether to give you a loan or credit card.

If you miss multiple credit card payments, your credit rating goes down. On the other hand, when you diligently pay bills on time, your credit rating goes up or at least stays the same.

Credit Bureaus Don’t Consider Assets When Determining Your Credit

Assets, such as real estate, CDs and savings accounts, don’t affect your credit score. You could regularly put money in savings, and it won’t affect your credit rating. And you can have a million dollars in savings and still have a bad credit score if you regularly make late payments on your credit card, have maxed out your credit cards or have too many hard inquiries on your file.

Granted, a mortgage lender might give borrower A, who has a million in savings and a 600 credit score, a home loan and not borrower B, who has $100 in savings and a score of 600. But, borrower A and B still have the same credit rating of 600.

The Catch—Opening a CD

There’s one time when assets can creep in and affect your credit score—when you open a new CD or another deposit account. For some reason, some banks and credit unions—not all—do a hard inquiry on your credit when you open a new account.

To put that into perspective, a hard inquiry really isn’t a big deal. Hard credit inquiries only account for about 10% of your credit score. Their cousins—soft inquiries—don’t affect your score at all. A single hard inquiry—also called a hard pull—can stay on your credit file for up to 2 years. It will drop your score by less than five points.

Just Ask

You have the right to ask if the bank, credit union or other financial institution does a hard pull on your credit when you open a CD. So, before opening the CD:

- Ask about the bank’s policy: Bank advisors can tell you upfront whether a hard pull is done for new CDs. If the bank limits checks to soft inquiries, you don’t have anything to worry about.

- Ask for a soft pull: Try asking for a soft pull directly. You’re the one looking to invest your money, so some banks may bend to accommodate your wishes.

If you’re in a situation with your credit rating where that hard pull will hurt, consider opening your CD elsewhere.

How to Assess the Impact of Opening a CD on Your Credit Rating

Depending on your current score, the few points that a hard inquiry put on your credit file is probably minimal. The few times the impact might matter include:

- You’ve applied for financing with several different banks over two or more months or for several different credit cards, which puts multiple hard pulls on your file that add up. Note: multiple hard inquiries for loans in a short period of time are counted as one inquiry.

- Your score is right on the line between two credit ratings. Say it’s at 740 and dropping it five points might take you from a very good FICO credit score to only a good FICO score and you need your score to be higher than lower, say for an upcoming mortgage approval.

Bottom Line on Open a CD and Your Credit Rating

Opening a CD might affect your credit rating if:

- The bank or other financial institution where you’re opening the CD does a hard pull on your credit file.

But, that hard pull should only really hurt your credit if:

- You’ve applied for financing with several different banks over two or more months or for several different credit cards, which has put multiple hard pulls on your file that add up. Note: multiple hard inquiries for loans in a short period of time are counted as one inquiry.

- Your score is right on the line between two credit ratings. Say it’s at 740 and dropping it five points might take you from a very good FICO credit score to only a good FICO score and you need your score to be higher than lower for an upcoming mortgage approval.

Make the Most of Your Savings and Your Credit Rating

Now that you know that opening a new CD might affect your credit rating, you can find out if your chosen institution will do a hard pull if that will hurt your credit.

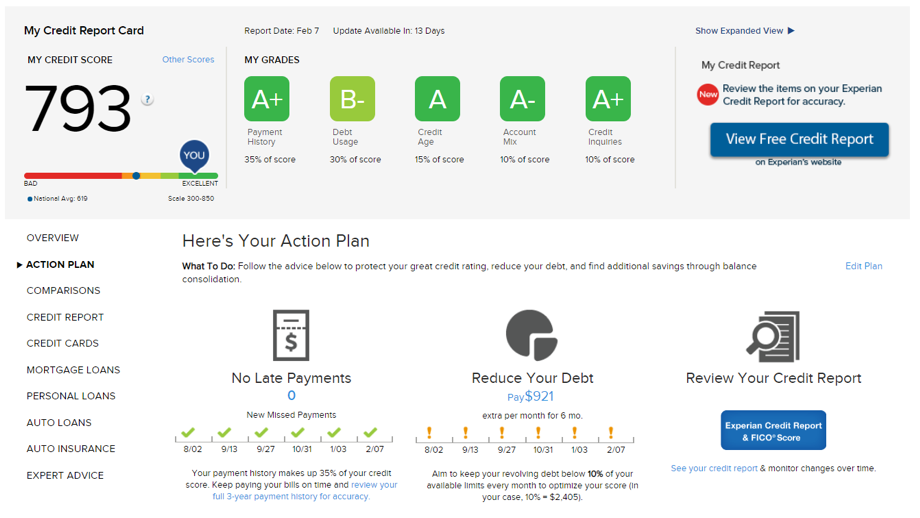

To keep a regular pulse on your credit rating you can also get your free Experian credit score and free credit report card here on Credit.com. Your score and your report card—sample shown below—let you keep an eye on your credit regularly. Along with how you are doing with payment history, debt usage, credit age and account mix, your report also shows how many credit inquiries you’ve had and how they’re affecting your score.

You Might Also Like

Find out if your rent and utility payments are reported on your c... Read More

April 11, 2023

Uncategorized

Becoming an authorized user is a common tip for individuals tryin... Read More

September 13, 2021

Uncategorized

Long-term unemployment can really hurt—and not just financially... Read More

August 4, 2021

Uncategorized