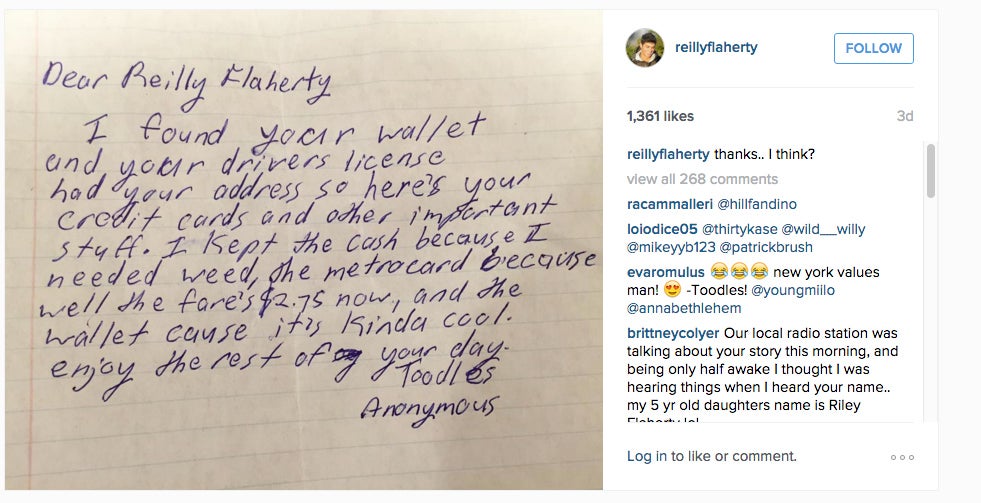

If you lose your wallet, the best case scenario is you get it back, no harm done. One New Yorker’s missing-wallet story is even better than that, because the person who found it returned his credit cards and driver’s license, along with a note explaining his intentions behind keeping everything else. The note is comical in its honesty, which is probably why it went viral.

Reilley Flaherty, the owner of the “kinda cool” wallet, posted the note to Instagram Feb. 15 and the New York Post ran it as a cover photo two days later. Flaherty did not immediately respond to a request from Credit.com for an interview, but he has told multiple media outlets that he had already replaced his credit cards and driver’s license before the anonymous letter-writer returned them.

As fun and feel-good as Flaherty’s tale is, it’s not necessarily a happily-ever-after kind of story (and not just because the person kept Flaherty’s cash, wallet and MetroCard). A driver’s license has a lot of personal information on it that could be copied down and used by an identity thief. Unlike a credit card, replacing a state-issued ID like a driver’s license doesn’t nullify the information on the old one, so you’re not really in the clear when you get a new one.

Sure, we’d all like to think that the person who found Flaherty’s wallet wanted nothing more from him than a few free subway rides and some money for weed, and maybe that’s really the case. However, when things like this happen, you have to consider the worst possible outcomes. That includes someone potentially stealing your identity.

Depending what else is in your wallet (and for the love of all things sensible, that should not include your Social Security card), a thief could do a lot of damage. The information on a state-issued ID alone is very valuable to an identity thief. After something like that falls into the hands of a stranger — even if they give it back — monitor your credit for signs of abuse. A sudden drop in your credit scores could be a sign of identity theft, and you can watch for that by looking at two of your free credit scores every month on Credit.com.

More on Identity Theft:

- How Can You Tell If Your Identity Has Been Stolen?

- What Should I Do If I’m a Victim of Identity Theft?

- How Credit Impacts Your Day-to-Day Life

Image: Thomas Northcut

You Might Also Like

Find out what someone can do with your stolen Social Security num... Read More

October 19, 2023

Identity Theft and Scams

The Federal Trade Commission’s Consumer Sentinel Network re... Read More

May 17, 2022

Identity Theft and Scams

COVID-19 vaccines are being rolled out across the country, and th... Read More

May 20, 2021

Identity Theft and Scams