Credit scores vary a bit, depending on the scoring system, but the purpose is always the same: to determine the likelihood that a consumer will pay his or her debts.

Credit scores may determine whether or not consumers will qualify for a variety of loans, and they also play a factor in the interest rates you get on those loans. From buying a home to getting car insurance, an individual’s credit score has a significant impact on how much that person pays for things.

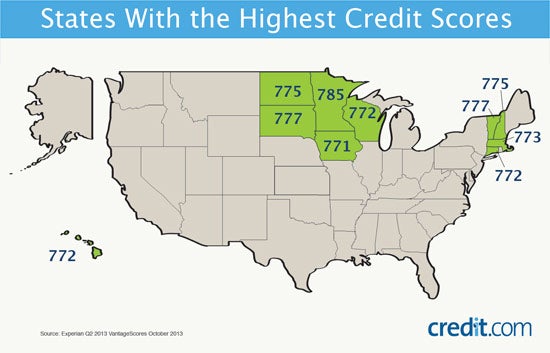

With that in mind, we wanted to find out which U.S. states have the highest credit scores. Experian provided Credit.com with its calculation of the average VantageScore in each state and the District of Columbia from the second quarter of this year.

VantageScore is a scoring method created by the three major credit bureaus — Experian, Equifax and TransUnion. The newer model, VantageScore 3.0, which is not used in these calculations, has a scale more aligned with other scoring models: 300 to 850.

The VantageScore scale for the model used in these calculations is from 501 to 990. Generally, 900 to 990 is considered excellent, 800 to 899 is good, 700 to 799 is fair, 600 to 699 is poor and 501 to 599 is bad.

The nation ranges from 707 to 785, with the average at 748.

According to Experian’s calculations, Minnesota has the best average credit score. While the three bureaus use the same formula to determine VantageScores, credit reports vary from bureau to bureau, which could result in score differences.

States With the Highest Credit Scores

Interestingly, with the exception of Hawaii, the states with the highest credit scores are clumped in two sections of the country: New England and the northern Midwest.

10. Iowa — 771

7. Tie: Connecticut, Hawaii, Wisconsin — 772

6. Massachusetts — 773

4. Tie: New Hampshire and North Dakota — 775

2. Tie: South Dakota and Vermont — 777

1. Minnesota — 785

If you wonder what your credit scores are, it’s a good idea to check them regularly. There are a number of free credit score tools online, and Credit.com’s Credit Report Card is one that offers you your credit scores and a breakdown of your credit profile so you know what areas you need to work on to build your credit.

Image: iStock

You Might Also Like

Experian is a credit reporting agency. It also offers consumer cr... Read More

March 7, 2023

Credit Score

Do you keep a close eye on your personal finances? Or maybe you�... Read More

January 4, 2021

Credit Score

If you’re serious about your credit score, you need to pay your... Read More

September 29, 2020

Credit Score