Shhh….The worst part of the Great Recession wasn’t the housing bubble. Or the loss of retirement savings. No, the dirty little secret about America’s most recent economic calamity is the massive surge of long-term unemployment that has struck the American workforce, and remains a scourge on the nation. Even with the economic recovery well under way, the long-term unemployment rate remains higher than any time before the recession, dating back to 1950, when the Fed began counting such data.

Fully one-third of the unemployed have been out of work for more than six months, according to the Fed.

Yet even the unemployed are holding on tight to the American Dream, according to Credit.com’s American Dream Survey. In fact, America’s recently unemployed adults don’t feel any less optimistic about their ability to achieve the American Dream than the general population, the survey suggests.

Long-term unemployed face special problems, however. Research has shown they are much less likely to get job interviews, making their climb out of the recession’s hole that much harder. Many in the group stop looking, and thus are no longer counted in what’s known as the “headline unemployment” rate. That’s one reason the unemployment rate seems to be going in the right direction, but the “employment rate” – the percentage of adults an economy employs — is staying stubbornly flat.

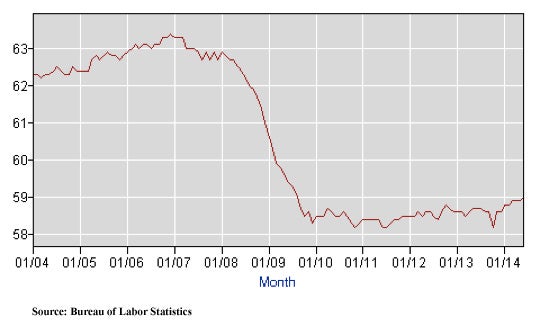

Sometimes called the “employment-population” ratio, the employment rate is a more comprehensive measure of how the economy is doing, some researchers believe. It fell below 60% in March 2009, according to the Bureau of Labor statistics and has remained incredibly stubborn since then, vacillating between 58 and 59% ever since (it sits at 59% in June).

An aging, retiring workforce is part of the explanation, economists warn — but so is long-term unemployment. During the recession, the six-months-or-longer unemployed rate peaked at 48% in April 2010 — one out of every two folks who lost their job then remained out of work for at least six months. For context, during the peak of the 1980s recession, in May 1983, the rate was 27%.

The Credit.com American Dream survey took a slightly longer view of this phenomenon, and the data are consistent with government data about long-term unemployed. We asked respondents if they’d been unemployed at any time during the past 36 months. Slightly more than 40% said they had been. Of that group, 28% said they had been unemployed more than once, and 60% said they were out of work for longer than 12 months.

Remarkably, this group’s economic dreams weren’t dampened much by their plight.

Among the unemployed, 43% said the American Dream was still within their grasp, compared to 49% for the general population. Among both groups, 16% said they’d already achieved the American Dream.

The group isn’t any more pessimistic about others, either. Among both groups, only 21% say the Dream is reachable for others, and about one-third of both groups say it’s within reach for Millennials (32% for unemployed vs. 33% for employed).

The group isn’t any more pessimistic about others, either. Among both groups, only 21% say the Dream is reachable for others, and about one-third of both groups say it’s within reach for Millennials (32% for unemployed vs. 33% for employed).

The unemployed and employed define the American Dream almost exactly the same way — retiring financially secure (34% vs. 36%), being debt-free (24% vs. 25%) or owning a home (18% vs. 17%).

Is It Really Within Reach?

Where there exists some optimism among the long-term unemployed respondents for their own future, however, the reality is troubling — at least for the time being. The challenges faced by the long-term unemployed were explored in a paper published in 2012 by Rand Ghayad, a visiting scholar at the Boston Fed. Ghayad sent out thousands of fake resumes and controlled for all factors to see if those who’d been without a job for six months face discrimination in hiring. They did. Companies preferred workers with no related experience to long-term unemployed with directly relevant job experience. In other words, even if you are the most qualified applicant, you probably won’t get the job if you’ve been out of work for more than six months.

This kind of unemployment has potential long-term impacts for the economy — we might already be living through them. Generally, there should be a tidy relationship between job openings and the employment/unemployment rate, something known as the Beveridge Curve. That makes sense — job openings should soak up unemployed people. When the Beveridge Curve breaks, as it did in the 1980s, many folks assume there is a skill gap. Unemployed folks don’t have the skills to fill open positions. That theory makes sense when you see a big economic shift, such as from blue-collar to white collar jobs. Then, unemployment is a structural problem that might be solved by sending workers to school. Such a shift shows up in the data; there’s a flood of folks with blue collar experience who can’t get job interviews, using the example above.

This is why Ghayad’s research was troubling. In his data, even controlling for all sorts of experience, the six-months-unemployed-and-you’re-out factor remained in effect. In other words, this structural problem can’t be solved by taking a few classes.

It *might* be solved by human resources departments realizing that long-term unemployment is nothing special. In fact, it’s perfectly normal. But as long as the employment rate remains stubbornly low, and the number of resumes per job application remains high (250 per job, according to one estimate), HR departments will keep looking for ways to quickly screen the pile. Chucking the long-term unemployed is an easy, perfectly legal way to do that.

For now, however, it seems the long-term unemployed haven’t chucked their American Dream. They might be right in the end. The number of job openings in the U.S. economy climbed in June, and while the Beveridge Curve remains out of whack, some economists see signs of a return to normal. That would meant the Great Recession, while a creating deep wound, is starting to heal – and with it, so is the American Dream.

More on Credit Reports and Credit Scores:

- How to Get Your Free Annual Credit Report

- How Do I Dispute an Error on My Credit Report?

- How Credit Impacts Your Day-to-Day Life

Image: Wavebreakmedia Ltd

You Might Also Like

Find out if your rent and utility payments are reported on your c... Read More

April 11, 2023

Uncategorized

Becoming an authorized user is a common tip for individuals tryin... Read More

September 13, 2021

Uncategorized

Long-term unemployment can really hurt—and not just financially... Read More

August 4, 2021

Uncategorized