What Is a Credit Report?

A credit report is a document that gathers data about your financial history. It's not the same thing as a credit score, which is a three-digit number meant to reflect the likelihood that you will pay your debts as agreed. Credit scores are based on the information included on your credit reports.

Your credit reports are maintained by the credit bureaus—there are many, but three main bureaus are Experian, Equifax, and TransUnion. Credit information is reported to the credit bureaus by your lenders. They aren’t required to report information to the bureaus, which means that the credit reports created by the bureaus will be slightly different from each other.

In general, credit reports include information about loans and other debts you've had in the recent past—around the last seven to ten years. This will include open and closed accounts and whether your payments are made on time or if you have defaulted on any accounts. Credit reports also include information about where you live and work as well as public records such as bankruptcies.

Who Can See My Credit Report?

Anyone who you give permission to can see your credit report. That includes creditors, employers, landlords, and insurance agencies that you allow to check your credit to evaluate you for an offer, service, or job. Government agencies, creditors, and others may be able to see the information in your credit file without your permission for other reasons.

For example, a business may be able to do a “soft” pull of your report to determine whether you’re eligible for a preapproved offer. When you get targeted credit card offers in the mail, those are likely the result of a soft credit pull by that lender. Beyond soft inquiries, entities may be able to view your credit report without your permission in a few specific situations, like child support determinations or in response to court orders or grand jury subpoenas.

The “inquiries” section of your credit report will show you who has viewed your credit report and when, so you can ensure no one is reviewing your personal information without your permission.

Why Is My Credit Report Important?

The information in your credit file is used to calculate your credit score. And that score is often a determining factor in whether or not you're approved for loans, credit cards, and other funds. Your score also plays a role in interest rates, which can impact how much that credit costs.

In some cases, your credit score can impact other areas of your life, including your employment eligibility at certain jobs, whether you have to put down a deposit for utility services, or whether are able to rent an apartment. If the information in your credit report is inaccurate, you may not be qualifying for the loans, rates, and opportunities that you deserve.

How Do I Get My Credit Reports?

You can view your credit report in a number of ways. Remember that you have multiple credit reports that may be different from each other, and you should review each one regularly to ensure their accuracy.

AnnualCreditReport.com

You can get one free credit report per year from each of the three main bureaus at AnnualCreditReport.com. This does not include your credit score, though it does allow you to see your full credit report. The bureaus are offering free weekly reports through April 2022 due to effects of coronavirus.

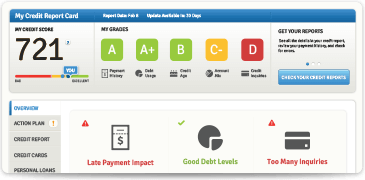

Credit.com’s Credit Report Card

The free Credit Report Card from Credit.com offers a quick and helpful overview to your credit. You’ll see your Experian VantageScore 3.0 and a letter grade for each of the five factors that influence your credit score.

ExtraCredit

ExtraCredit offers in-depth insights into your credit reports from each of the three credit bureaus, as well as 28 of your FICO scores based on those credit reports. Seeing your reports and your scores together in this way can help you better understand the factors in your credit profile that may be negatively affecting your scores.

How to Read My Credit Reports

Your credit report is broken up into sections: personal information, account information, inquiries, and public record information. Each bureau will display this information differently, but the breakdown should be more or less the same.

Personal Information

This section includes your name, places you've lived and worked, your Social Security number, and other information that might help identify you. Scan this section to make sure it's all correct. If there are wrong addresses or variations of your name that you don’t recognize, your file could be getting mixed up with someone else’s—or it could be a sign of identity theft.

- Name and other names you’ve gone by

- Report number

- Social Security number

- Birth date

- Phone number

- Current and previous addresses

- Employment data

Account Information

Every credit account that has been reported to the bureau over the past seven to ten years will also be listed on your report. Each one is identified by a name and account number as well as other detailed information about the account’s history. Review the information carefully to ensure its accuracy.

- Lender name and account number

- Date the account was opened and closed (if applicable)

- Type of account (installment or revolving account)

- Ownership (individual, joint, authorized user)

- Original and current balance

- Highest balance and/or credit limit

- Monthly payment amount

- Payment history

- Current status (paid as agreed, 30 days late, etc.)

These accounts may be organized based on whether they are considered potentially negative or are accounts in good standing. Review the whole document to ensure you are looking at all of the accounts listed on your report.

If you don’t recognize the names of the companies found here, you’ll want to look into those. The name of the business reporting credit may be different from the name of the business you think you’re dealing with (your airline rewards credit card, for example, will likely appear under the issuer’s name, rather than the airline’s name). But this could also be an indication of fraud or identity theft. Full contact information for each company should be listed on your credit report so that you can contact them directly. If not, ask the bureau for that information.

Inquiries

The inquiries or “credit history requests” section shows all the times someone accessed your credit report and why. Hard inquiries are visible to anyone checking your report. These occur when someone checks your report for the purpose of evaluating you for credit. Soft inquiries are only visible to you—these occur when people see your report for other reasons.

Public Records

Certain types of public records can be listed on your report. This includes bankruptcies and certain types of collections accounts.

Personal Statement

If you have disputed something or placed a fraud alert on your report, you may also see a section with a personal statement.

Review Your Reports Regularly

When you review your credit report, look closely at each section. Make sure everything looks accurate. If you see anything that's not correct—especially negative items—you can request that the credit bureau look into the matter and correct the error if appropriate.

Important Facts about Credit Reports

- The credit bureaus don't judge your report or the information in it. The report is simply a compilation of information provided to the bureau. Lenders look at this information to decide whether the information is "good" or "bad" when they evaluate you for credit.

- Reports change constantly. Businesses are constantly reporting information about payments and accounts. If you check your report today, the information you see is a reflection of what's in the bureau's database at the time. That can change tomorrow.

- The three credit bureaus don't share information with each other. That can mean that the information in your various credit files is slightly different because lenders and others are under no obligation to report to all of them—or even any of them.

- You have a legal right to a credit report that is free of errors. That right is stated in the Fair Credit Reporting Act.

- If you find a mistake on your credit report, you can ask the bureau to investigate it. By law, the bureau must launch an investigation in a timely manner. If the entity reporting that information can't back it up with documentation, the credit bureau has to remove or correct it. You can work with a credit repair firm to help you with this process if you’d like.

- You're entitled to one free credit report from each bureau every 12 months. In some cases, you may be entitled to a credit report if you were denied credit because of information in your file. In such cases, you should receive a letter from the lender letting you know you were denied because of that information and which bureau it came from. You can use that letter to request a copy of your report from the bureau in question.

Credit Report FAQs

How do you check your credit score for free?

You can get a free credit score via the Credit Report Card from Credit.com. There are other products that provide free informational credit scores as well. It's important to note that there are numerous credit scoring models—your free credit score from Credit.com is your Experian VantageScore 3.0. While your informational score can help you understand how you're doing with credit, it is unlikely to be exactly the same as a score a lender pulls at any given time.

How many credit reports can you get per year?

You can get one free detailed credit report from each major credit bureau for free each year. The bureaus are allowing you to request your reports weekly through April 2022. If you pay for a credit monitoring service, you can often gain unlimited access to the information in your credit reports. You can also get updated information via the Credit Report Card every 14 days.

Does checking your credit report hurt your credit score?

If you check your own credit, it's considered a soft inquiry. Soft inquiries do not impact your credit score. This is different from a hard inquiry, which occurs when a lender checks your credit when you apply for a loan or credit card. Hard inquiries can have a small impact on your score.

What is the difference between your credit report and the Credit Report Card?

The Credit Report Card is a product offered by Credit.com. It provides information about your credit report and breaks it down into five areas that most impact your score so you can see how you're doing with each. You can get your full credit reports from AnnualCreditReport.com for free or with a paid subscription through ExtraCredit.

Does your credit score come with your credit report?

Your score doesn't automatically come with your credit report. You’ll need to request that information separately or use a service like the Credit Report Card or ExtraCredit.

Is it really free?

Yes, when you request your credit report from AnnualCreditReport.com, it's really free. It's also free to sign up for the Credit Report Card.

Is it accurate?

The information in your credit report is constantly changing, and there are three bureaus with potentially different information. So, while Credit Report Card is accurate, it's only as accurate as the information in your credit report at the time it's pulled.

Is it safe?

Requesting your credit report or signing up for reputable services such as the Credit Report Card or ExtraCredit is safe. In fact, by ensuring you know what's on your credit report, you can help safeguard your identity and credit. Odd items on your report or a sudden change in your score can be signs of identity theft. If you're using a credit monitoring service or getting access to your credit report, you know about those issues early, which can help you stop them before you suffer major losses.

Take Control of Your Credit Profile with Credit.com

Great credit doesn’t happen overnight. Building your credit profile and improving your credit score takes patience and insight into the factors that matter most. To get insight into your own credit profile and start making positive financial choices, sign up for a free trial of ExtraCredit today!