These days, many people receive their wages by direct deposit rather than via a paper check. Direct deposit is convenient—but you should still check your stub to make sure your deductions are correct. If you’ve been wondering how to read a pay stub, you’re in the right place. Let’s go ahead and unpack your paycheck—and untangle a few acronyms along the way.

What Will a Pay Stub Tell You?

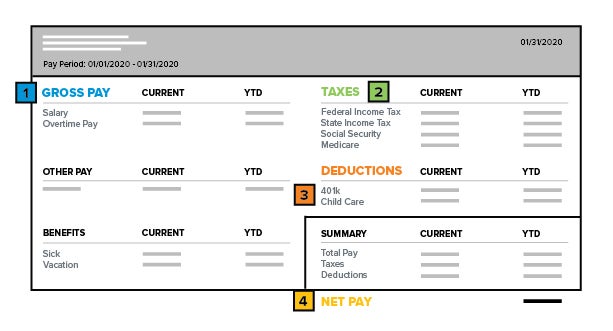

Your pay stub contains a lot of information. At a glance, you’ll see your gross pay, your net pay, your state and federal taxes and any other deductions you pay—including health insurance premiums and pension contributions.

1. Gross Pay

Your gross pay is the total amount of money you earn in any given pay period—before taxes and other deductions are taken out. Let’s take a closer look:

You might also see your year-to-date gross pay in this section. If so, it’ll probably be marked with “YTD.”

2. Taxes

Taxes vary from state to state, so the tax section can get a little complex. Some local municipalities impose income taxes on top of state and federal taxes. Nine states, including Florida, Alaska, Tennessee and Texas, don’t have individual income taxes—but residents do still pay federal income taxes. Most check stubs show taxes for that pay period, plus year-to-date amounts.

Federal

Federal income taxes apply no matter where you live. Your employer uses several pieces of information to calculate your estimated federal tax liability:

Employers send federal tax withholdings straight to the federal government. If you want a bigger income tax refund, reduce the number of dependents you claim. If you’d prefer more money per paycheck, claim a greater number of dependents. Keep in mind—if you underpay federal taxes, you’ll owe money to the IRS at the end of the year.

State

State taxes work a lot like federal taxes. Employers use several pieces of information to come up with your estimated state tax liability, and they send tax withholdings straight to the state. Once again, you’ll either owe money or receive a refund at the end of the year. These nine states currently don’t charge residents any income tax:

New Hampshire does still tax investment earnings, so you may still have to file a state return if you receive interest, dividends or capital gains.

FICA

Federal Insurance Contributions Act (FICA) taxes include Social Security and Medicare payments. Take a look at your pay stub—any amount labeled as FICA is a contribution to those two federal programs. Some check stubs break out Social Security and Medicare payments to show you how much you’re contributing to each fund.

Here’s the lowdown on FICA:

- Social Security—6.2%. You pay 6.2% of your income to Social Security (SS). Your employer contributes another 6.2% for a total of 12.4%. If you’re self-employed, you have to pay both the employee and the employer SS contributions—but you pay based on net, rather than gross income.

- Medicare—1.45%. Medicare payments amount to 1.45% of your income. Your employer contributes a further 1.45% for a total of 2.9%. Again, if you’re self-employed, you pay both the employer and the employee contributions on your net income.

3. Deductions

Income taxes and government programs aren’t the only deductions listed on your pay stub. Other deductions include health insurance payments, flexible spending account contributions and retirement plans.

Insurance

If you’ve signed up for employer-sponsored health insurance, dental insurance or life insurance, the premiums you pay will show up as deductions on your pay stub. Businesses with more than 50 employees have to contribute a minimum of 60% of an employee’s health insurance premiums—but according to a survey by the Kaiser Family Foundation, most pay 82% or more.

Insurance premiums are pre-tax deductions—in other words, you don’t pay taxes on them and they reduce your taxable income.

Flexible Spending Accounts

Flexible spending accounts (FSA) let you set aside money to pay medical expenses throughout the year. Again, FSA contributions are pre-tax, so you don’t pay taxes on them and they reduce your taxable income. You’ll notice your FSA account contributions listed on your pay stub.

You can spend FSA dollars on prescription medications, health insurance copayments, deductibles and more. If you don’t spend all your FSA funds by the FSA provider’s deadline—usually January to March of the following year—you lose them.

Health Savings Accounts

If you have a high-deductible health insurance plan, you may be eligible for a health savings account (HSA). Like flexible spending accounts, the funds you contribute to your HSA are pre-tax dollars, and you’ll see those amounts on your pay stub.

You can spend HSA funds on hospital bills, dental or vision care, prescription medications, deductibles and many other medical expenses. Unlike FSA funds, HSA funds don’t expire—instead, they accrue in your HSA account and remain there until you spend them.

Retirement Savings Plans

Numerous types of retirement savings options exist, including 401(k) and IRA plans. Like other deductions, retirement account contributions are pre-tax dollars. If you have a retirement account, a proportion of your pre-tax earnings will go into your 401(k) or IRA every pay period. You’ll see the amount listed on your pay stub.

4. Net Pay

Your net pay is the amount of money you actually receive in your bank account. In a nutshell, it’s your gross pay minus allof the taxes and other deductions you pay. You can track your net pay and use it to create an affordable budget—including spending money, debt payments, savings and more.

What Do Pay Stub Deduction Codes Mean?

Are acronyms getting you down? Here are some of the most common pay stub deduction codes, demystified:

- FED, FIT or FITW: Federal income taxes

- STATE, SIT or SITW: State income taxes

- OASDI, FICA, SS or SOCSEC: Social Security payments

- MED: Medicare taxes

- FSA or HAS: Flexible spending account or health savings account

- 401(k) or IRA: Your retirement plan

- LV or LEVY: Tax levies

- CHSPPRT: Child support

- GARN: Wage garnishment

Why Keep Track of Your Deductions?

Your employer’s tax estimates are just that—estimates. It’s up to youto keep track of deductions to make sure they’re accurate. If you find deduction or payment errors, you need to report them and fix them as soon as you can to ensure you don’t end up with a big tax bill or too little money in your FSA.

Make sure all the information on your current pay stub matches your most recent W-2—if you move, update your address. Spot check your pay regularly to make sure you’re being paid properly for hourly work and overtime. If you see a mistake, contact your HR department.

Save While You Earn

It’s important to learn how to read a pay stub. Pay stubs provide a helpful breakdown of gross pay, net pay and all the deductions in between. To keep errors to a minimum, check your pay stub regularly and report mistakes to your employer.

Ready to save for a financially stable future? Understanding your paycheck can help—and many people find high-yield savings accounts useful and convenient. You can have part of your paycheck deposited directly into your savings account, which can make saving easier.