It's Financial Literacy Month: Here's What Your Credit Score Wants You to Know

Learn how to improve your credit score with essential tips on payment history, credit utilization, and more this Financial Literacy Month.

Published February 22, 2021

This post originally appeared on Finder.com.

Americans fell victim to a reported $1.9 billion in fraud losses in 2019, with more than 270,000 cases reported specifically due to credit card fraud.

American adults have seemingly had a consistent amount of credit card fraud victimization, according to a January 2021 survey from Finder. An estimated 15% of American adults who own at least one credit card — roughly 37.2 million Americans — report they’ve been on the wrong end of fraudulent transactions at least once, an increase of 4.4%. Even more alarming is how much criminals made off with through this fraud.

According to the Federal Trade Commission, Americans reported losing an estimated $1.9 billion to fraud in 2019. Over 270,000 of the 1.7 million cases reported were due to credit card fraud, a 72.35% increase in credit card fraud cases from the previous year.

A gender fraud gap exists in America, with almost 21.8 million men (18%) admitting to falling victim to credit card fraud at least once in their life compared to nearly 15.3 million women (11%).

Finder reveals that 11.4 million (19%) in Gen X admit to falling victim to credit card fraud. Following Gen X is 10.8 million millennials (16.3%) and 9.7 million baby boomers (12.4%) who report the same. Only 11.4% of Gen Z (3.0 million) say they’ve fallen prey to credit card fraud (2.3 million), followed by 9.14% of the silent generation.

| Generation | % victims of credit card fraud | Number of credit card fraud victims |

| Gen Z | 11.41% | 2,993,971 |

| Millennials | 16.34% | 10,835,323 |

| Gen X | 19.23% | 11,405,603 |

| Baby boomers | 12.36% | 9,694,763 |

| Silent generation | 9.14% | 2,281,121 |

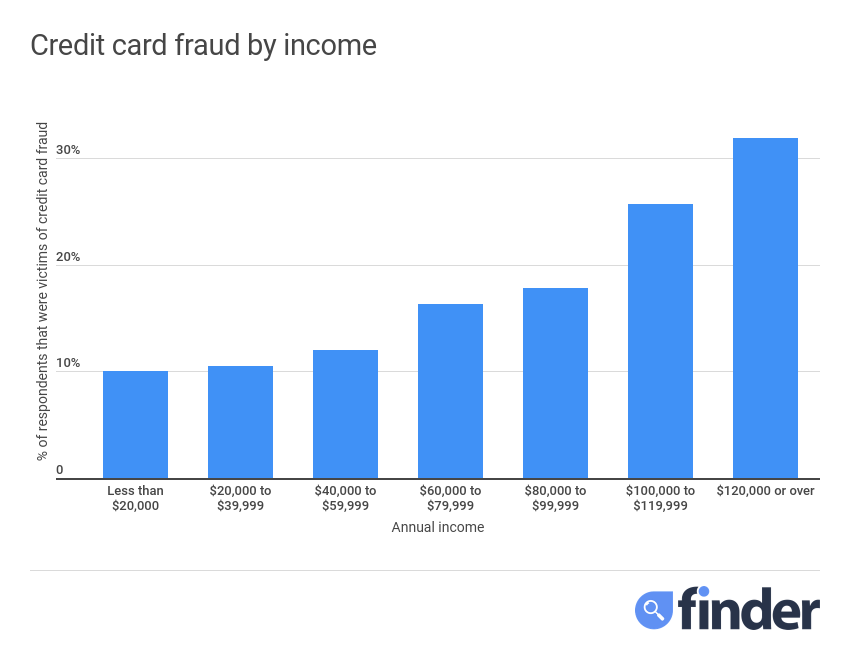

As income levels increase, the likelihood of becoming a victim of credit card fraud increases along with income levels. According to our survey, 10.1% of adults with annual incomes of less than $20,000 say they have been a victim of credit card fraud. In comparison, 31.9% of adults who earn more than $120,000 annually say the same. It suggests that adults with the highest income level in our survey are 3.17 times more likely to become a victim of credit card fraud than adults in the lowest income level.

| Annual income | % victims of credit card fraud | Number of credit card fraud victims |

| Less than $20,000 | 10.07% | 6,273,082 |

| $20,000 to $39,999 | 10.47% | 6,415,652 |

| $40,000 to $59,999 | 12.05% | 5,275,092 |

| $60,000 to $79,999 | 16.31% | 5,417,662 |

| $80,000 to $99,999 | 17.81% | 3,706,821 |

| $100,000 to $119,999 | 25.68% | 2,708,831 |

| $120,000 or over | 31.90% | 7,413,642 |

Given how fast the world turns, consumers need to stay on top of who’s charging us and for what. Fortunately, we can assume that banks and other financial institutions are more vigilant than ever about monitoring fraud: 60% of Americans surveyed learned their accounts had been compromised after their bank reached out directly.

Although the most common way credit card victims are notified about fraud is by phone call (37%), 15% say they found out through an email alert from their bank, and 8% found out through a text notification from their bank. Another 6% were clued into a problem at the register, where they saw “declined” after swiping, while 30% discovered a fraudulent charge after diligently checking their statements.

We can analyze these insights in two ways:

Either way, we all need to do more to protect our finances both on and offline.

| How did you find out your credit card was compromised? | % of credit card fraud victims | Number of credit card victims |

| A phone call from my bank | 36.78% | 13,686,724 |

| A email from my bank | 14.94% | 5,560,232 |

| A text from my bank | 8.43% | 3,136,541 |

| I found out myself by checking my statements and finding fraudulent charges | 29.50% | 10,977,893 |

| My credit card was declined when I tried to use it | 6.13% | 2,281,121 |

| Other | 4.21% | 1,568,270 |

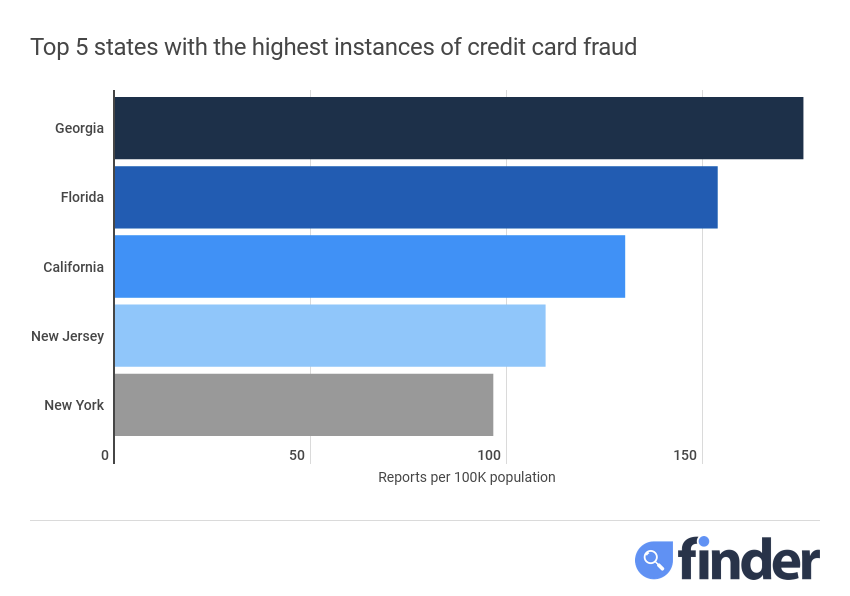

| Rank | State | Reports per 100K Population | # of Reports |

| 1 | Georgia | 175.77 | 18,662 |

| 2 | Florida | 153.88 | 33,050 |

| 3 | California | 130.26 | 51,468 |

| 4 | New Jersey | 109.94 | 9,765 |

| 5 | New York | 96.59 | 18,790 |

The best way to minimize the chance of becoming a victim of fraud is by keeping your sensitive personal and financial information safe from would-be criminals.

Phishing and other cybercrime are easy ways to part you from your money. Online scammers are becoming only more sophisticated, using increasingly elaborate schemes to trick you into revealing your personal and financial details. Learn how to protect your credit card information when shopping online, starting with checking the site you’re on is secure.

Phishing scams and malware. These scams typically involve email that looks like it’s from a reputable company — but is in fact designed to intercept your credit card number or password. Clicking, sharing or opening what the fraudsters are pedaling can unleash viruses, trackers or other malware on your device.

What can you do? Do not click links in an email, verify your personal data or download an attachment without first confirming the request is from a legitimate source. Know that no lawful bank, retailer or provider will ask you to confirm personal information online. If in doubt, call the institution it appears to be from to confirm the communication.

Online shopping. Shopping online is part and parcel of living in the 21st century. But just as you wouldn’t swipe your card at a sketchy storefront, don’t enter your details into an unsecure site. Avoid falling prey to scammers looking to leverage the anonymity of the Internet to rip you off. IRL applies here too: If it sounds too good to be true, it just might be.

What can you do? Be wary of any deal that asks for upfront deposits or specific payment methods, like wire transfers or money orders. Confirm that you’re on an encrypted site by looking for “https” at the start of the URL. And search the Internet to see what others say about the site.

Take extra precautions with a credit card that offers customer protection, like Verified by Visa, Mastercard SecureCode and American Express Safekey. Simply enter a one-time SMS or email code with each purchase online.

Keep an eye out for traditional fraud in the analog world.

Dumpster diving. Yep, people may be digging through your garbage to find more than recyclable cans and bottles. Rather, they’re after details you toss away that can help them steal your identity.

What can you do? Never throw out documents that contain your personal information without making some effort to tear them up or run them through a shredder. Better yet, cancel as many paper bills or statements as you can, opting for e-statements instead.

Discard your credit card safely by demagnetizing the strip or shredding the card horizontally.

Stolen or lost cards. There’s no easier way for a thief to make fraudulent charges than with your actual card in their possession.

What can you do? Whether you think you’ve left your card behind at the bar or your wallet’s gone missing, act fast. Call the last location you remember having it to ask if somebody’s found it. If not, contact your bank to cancel your card.

Beware the skimmers. These tricky little card readers can be hard to spot, but scammers have attached them to ATMs, gas pumps and other devices requiring your card for payments or cash.

What can you do? Before inserting your card into a reader, jiggle or shake it to make sure it’s firmly attached. Learn how skimmers work, and if a card reader looks suspect, don’t use it. If you think your info might’ve been skimmed, notify your bank first and then alert the FTC to submit a fraud alert.

Learn more about protecting your identity in our comprehensive guide to identity theft.

Finder’s data is based on an online survey of 1,790 US adults born between 1928 and 2002 commissioned by Finder and conducted by Pureprofile in September 2020. Participants were paid volunteers.

We assume the participants in our survey represent the US population of 254.7 million Americans who are at least 18 years old according to the July 2019 US Census Bureau estimate. This assumption is made at the 95% confidence level with a 2.32% margin of error.

The survey asked respondents whether they've experienced credit card fraud in the past 12 months and, if so, how they found out their credit card had been compromised.

We sourced monetary amounts and the number of credit card fraud reports by state from the Federal Trade Commission Data Book for 2019 published in January 2020. To calculate credit card fraud reports per 100K population in each state, we used 2019 Census estimates of each state’s population.

We define generations by birth year according to the Pew Research Center’s generational guidelines:

We define geographical regions according to the divisions of the US Census Bureau.

Sources:

Learn how to improve your credit score with essential tips on payment history, credit utilization, and more this Financial Literacy Month.

Learn how to use your tax refund to improve your credit score with these strategic financial tips. Boost your financial health and achieve your credit goals.

Take control of your financial health and strengthen your money relationship with practical tips to improve your credit score and set financial goals today.