It's Financial Literacy Month: Here's What Your Credit Score Wants You to Know

Learn how to improve your credit score with essential tips on payment history, credit utilization, and more this Financial Literacy Month.

Published May 20, 2019

Is your credit score subprime? Then any unsecured loan that you’re approved for is a high-risk loan. “High risk loans” are loans that pose more risk to a lender that choose to issue credit to someone with a low credit score—considered a “high-risk borrower.” The borrower’s low credit score is the result of a history of making late payments, keeping credit card balances close to their limits, having recently applied for a lot of credit or having a limited credit history.

“A high-risk loan is a subprime loan that is offered to someone with a blemished credit history, according to their credit report,” says Thomas Nitzsche, media relations manager for Clearpoint Credit Counseling. According to Nitzsche, high-risk loans can have double- or even triple-digit interest rates.

High interest rates are how lenders mitigate the risk of making loans to people with bad credit. If you don’t repay the loan, the interest paid on that loan at least makes up for or reduces the lenders’ loss.

Many high-risk unsecured personal loans are available online and are easy to obtain. But if you have poor credit and pursue a loan, read the terms and paperwork closely so you know what you’re getting into.

High-risk loans are unsecured loans. An unsecured loan is one that doesn’t require a guarantee, or any collateral to give security to the lender if the borrower defaults on the loan, such as a valuable possession, asset, property, car or home. Since the borrower doesn’t have to put up collateral, the loan is unsecured. On the flip side, secured loans—like a mortgage—require a guarantee.

In order to balance the lender's risk, unsecured loans charge a high interest rate. If the borrower pays the loan as agreed, his/her credit score should go up. But if the borrower fails to make payments on time or defaults on the loan, the borrower can wind up in debt and with a damaged credit score.

You’re a high-risk borrower if you have a high-risk credit score. Your credit score is a three-digit number that indicates how likely it is that you pay a loan back and make timely payments. Loans include a credit card, car loan, personal loan, mortgage, etc. If you have low credit score—one below 620—lenders consider you a high-risk borrower.

If you have a pattern of the following, you might be a high-risk borrower and qualify for a high-risk loan:

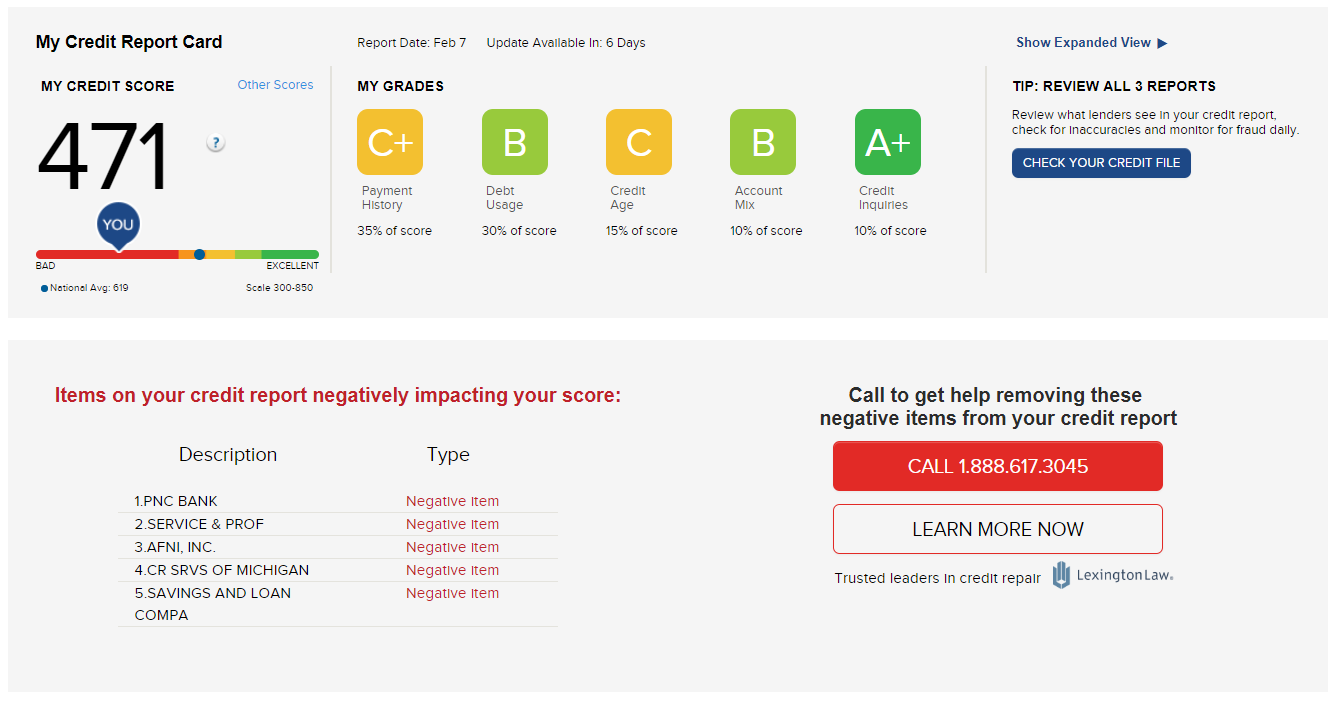

To see if you’re a high-risk borrower, you can get your Experian credit score for free on Credit.com. Your score includes a free credit report card. Your report card tracks the five key factors that make up your credit score—payment history, debt usage, credit age, account mix and inquiries. Plus, you can get advice on how to improve your credit by improving each of the five areas.

If you have a low credit score of around 500, you have limited options for loans. You might qualify for an unsecured high-risk loan, but it’ll have a low loan amount and a high interest rate.

There are a few steps that you can take to get a loan with bad credit:

There are loans that you can qualify for if you have low credit. Here are a few:

High-risk loans can be useful for a variety of reasons, such as paying off other debts or rebuilding your credit. If you make all of your payments on time, keep debt-levels low and keep a close eye on your credit, you can improve your credit score.

If you've made financial mistakes in the past, you can slowly improve your credit score by starting with a lender who’s willing to take a chance on your credit. Take a look at the following table to find the right personal loan for you:

Consumers often look to personal loans as a way to consolidate credit card debt and to save money while doing so. But that’s not always the right solution, especially if have bad credit and are facing a high-risk loan with high interest.

Nitzsche said it’s extremely common for lenders to deny consolidation loan applications, as applicants tend to have a high debt-to-income ratio and low credit scores.

If you do get approved for a personal loan despite your bad credit, the terms that come with high-risk loans may actually cancel out the benefits of a consolidation loan.

For example, if the interest rate on your personal loan is higher than the average annual percentage rate (APR) across the credit cards you’re trying to pay off, you won’t save money by consolidating your credit card debt.

Another benefit of using a personal loan to consolidate credit card debt is that you’re given a firm structure for repaying the debt. Say the loan term is five years and has a fixed interest rate, you have to repay the loan within five years and have the same loan payment every month. That specific timeline can be helpful, given how long credit card debt can drag on when you only make minimum payments.

Still, you may have better options.

If you can’t qualify for a consolidation loan with an interest rate lower than your credit card APRs, you may just want to focus on tackling the cards themselves

If you can no longer afford your credit cards’ minimum payments, that’s a different story.

You can negotiate with the credit card issuer for payment terms and put those terms in a debt settlement letter. “…a creditor financial hardship [debt settlement letter] plan can lower the interest rate and make the payment more affordable. Because credit cards report monthly payment history, sticking to these modified payment terms can also help improve credit,” Nitzsche said.

Another option is a debt management plan (DMP) through a nonprofit credit counselor that reduces your interest rates and consolidates all your monthly debt payments into one.

A DMP can negatively affect your credit because you generally have to close your accounts when you enter the plan and the plan appears on your credit reports.

Every solution has its pros and cons, so take the time to research your options and ask questions about how the option will affect your credit and overall financial health.

The first step to a loan is know your credit score. Once you have that in hand, you can apply for the best personal loan option for you if that’s the path you choose to take.

Learn how to improve your credit score with essential tips on payment history, credit utilization, and more this Financial Literacy Month.

Learn how to use your tax refund to improve your credit score with these strategic financial tips. Boost your financial health and achieve your credit goals.

Take control of your financial health and strengthen your money relationship with practical tips to improve your credit score and set financial goals today.