Your credit age accounts for 15% of your credit score. Apply for credit early, and keep your accounts open as long as you can.

Length or age of credit history is how long you’ve had credit lines in your name. It accounts for about 15% of your credit score, and there’s not much you can do except be patient to help this factor improve. Find out more about credit age and what it means for your score below.

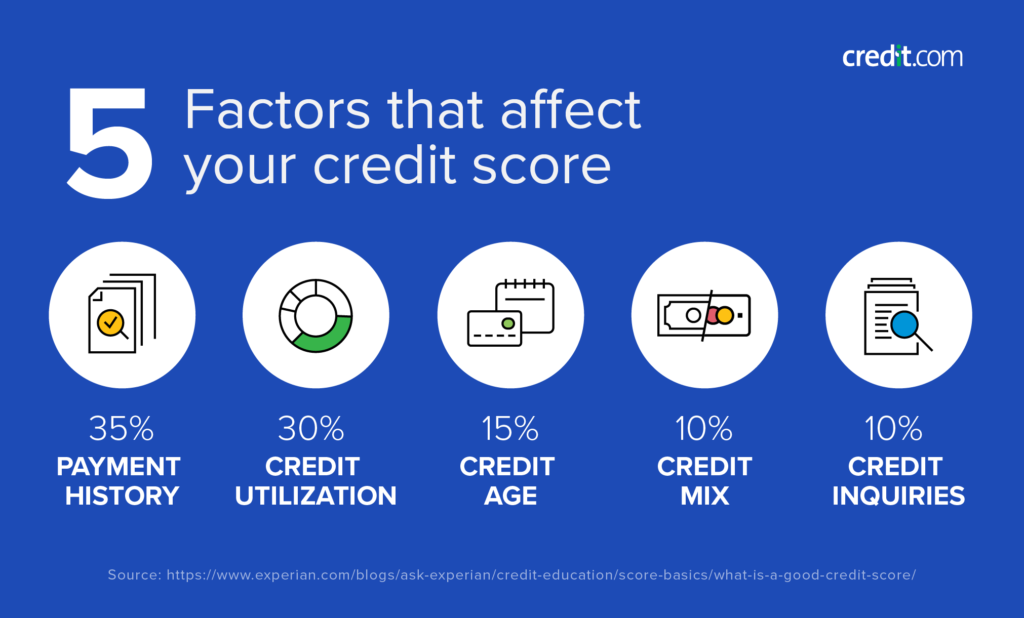

In this series, we’re covering five factors that impact your credit score:

Payment history, which refers to whether you pay your debts as agreed and on time. This makes up around 35% of your score.

Credit utilization, which is the amount of debt you owe compared to your available credit. Utilization accounts for roughly 30% of your score.

Credit mix, which refers to the types of credit accounts you have. It’s roughly 10% of your score.

Age of credit, which is how long you’ve had credit. Credit age accounts for around 15% of your score.

Hard inquiries, which occur when you apply for credit. This drives around 10% of your score.

What Does Age of Credit Lines Mean?

Age of credit history addresses the age of the information on your credit reports, not your own age. Obviously, if you’re only 18 years old, you’re unlikely to have a lengthy credit history as you probably just got your first credit card. But you could be 40 years old without much of a credit history, too.

TIP: Want to get a new credit line listed on your account without opening a credit card? Consider signing up for ExtraCredit. You can use the Build It feature to get rent and utility payments reported as new tradelines on your credit profile.

How Is Credit Age Calculated?

In most cases, two numbers are important when discussing credit age. The first is the actual “age” of your credit report. The second is the average age of the accounts on your report.

You don’t have a credit report until something is reported to the credit bureaus. So, the age of the oldest item showing up on the report is the age of your credit report.

Each of the accounts on your credit report has a field called “Date Opened.” This date has been reported to the credit reporting agencies by your creditors. The date opened is supposed to be exactly what it sounds like—the month and year that the account was opened.

The credit scoring models can read this date and determine the age of the account by calculating the number of months and years that the account has been open. This oldest date becomes the age of your credit report.

Note that this doesn’t necessarily mean this is the oldest account you’ve ever had. Accounts can age off credit reports after they’re closed. Your age of credit, then, is calculated based on what is still being reported.

Average Age of Accounts Is Also Important

Another important measurement is the average age of your accounts. This is simply the average age of all of your accounts as measured using the same date opened field. For example, if you have two accounts that are 3 years old and 5 years old, your average age of credit is 4 years.

Your Age of Credit History Can Change

Because items can age off your credit report, credit age can change. Here’s a hypothetical example to help you understand how credit age can change:

You have a closed account that’s 7 years old, plus two open accounts that are 4 and 2 years old.

Your current credit report age is 7 years and your average age of accounts is 4.33 years.

That old, closed account is about to age off your report. That leaves two accounts with ages of 4 and 2 years. You also open a brand-new account that’s got a credit age of 0.

Your credit report age is now 4 years, and your average age of accounts is 2 years.

This is simplified math, but you can see how your age of credit history can change by a lot in a short amount of time. That could cause your credit score to go down a bit, too.

Why Your Credit Age Matters

Generally, a longer credit history is better for your credit score. Consumers with younger credit history tend to be considered riskier borrowers than consumers who have had credit for many years. Without a history of data to show them how you handle your debts, lenders are less likely to be willing to lend you money—especially large amounts like what is required for a mortgage loan.

Lenders want to know how consumers have dealt with credit in the past to determine how likely they are to repay their future debts. The longer your credit history, the more experience you have with credit.

You need to have an account open for six months in order for FICO to calculate your credit scores. VantageScore can calculate a score after just a month or two of an account opening.

Time isn’t something you’re in control of, so what can you do to positively impact age of credit history to strengthen your score? Turns out, there are a few things you can do.

1. Open new credit as soon as possible and manage it well.

Waiting to start building your credit means that your credit age is younger than it has to be. Consider signing up for a credit card when you’re young to start building your credit report and age of credit. Even if you don’t have credit right now, you may still be able to qualify for a secured credit card.

No credit check to apply. Zero credit risk to apply!

Looking to build or rebuild your credit? 2/3 of cardholders receive a 48+ point improvement after making 3 on-time payments

Extend your $200 credit line by getting considered for an unsecured credit line increase after 6 months, no additional deposit required!

Get free monthly access to your FICO score in our mobile application

Build your credit history across 3 major credit reporting agencies: Experian, Equifax, and Transunion

Add to your mobile wallet and make purchases using Apple Pay, Samsung Pay and Google Pay

Fund your card with a low $200 refundable security deposit to get a $200 credit line

Apply in less than 5 minutes with our mobile first application

Choose the due date that fits your schedule with flexible payment dates

Join over 1.2 million cardholders who’ve used OpenSky to build their credit

Card Details +

If you’re a parent, help your child build healthy credit habits now! You can add them as an authorized user to your credit card—just check that it’s one that reports authorized users so they get credit for it!—or help them open and manage their own accounts.

Tip: If you’re paying rent and utilities, you could get those added to your credit report by signing up for ExtraCredit!

2. Don’t close old accounts if you don’t have to.

Closing old accounts means they’ll eventually age off your credit report, which can substantially drop your credit age. Instead, consider keeping credit card accounts open as long as possible—especially if you’re not paying annual fees. You’ll probably need to make small purchases on the cards and pay them off regularly, or the credit card company might close them for inactivity.

However, this tip is one to wield carefully. If you’re struggling with debt or know you may be tempted to run up credit card balances, closing accounts might be in your best interest. Consider your situation carefully to make a decision that’s right for you.

3. Be careful about opening new accounts you don’t need.

New accounts are young accounts. That means they’ll bring down the average age of your credit. Before you apply for credit, always consider the big picture of your financial situation and how a new account might help and hurt you in the long-term.

Age of Credit History

Age of credit history is an important factor in determining your credit score. But it’s not the only factor—and it’s not the most powerful one. For a robust credit profile and a healthy credit score, you need to consider all five factors together. To understand how you’re doing with all five factors, sign up for ExtraCredit today.