The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Information on this website may not be current. This website may contain links to other third-party websites. Such links are only for the convenience of the reader, user or browser; we do not recommend or endorse the contents of any third-party sites. Readers of this website should contact their attorney, accountant or credit counselor to obtain advice with respect to their particular situation. No reader, user, or browser of this site should act or not act on the basis of information on this site. Always seek personal legal, financial or credit advice for your relevant jurisdiction. Only your individual attorney or advisor can provide assurances that the information contained herein – and your interpretation of it – is applicable or appropriate to your particular situation. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, contributors, contributing firms, or their respective employers.

Credit.com receives compensation for the financial products and services advertised on this site if our users apply for and sign up for any of them. Compensation is not a factor in the substantive evaluation of any product.

Maybe you’re paying for an airline miles card, but not flying, or your credit card interest rate is too high, so you’re afraid to use the card at all. About one in five credit card users are carrying the wrong card, according to a J.D. Power study released Thursday.

“More than 20% of customers have a card which has fees or rewards not aligned with their actual purchase habits,” the study found.

Per J.D. Power, most people select a card for its rewards program, yet 20% of customers who have a rewards card would be better off having a card with different rewards or lower interest, because they’re not spending enough to earn rewards to offset their annual fee.

Airline cards, for example, usually charge an annual fee of $75 or more. Although they’re popular with credit card customers, 44% of airline card customers spend less than the $500 per month on the card that’s typically needed to earn enough rewards to balance out the average annual fee; haven’t used the airline benefits accrued in the past 12 months; or they have not redeemed rewards in the past 18 months, the study found.

“As a result, these customers have lower overall satisfaction than do those who have the right card (scores of 768 vs. 800, respectively, on a 1,000-point scale), spend less per month on their card ($1,150 vs. $1,851) and have a higher intent to switch cards (16% vs. 8%),” according to a J.D. Power press release.

Other credit card customers may have been lured by a sweet sign-on incentive, can’t use the rewards, or the card’s fees or rewards programs have changed since they signed onto it, and, as a result, the card has become less attractive.

These customers collectively aren’t dramatically more dissatisfied, but the improper pairing causes them to spend less per month on their primary card ($783 vs. $1,035), or use their card for a smaller share of their total spending habits (37% vs. 45%) and are more likely to switch cards (21% vs. 9%).

Jim Miller, senior director of banking at J.D. Power, says customers need to understand their card’s fee structure and rewards programs, and make sure it best meets their needs. “In many cases, the current provider may have a card that is better suited for you,” Miller said in a press release.

But card issuers also have a responsibility, he said: They should make sure customers are aware of the benefits of their card and how to use them, and should review their customers’ profile and spending history to recommend the right card for them.

If you’re shopping for a new card, it’s best to review your own spending habits and check your credit score. (You can view two of your credit scores for free each month on Credit.com.) Generally speaking, the better your score, the better the card incentives. And perhaps you can try to improve it before applying for a card.

You can also ask yourself which categories you’re likely to spend most on the card (travel, groceries, or gas, for instance) and seek cards that reward you the most for those categories. You’ll also want to consider whether you prefer cards that offer cash back or those that offer airline miles or other benefits, and determine if you’re likely to pay the card’s full balance each month, or carry it forward. If you’re not likely to pay off your card’s debt, you’ll want to choose a card with a lower interest rate.

J.D. Power’s study included responses from 20,206 credit card customers (surveyed from Sept. 2015 through May 2016). It ranked major credit card issuers by examining six factors (in descending order of importance): interaction, credit card terms, billing and payment, rewards, benefits and services, and problem resolution.

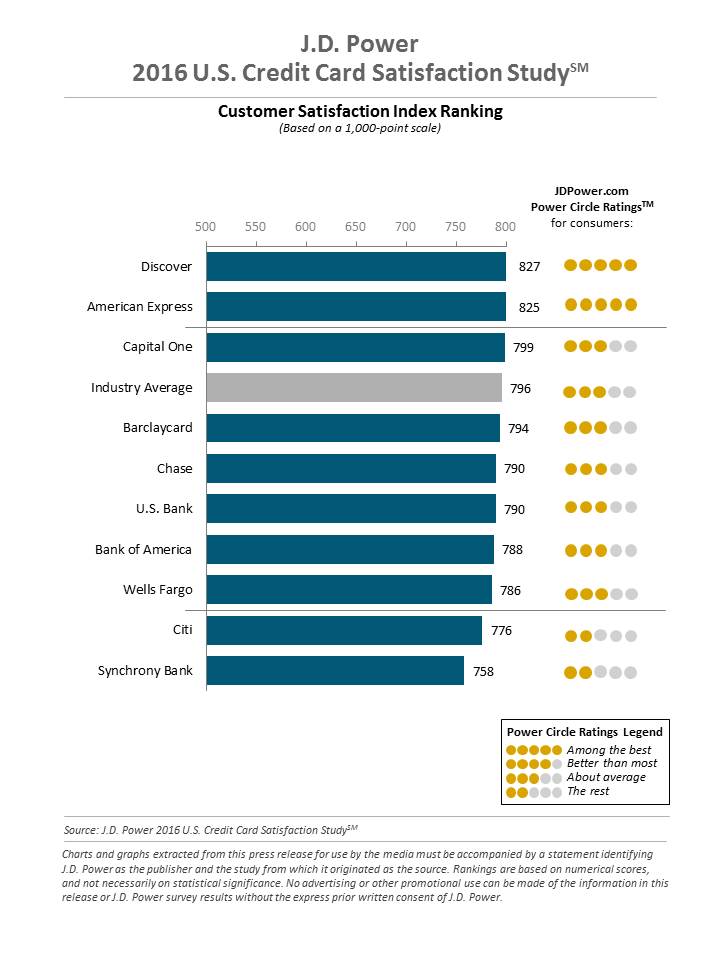

Interestingly, according to the study, customer satisfaction is at an all-time high of 796, surpassing the previous high of 790 in the 2015 study.

Discover, American Express and Capital One had the highest customer satisfaction rating, respectively, while Synchrony Bank and Citi had the lowest scores.

Synchrony Financial issued the following response by email: “Consumers choose to use private label credit cards and Dual Cards because of the distinctive benefits they enjoy with a partner brand and satisfaction with their experience. These programs add value to the shopping experience with uniquely tailored discounts, special savings and services, promotional offers, loyalty rewards, and mobile capabilities aligned with a partner brand.”

Citi spokeswoman Jennifer Bombardier said, “Citi is committed to driving long-term customer engagement and loyalty with our credit cardmembers and continues to make significant progress improving the customer experience, especially in digital channels where more than two-thirds of our customer interactions now take place.”

Image: monkeybusinessimages

April 9, 2024

Credit Cards

October 21, 2020

Credit Cards

August 3, 2020

Credit Cards

{kind=link}