It's Financial Literacy Month: Here's What Your Credit Score Wants You to Know

Learn how to improve your credit score with essential tips on payment history, credit utilization, and more this Financial Literacy Month.

Published May 28, 2025

Paying off your car loan can lower your credit score, but the effects are usually temporary. Paying off debt is generally good for your overall debt-to-income ratio, which compares monthly debt to gross monthly income and is a key metric that lenders use when evaluating you.

Are you thinking about paying off your car loan early? Whether to free up your budget or have the satisfaction of one less monthly bill, many consumers expect doing so will boost their credit score. Surprisingly, the opposite can occur—paying off a car loan early can cause a dip in your credit score.

Fortunately, the impact is usually short-term and may not happen to every consumer. This is because other factors and variables can affect your overall credit score. While paying off debt is a good strategy for improving your credit, doing so for a car loan doesn’t necessarily work the same way, as you may face penalties or reduce your overall savings.

Keep reading to learn more about a car loan’s correlation to your credit score and everything you should know before deciding to pay it off.

In This Piece:

Your credit score can change any time your credit history changes, such as information updates or a newly opened/closed account. Paying off your car loan early will equate to closing an account.

One less account shifts your credit utilization and your credit history age. These changes may lower your credit score, depending on a range of factors.

It can be disappointing to see your score drop if you’ve worked hard to establish good credit, especially if you’re balancing between the poor and fair credit thresholds.

In the next section, we’ll explain how car loans affect credit utilization and other variables that affect your overall score.

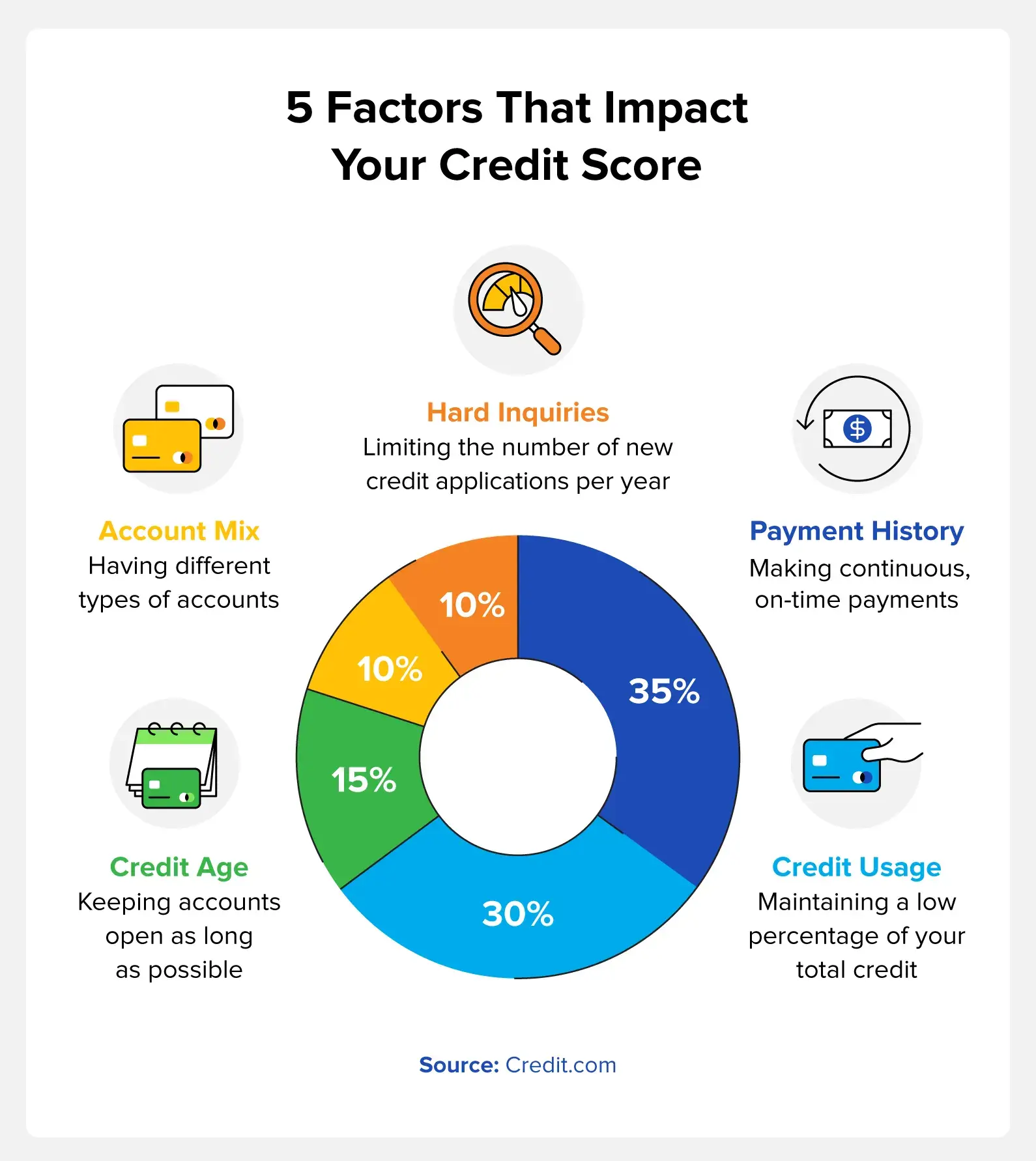

Before choosing any type of loan, it’s important to know how credit works. Your credit score takes several factors into consideration, such as making the payments on time and how long you’ve been doing so. Credit bureaus monitor and compute this data using the following weighted system for each variable:

Sometimes, the trade-off of a temporary credit hit is long-term benefits. For example, if you plan on selling the car, paying off the balance to have the vehicle title beforehand can make the process easier.

Here are other scenarios when paying off your car loan early is typically a good decision:

Depending on your financial situation, closing an installment account means one less bill to worry about, especially when trying to save more cash each month. Paying off a car loan early makes sense if you plan to build up a rainy-day fund or put extra money toward paying off collections and other debt.

Since the credit utilization ratio is a high-weighting factor of your credit score, paying off debt to lower the utilization is essentially a smart move. If your car loan accounts for a large portion of your debt, it makes sense to pay it off. Your score may drop initially when the account closes, but it should bump up your credit score shortly after.

You’ll pay a lot more in interest over the course of a long-term car loan, such as in installments that are six or more years. Additionally, even average-length terms with high interest rates will do the same. If there is no prepayment penalty, paying off your car loan early is a good way to reduce the amount of interest over time.

So, can you pay off a car loan early? Yes, but there are certain situations where keeping debt is beneficial. For example, having a mix of open and active accounts with a strong history of on-time payments is good for your credit score. It also shows creditors you’re responsible for with loans should you apply for another in the future.

The following circumstances are some examples of disadvantages of paying off a car loan early:

While not extremely common, prepayment penalties are fees you’ll owe if you pay off your car loan before the term ends. Some lenders, such as finance companies, include these types of penalties in the car loan as a way to still earn interest if the client decides to pay it off early.

Prepayment penalties will account for a percentage of the car loan amount, which could cost you more than you’d have paid in interest. Make sure you check the loan agreement beforehand for any prepayment penalties. Should you decide to pay off the car loan early, you’ll know what to expect.

Do you have enough money in emergency savings to cover car issues and unpredictable expenses that may arise? If not, you may want to delay paying off that car loan.

A good rule of thumb is to save at least $100 monthly for car maintenance, repairs, and other expenses. You can leverage your car loan term by setting aside money during each payment.

Making timely payments on a low-interest-rate car loan is less expensive than those with high rates or an outstanding credit card balance. In this case, keeping the account open helps maintain a good credit mix and history, which is beneficial for your credit score.

Before implementing any repayment strategy, confirm with your lender that there are no prepayment penalties and that extra payments are applied to the principal. If you’re thinking of paying off your car loan entirely, there are several options:

When considering paying off your car loan early, consider whether the benefits of doing so will outweigh the score drop. Is your score fairly high and in good standing? If so, dropping a few points won’t change much. On the other hand, understand that paying off a car loan early may work against your credit score, depending on the variables above.

Instead, review your financial goals and look into other ways to raise your score. These include keeping a good mix of credit accounts, limiting new inquiries, and making all your other payments on time.

If you still have unanswered questions about whether paying off a car loan early is right for you, here are some answers to frequently asked questions.

While you may pay more in the short term, it can be worth it in the long run to lower your debt-to-income ratio, pay less interest, and save money.

Some lenders may charge a penalty for paying off a car loan early. Review your contract to see if this applies to you before paying off the loan, as it may cost you more than the interest would have.

Paying off a car loan can have a complex effect on your credit. While consistently making on-time payments during the loan term positively impacts your credit history, closing the account by paying it off can sometimes cause a temporary, slight dip in your score, primarily due to changes in your credit mix.

However, in the long term, reducing your overall debt improves your debt-to-income ratio, which is beneficial for your creditworthiness.

Learn how to improve your credit score with essential tips on payment history, credit utilization, and more this Financial Literacy Month.

Learn how to use your tax refund to improve your credit score with these strategic financial tips. Boost your financial health and achieve your credit goals.

Take control of your financial health and strengthen your money relationship with practical tips to improve your credit score and set financial goals today.