This article originally appeared on The Financially Independent Millennial and was republished with permission.

T. Rowe Price conducted a Parents, Kids & Money Survey in 2020 with some unsettling results. For example, just over half of parents surveyed have talked to their children (ages 8-14) about investing. Yet, 41% of parents haven’t discussed or taught any of those investment topics with their kids.

One of the biggest mistakes parents make today when trying to instill financial literacy into their children is trying to run before their kids can crawl. Teaching your kids to invest in individual stocks before they have a basic foundation of some core financial principles is like trying to teach a youth basketball player to dunk before you teach them how to dribble the ball. Dunking is cool, but there is no dunking until they can dribble the ball to the basket to make that dunk.

What other financial topics are there that should be in line ahead of investing? It is debatable, but one would have to consider issues such as: receiving an allowance, the miracle of compound interest, and inflation. There are probably a few more, but those are examples of items you’ll want to make sure your child has a grasp on before you venture down the road of creating the next Warren Buffett.

Steps to Teaching Kids to Invest

Parents often get excited and want to jump right to teaching kids to invest and buy stocks. But, in my opinion, that is not the place to start. Now you would be entirely correct if you said if they opened the door and showed an interest, you’d want to capitalize on teaching them about money. Meaning, skip the other things you should teach them first and jump into what interests them today – AKA the shiny penny syndrome.

But if you take a step back and think about it, will most young adults grow their investment skillset AND have the time/energy to apply these skills properly – in addition to their day job? The answer is likely NO. It would mean they’d have to get their financial investment understanding to the level that they will manage their portfolio during the day alongside their real job. Not only that, they’d need to manage their asset classes (and geographic regions), a diversified portfolio, and remember we’re talking about high quality, individual stocks and/or bonds (not diversified ETFs or mutual funds). It is doubtful they would be able to take this effort on and perform well.

Learning about individual stocks is the sizzle but not a core foundational piece that the beginning investor should spend a lot of time on. I’d implore you to keep it simple out of the gates until such time they can start managing their portfolio from an individual stock perspective.

When it comes to teaching your kids about investing, here are the steps that make sense to follow:

Step 1: Know Your Time Horizon

It’s is going to go right into a conversation of risk and reward. Understanding the time horizon might be the most significant factor in determining how you will ultimately structure your portfolio.

I want you to think about this in terms of your child’s 529 college savings plan (if you have one). Most of you get advised to choose the “aged-based plan.” What we have here is a portfolio that – over 18 years if you start the day they come out of the womb. It starts aggressive and gradually becomes less aggressive as your child gets closer to college. Why? Because the less time between today and when that first check to University needs to get cut, the less time you’ll have to let your portfolio recoup should the market have a pullback (1987, 2000-02, 2008, 2020 – to name a few).

When your child is born, he has an 18 year time horizon until that first check needs to get cut. But when that child turns 15, a three-year time horizon doesn’t quite cut it should the markets pull back in a bad way, thus making you liquidate those funds at a low – the worst time to take money out of your equity portfolio.

Time Horizon Examples

Here are examples of 3 scenarios to let your child tell you how much risk they should take in their investment portfolio based on their time horizon:

- You have $18,000 that you need to use for college next year.

- Or, You won $20,000 from a scratch-off card, and you won’t need the money for quite some time.

- Or, You received $1000 in gift money in 7th grade. You plan on using this money to buy your first car in 12th grade.

Make sure you know how long it will be until you need to use this money to guide the next step.

Read more: 19 Ways to Use Your Tax Refund to Build Wealth

Step 2: Understand Risk versus Reward

By now, most parents have learned the phrase:

Low risk, low return – High risk, high return. But it’s hard for a young adult to understand what that means. They get a general concept, but they have no clue which investment vehicles help you manage that risk.

It’s is typically an excellent time to get a top-down understanding of the many investment products that one will use, in a diversified fashion, to meet their future savings goals.

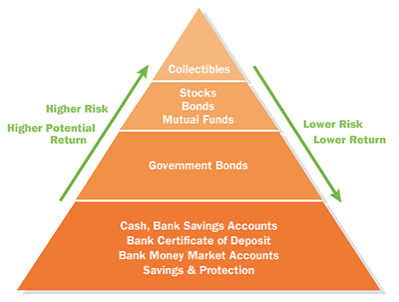

Refer to the Investment Products Pyramid

My favorite visual for teaching risk versus reward of investment products in this pyramid:

The visual above shows the risks/rewards of different types of investments. You can see that investments with lower risks and lower returns are at the bottom. It’s what we would refer to as stable asset classes. Investments that would fall into this foundational level of the investment pyramid include cash, CDs, and money market accounts.

At the top of the chart, you see stocks. And, while stocks historically give us healthy returns over the long run, that comes with a tremendous amount of volatility and risk during the short run. If you take a step back and think about it, investors need volatility and risk to get a higher return. While there is no guarantee that high risk equals high returns, making educated allocations with some of these asset classes is usually necessary to help your money not lose purchasing power and keep up with inflation.

Related read: Tax Preparation Services Near Me

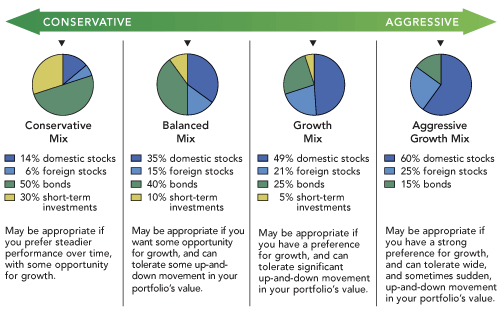

Step 3: Establish Your Diversification

It has been said (cite Fama French Study) that the single biggest determinant of investor returns comes from asset allocation – otherwise known as diversification. Try this chart on for size:

The chart implies a corresponding asset allocation of diversified assets for every level of risk that would align with risk tolerance. It’s an art and not a science. As you have heard legal disclaimers say, “Past performance is not an indication of future results.” That is true, but it’s still what the financial planning and asset management community use to base their portfolio’s diversification. Choosing a mix of stocks, bonds, alternative asset classes, and cash are the major buckets one uses to help construct these portfolios.

The longer time horizon investors have to ride out the ups and downs of the market’s volatility, the more comfortable they can move to the right on the risk scale provided this essential point:

Investors should only take on a risk level to the extent that they won’t get overly emotional when the market goes down (and it will), causing them to take action on abandoning the plan. Diversification only works when investors stay the course in both up AND down markets.

-Thomas Henske

What if my time horizon is short?

If your time horizon is just a couple of years, then do yourself a favor and don’t venture too far out on the risk scale. Better to keep those shorter-term dollars in more stable asset classes so that the money will be there in its entirety when you intend to use it and don’t need to stay in it “until the market comes back.”

One key lesson is that trying to predict returns for various investments is a losing strategy. You can lump into that futility trying to guess how asset classes will perform relative to one another in the short run too.

Step 4: Choose Your Investments

These days, a never-ending list of choices exist in the financial marketplace today. And, picking stocks, bonds, mutual funds, ETFs, or money managers to execute each part of your well-diversified portfolio is not easy to do.

My preference is to stick with index funds as they give broader diversification than just one individual stock. Also, they are low in fees and serve as a great starter kit for kids to understand to fill in their “buckets of diversification.” However, it’s a much longer discussion and probably could be a subject to which we dedicate an entire article.

Step 5: Maintain Your Course

This is not an exercise of setting a portfolio and then forgetting about it. There is a balance between looking at your portfolio too much versus not enough. Just because you set an asset allocation doesn’t mean you never tweak it. It’s important to monitor things from time to time and rebalance every so often. For young kids, I think you make this point and then rebalance twice per year. That way, they make it a habit, and later on, when they are no longer in your home and are in their real life, they can determine the frequency of the monitoring and rebalancing. By the time they get there, computers will have taken over this entire process and monitor and rebalance for them.

Here is an excellent chart for you to use, called the Periodic Table of Investment Returns, to talk about what’s happened historically in the markets, the importance of maintaining the course, and to get them thinking about rebalancing based on what’s happened within the last year in certain asset classes.

Resources to Use When Teaching Kids to Invest

There are so many players in the “teach your kids to invest” world that it would be impossible to cover it all. Instead, let me share a few investment platform solutions that have passed my desk over the years without giving you an opinion about how I feel about them.

Platforms to invest real money

- BusyKid

- Robinhood

- Betterment

- Stockpile

- Beanstock

- Cash App

- FinTron

- Learn & Earn

- M1 Finance

- Schwab Stock Slices

- Public Investing

- SoFi Invest

Virtual stock picking

- Stock Market Game

- Single share purchase (just a framed copy of a single share of stock)

Books

- The Little Red Hen – The gist of this fable: The hen invested the time and effort to turn wheat into bread- sowing the grain, harvesting it, and making dough. It suggests using long-term thinking of investing time/energy.

Final Thoughts

You are just looking for little coachable moments as a parent. Those are opportunities that pop up in the flow of ordinary life, enabling you to teach investing to your child in a natural way to what’s going on around them. That could mean showing them an account statement when it arrives in the mail and teaching them about asset allocation. Or it could be asking at the dinner table, “Did you happen to see what happened in the stock market today?” And when the iron is hot and they show some interest, try to dive deeper into the information above. What happens if they don’t show an interest? Please find a way to get it on topic anyway. While they might not appreciate it now, they certainly will later. And that’s for sure!

You Might Also Like

Kids are expensive. According to the USDA, raising a child can co... Read More

March 5, 2021

Investing

Are you new to investing? Not sure where to start? Investing for ... Read More

November 11, 2020

Investing