The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Information on this website may not be current. This website may contain links to other third-party websites. Such links are only for the convenience of the reader, user or browser; we do not recommend or endorse the contents of any third-party sites. Readers of this website should contact their attorney, accountant or credit counselor to obtain advice with respect to their particular situation. No reader, user, or browser of this site should act or not act on the basis of information on this site. Always seek personal legal, financial or credit advice for your relevant jurisdiction. Only your individual attorney or advisor can provide assurances that the information contained herein – and your interpretation of it – is applicable or appropriate to your particular situation. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, contributors, contributing firms, or their respective employers.

Credit.com receives compensation for the financial products and services advertised on this site if our users apply for and sign up for any of them. Compensation is not a factor in the substantive evaluation of any product.

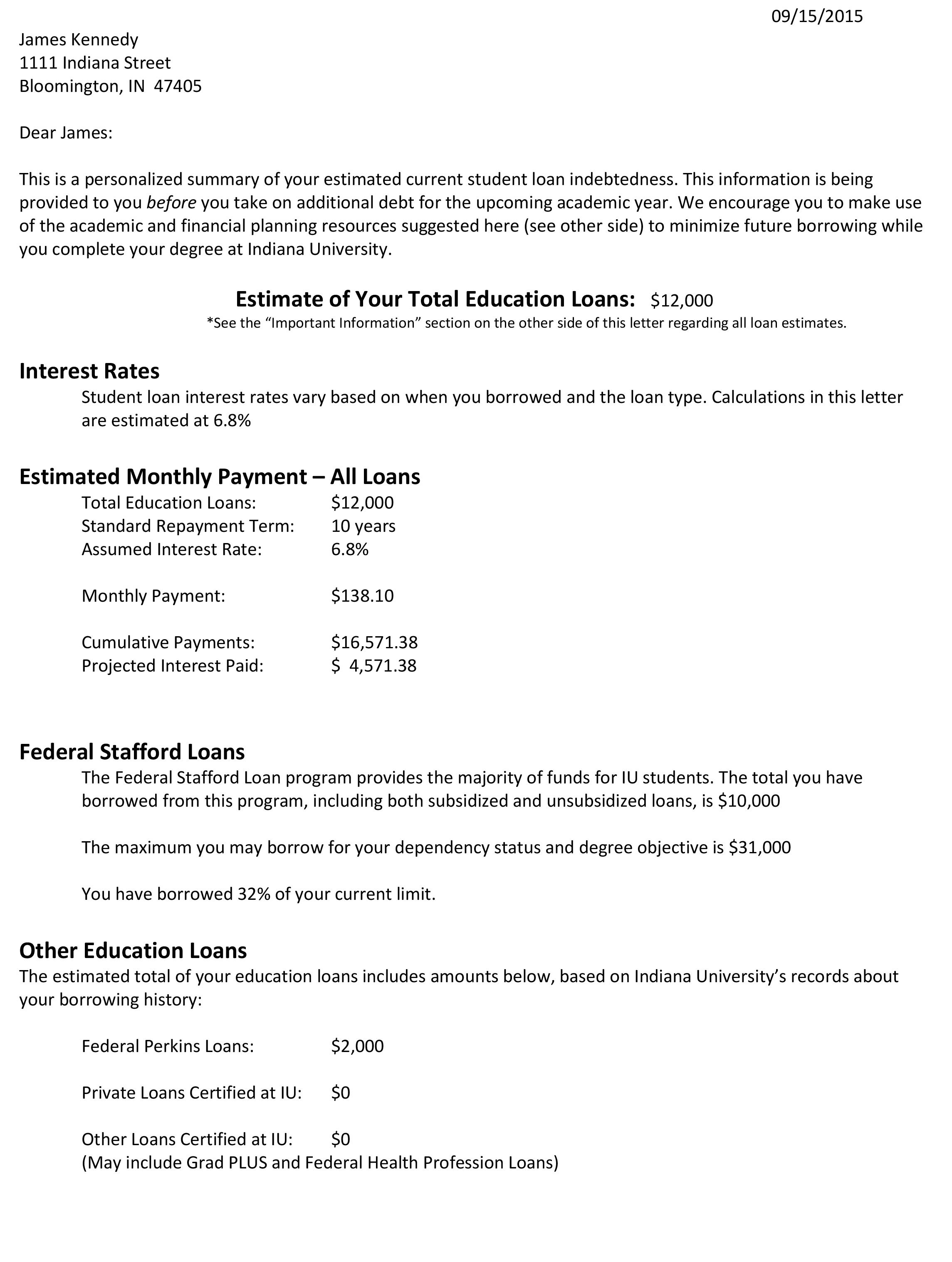

Indiana University is changing the way its students are borrowing to pay for their education.

Back in 2012, the school began sending letters to students, estimating their total student loan debt and future monthly payments. Since then, the university says borrowing by undergraduates has dropped by 18%.

“We want students at every year to understand the debt they have,” says Jim Kennedy, associate vice president for student services and systems. “They get this every year, and they can see where they’re at.”

Back in 2012, after holding a series of focus groups in which students revealed they were confused about how much debt they had, the school decided to launch a series of initiatives designed to empower them financially.

Any of IU’s 110,000 students carrying loans receive the letter (you can see an example letter below), and they also have access to MoneySmarts, a series of podcasts and campus programs that focus on the intersection of college and money. (The most popular, according to Kennedy, is “How Not to Move in With Your Parents.”)

Around each of the school’s seven campuses, signs and posters encourage students to take “15 to finish,” or 15 credits so that they graduate in four years, thereby minimizing their loans. Peer-to-peer counseling and a service that contacts students post-graduation about their repayment options are two other ways the school is trying to secure its graduates’ future.

“We’re just very concerned about students and student loan debt, and our administration is very concerned,” says Kennedy.

He adds, “Anything that colleges can do to raise awareness about student loans is a very positive thing.”

Remember, defaulting on a student or any other type of loan seriously damages your credit score, and because student loans are rarely discharged in bankruptcy, the debt can beat down on you for decades. (You can see how your student loans are currently impacting your credit scores for free on Credit.com.)

There are some options for people who are behind on payments to get back on track, though. To get out of default, you can combine eligible loans with a federal Direct Consolidation Loan, or you can go through the government’s default rehabilitation program. If you make nine consecutive on-time payments (the payments can be extremely low), your account goes back into good standing, and the default is removed from your credit report.

An example of the school’s loan letter is below:

Image: sanjeri

August 26, 2020

Student Loans

August 4, 2020

Student Loans

July 31, 2020

Student Loans

{kind=link}

{kind=link}