The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Information on this website may not be current. This website may contain links to other third-party websites. Such links are only for the convenience of the reader, user or browser; we do not recommend or endorse the contents of any third-party sites. Readers of this website should contact their attorney, accountant or credit counselor to obtain advice with respect to their particular situation. No reader, user, or browser of this site should act or not act on the basis of information on this site. Always seek personal legal, financial or credit advice for your relevant jurisdiction. Only your individual attorney or advisor can provide assurances that the information contained herein – and your interpretation of it – is applicable or appropriate to your particular situation. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, contributors, contributing firms, or their respective employers.

Credit.com receives compensation for the financial products and services advertised on this site if our users apply for and sign up for any of them. Compensation is not a factor in the substantive evaluation of any product.

Nearly 70% of student loan borrowers whose loans have gone into default could have qualified for reduced, income-based repayment plans, thus avoiding the late fees, bad credit and stress that go hand-in-hand with falling behind. That’s why the government wants to raise awareness about the various ways student loans can be repaid.

To that end, the Department of Education and the Consumer Financial Protection Bureau have come up with a free, personalized guide to student loan repayment options called the Payback Playbook.

About 43 million Americans owe student loan debt, with outstanding debt estimated at $1.3 trillion.

“Millions of consumers needlessly fall behind on their student loan debt, despite their right under federal law to a payment they can afford,” said CFPB Director Richard Cordray in a prepared statement.

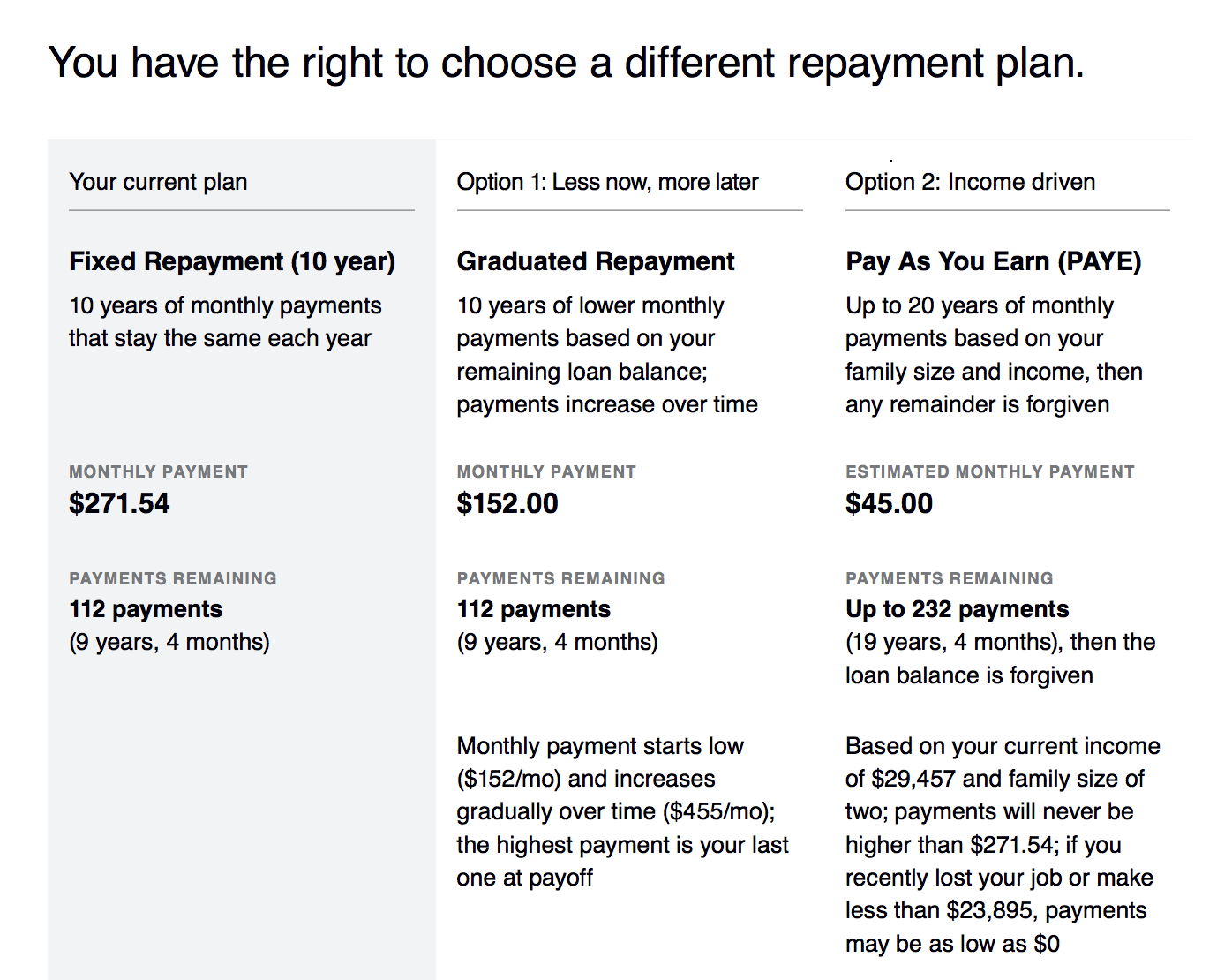

Here’s how the proposed playbooks would work:

Borrowers entering into repayment after graduation would receive the playbook from their servicer, which will hopefully help cut through some of the information clutter by clearly presenting three personalized repayment options.

Struggling borrowers who have missed a payment or are at risk of default will receive a playbook that provides a single option with personalized instructions written in plain language describing how to lower their monthly payment.

The Department of Education offers numerous plans to borrowers with federal student loans that help make payments more affordable. These include options that let borrowers set their monthly payment based on their income.

Repayment plan options for federal loans have expanded in recent years, but record numbers of student borrowers continue to struggle with debt, and a quarter of borrowers are in default or scrambling to stay current on their loans, despite the availability of income-driven repayment options for the vast majority of borrowers.

The Payback Playbook prototype disclosures are available online and the public can provide feedback through June 12, 2016, though it is unclear when they will be available to borrowers.

If you’re struggling with student loan debt, you can review these little-known ways to get your student loan debt forgiven to see if any are right for you, or you can try to defer or forbear your loans while you shore up your finances. Remember, missing payments will impact your credit. If you’ve already done so, you can see how bad the damage is by checking your free credit report summary on Credit.com.

Want more government freebies? Check out our full list of things you can get for free from the government.

Image: iStock

August 26, 2020

Student Loans

August 4, 2020

Student Loans

July 31, 2020

Student Loans

{kind=link}