The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Information on this website may not be current. This website may contain links to other third-party websites. Such links are only for the convenience of the reader, user or browser; we do not recommend or endorse the contents of any third-party sites. Readers of this website should contact their attorney, accountant or credit counselor to obtain advice with respect to their particular situation. No reader, user, or browser of this site should act or not act on the basis of information on this site. Always seek personal legal, financial or credit advice for your relevant jurisdiction. Only your individual attorney or advisor can provide assurances that the information contained herein – and your interpretation of it – is applicable or appropriate to your particular situation. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, contributors, contributing firms, or their respective employers.

Credit.com receives compensation for the financial products and services advertised on this site if our users apply for and sign up for any of them. Compensation is not a factor in the substantive evaluation of any product.

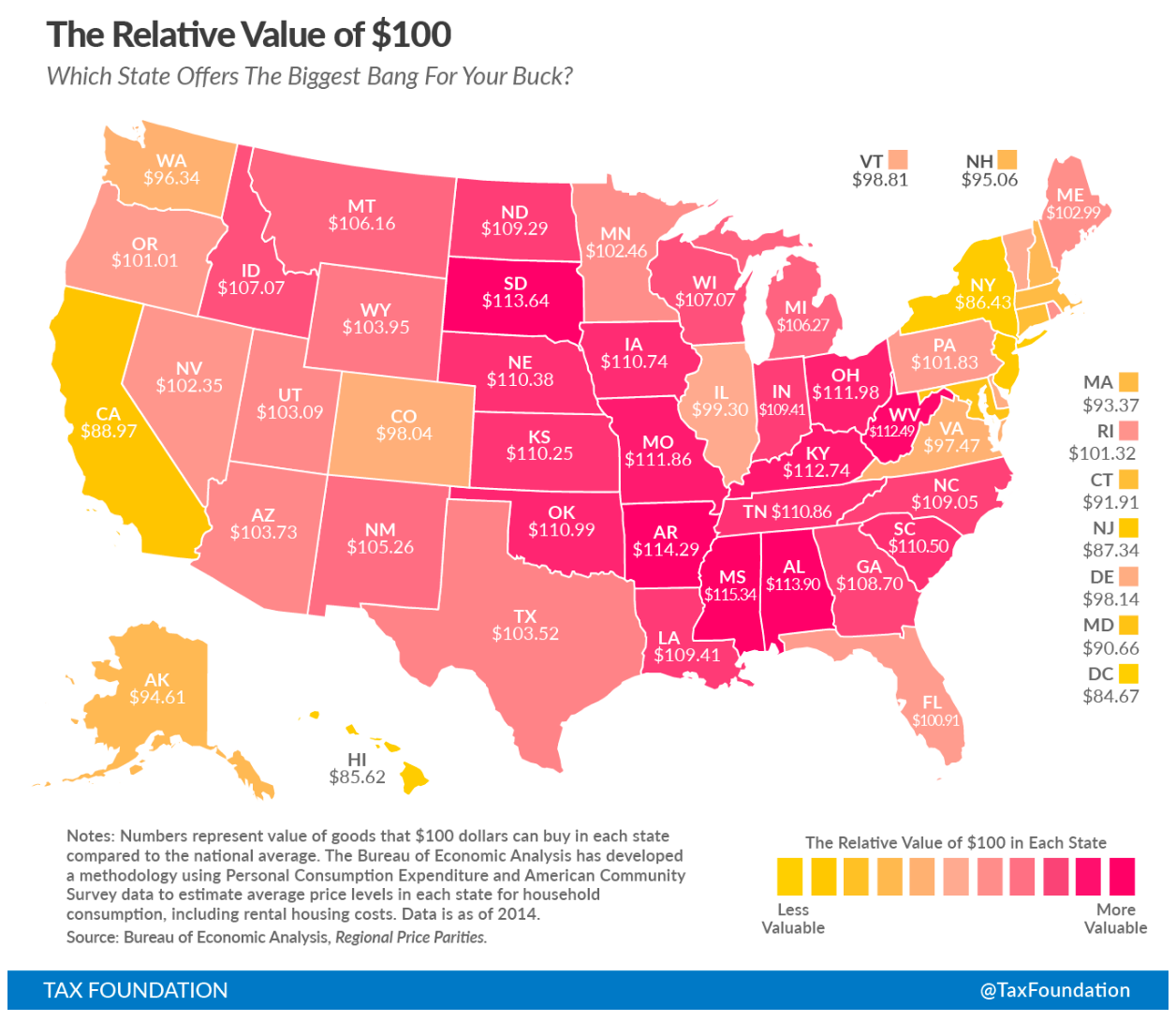

A dollar isn’t always a dollar, as a recent report makes clear. Sometimes it’s $1.15. Other times it’s less than 85 cents, and it all boils down to where you live.

That’s the finding of the Bureau of Economic Analysis, which published in July its report for 2014 prices for household consumption across the country. Your dollar will go a lot farther — 30% farther, in fact — in states like Mississippi and Arkansas than it will in places like Washington, D.C., and Hawaii.

The states where your dollar (rounded to the nearest cent) is worth the most are:

1. Mississippi ($1.15)

2. Arkansas ($1.14)

3. Alabama ($1.14)

4. South Dakota ($1.14)

5. Kentucky ($1.13)

6. West Virginia ($1.12)

7. Ohio ($1.12)

8. Missouri ($1.12)

9. Oklahoma ($1.11)

10. Tennessee ($1.11)

11. Iowa ($1.11)

In all, the cost of living in 35 states was below the national average, the report showed. The Tax Foundation used the numbers to create a map showing a comparison of the value of $100 in each state across the country:

The areas where your dollar is worth the least are the District of Columbia (85 cents), Hawaii (86 cents), New York (86 cents), New Jersey (87 cents), and California (89 cents).

The BEA used regional price parities (RPPs) calculated by using price quotes for a wide variety of items related to food, transportation and education, and compared that to the national average. So, if the RPP for area A is found to be 120 and for area B it is 90, then on average, prices are 20% higher and 10% lower than the U.S. average for A and B, respectively.

If the personal income for area A is $12,000 and for area B is $9,000, then RPP-adjusted incomes are $10,000 ($12,000/1.20) and $10,000 ($9,000/0.90), respectively. In other words, the purchasing power of the two incomes is equivalent when adjusted by their respective RPPs.

Regardless of where you live, credit card debt can be one of the most difficult things to overcome in trying to get ahead financially. Having a high balance on your cards will hurt your credit score, and it can be extremely challenging to break the spending habits that got you into debt in the first place.

Having a poor credit score won’t make you a credit exile — for instance, there are some credit cards for people with bad credit — but it can make your finances more challenging. One of the best ways to improve your credit while tackling debt is to prioritize making payments on time and reducing spending, so you can chip away at your credit card debt rather than add to it.

Paying off your credit card debt may also help you save money. The sooner you pay it off, the less you’re going to pay in interest and can save over time. (You can read this guide for tips on getting out of debt.)

Paying down debt will also improve your credit score. You run the risk of damaging your credit if you are in too much debt and can’t keep up with payments. To see how your debts and spending habits are affecting your finances, you can view your free credit report summary, updated every 14 days, on Credit.com.

Image: Cathy Yeulet

April 11, 2023

Uncategorized

September 13, 2021

Uncategorized

August 4, 2021

Uncategorized

{kind=link}