Is renting a picket fence the new American Dream?

You’ve probably seen the slew of reports recently confirming that homeownership is on the decline around the country — a trend begun during the Great Recession that has not changed during the recovery. The Census Bureau reported last month that the share of homeowners in America dropped to its lowest level since 1967 — since before humans walked on the moon!

This is not good news for renters. The more competition for rental units, the higher the prices. Zillow reported recently that rental prices were up 4.3% in June year over year, leading to this dismal proclamation by Zillow’s chief economist Stan Humphries: “Rents are insanely unaffordable on a historical basis in the United States right now.” Rent increases are far outpacing wage increases.

When rents rise like this, renters normally turn to purchasing homes. Mortgages offer one clear advantage over renting: fixed monthly payments. But housing prices are rising in many markets too, and the for-sale inventory is shrinking, Zillow says, meaning there aren’t many home bargains out there either.

The compromise between renting an apartment and buying a home is renting a single-family home. That’s traditionally a choice made by only a small number of Americans, but one of the trends-within-a-trend in the housing market is a tremendous surge in families doing just that. Here are some startling numbers from a recent report published by the Joint Center for Housing Studies at Harvard University.

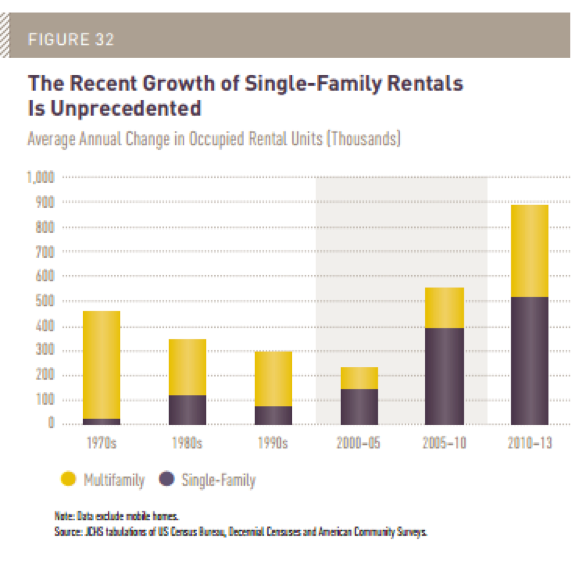

‘Unprecedented’ Change

During the 1990s, single-family homes for rent grew at an average of 73,000 units annually. Pre-recession, growth jumped to 138,000. When the recession hit, that number soared to 513,000 annually. Add it all up, and one hidden consequence of the housing bubble burst is 3.2 million more American households rent their single-family home, rather than owning — a figure that accounts for nearly half the jump in all rentals post-recession.

“The recent growth of single-family rentals is unprecedented,” the Harvard report says.

Some of the reasons for this are obvious, some less so. Many Americans hit by the recession could no longer afford their house payments, or were no longer able to obtain mortgages because of bad credit scores or limited income. (You can check your credit scores for free on Credit.com to see how you compare to the average American.) Renting single-family, detached homes became an attractive option for this group. Also, single-family housing construction projects begun during the housing bubble became difficult to sell when the bubble burst. Builders rushed to convert them to rental stock.

“When rental demand began to climb after the housing bust, conversions of owner-occupied single-family homes to rentals accommodated much of this growth. These shifts also helped to stabilize for-sale markets, especially in the Sunbelt metros with the largest inventories of distressed and vacant single-family homes,” the Harvard report said.

So conversion to rentals helped restore order to neighborhoods plagued by foreclosures; but some now fear that as the trend continues, it’s another factor squeezing out young adults trying to start families. Investors noticing the solid returns on rental homes are gobbling up that excess single-family housing stock, and have begun renting out homes en masse.

Data from RealtyTrac demonstrates the trend. Owner-occupant buyers accounted for 63.2% of all residential single family home and condo sales in the first quarter of 2015, down from 68.6% a year ago, to the lowest quarterly level going back to the first quarter of 2011, the earliest quarter with data available. Meanwhile non-owner-occupant buyers — any buyer who purchased a property but has their property tax bill mailed somewhere else — reached a new high of 36.8% in the first quarter of 2015.

Bad News for Would-Be Buyers

This trend is having unfortunate consequences for would-be first-time homebuyers. First, those who might rent a single-family home as a transition stage are facing the same competitive atmosphere that all renters are — rental fees are rising. More important, investors who have no plans to occupy the homes they buy are pushing up prices on what would otherwise be low-priced starter homes for families.

RealtyTrac data hints that, in some markets, larger investors have pulled back slightly from single-family home purchases … but smaller “mom-and-pop” investors have taken their place.

“Investor activity continues to represent a disproportionately high share of all home sales activity in this housing recovery,” said Daren Blomquist, vice president at RealtyTrac.

And hot housing markets are a big target for investors — contributing to rising prices and rents.

“Among metropolitan statistical areas with a population of at least 500,000, Memphis, Tennessee, posted the highest share of institutional investor purchases of single family homes in the first quarter of 2015 — 14.1 percent — followed by Charlotte, North Carolina (12.1 percent), Atlanta, Georgia (9.6 percent), Jacksonville, Florida (8.5 percent), and Oklahoma City, Oklahoma (7.6 percent),” RealtyTrac says.

It all adds up to higher prices for families trying to move out of apartments and trying to find a home to live in, buying or renting. But the shift to a renter-heavy mix in neighborhoods might have longer-term social consequences, warns housing expert Logan Mohtashami, a loan officer in California.

“Are we at the beginning of a sociological movement away from middle-class home ownership and towards a cultural split between the investment property landlords and their renters both of whom may have less personal investment in neighborhood security, local schools and shared public facilities compared to primary homeowners,” he said. “The longer-term consequences of an unstable residential real estate market may be more serious than just the destruction of individual wealth. The ideal of middle-class homeownership may be at stake.”

More Money-Saving Reads:

Image: iStock

You Might Also Like

Find out if your rent and utility payments are reported on your c... Read More

April 11, 2023

Uncategorized

Becoming an authorized user is a common tip for individuals tryin... Read More

September 13, 2021

Uncategorized

Long-term unemployment can really hurt—and not just financially... Read More

August 4, 2021

Uncategorized