Have you ever been to a financial seminar or workshop? The presenter no doubt tried to project an aura of financial savvy and confidence, likely dressing the part in a suit or similar business attire.

But if you were to attend one of Michael Finley’s seminars, you would see him wearing something a little different: a bright pink wig. He wears it to make a point he thinks is crucial to his message about financial literacy. If you want to be financially successful, you need to be a little crazy.

Not crazy as in “here’s a little-known technique to beat the market and get rich” crazy, but crazy as in “I don’t care what people think.” It’s become his trademark and he wears it proudly.

“The pink wig is a metaphor I use to help people see if they are going to live a financially successful life it is going to be tough,” he says. “It is going to take someone who is OK being different from the crowd. To be different you are going to be identified as strange, unique or quite possibly crazy. That’s OK, because walking the path of a financially literate and low-debt life can lead to something greater.”

Making Mistakes … and Learning

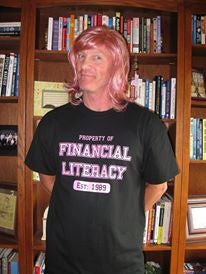

Michael Finley in his trademark pink wig

Finley’s journey to financial success started when in his 20s when, with no job and no prospect of one, he enrolled in the U.S. Army. In 1985, he was introduced to a stockbroker with whom he invested $300 a month in stocks and mutual funds. An insurance salesman sold him a whole life insurance policy. He financed a new vehicle.

He thought he was on his way.

It was only until 1989 when he was stationed in Germany and looking for ways to spend his free time that he started to learn about personal finance, reading every book on the subject he could find. He discovered he had already made some big mistakes. He calculated his net worth and had a rude awakening: he was in the red. He was paying far too much in commissions on the stock and mutual funds he owned. He didn’t need an overpriced whole life insurance policy. And he was paying a high interest rate on his vehicle loan. “Dumb, dumb and dumb,” he says.

But he was determined to turn things around, and he did. “I took full responsibility,” he says. “I had a real commitment to pay (my debt) off. I lived in a very frugal way spending very little extra money and paying off those debts as fast as I could.”

This was before he found the pink wig, but even then he could sense that he was viewed as a little different. “There were more than a few people who asked me if I was having financial problems,” he recounts. “I was being a little crazy at that time. I stuck to that path even though the people around me weren’t so supportive.”

His commitment to his education and financial success paid off. By the age of 45, he had a net worth of $1 million. As his investments grew, his passive income from his investments gradually surpassed his earned income, which never hit the six-figure mark.

Words to Budget By

His new book, Financial Happine$$, is an easy-to-read manual in which he explains to his readers how he created financial success and how they can, too. Each chapter is short: no more than two or three pages, and succinctly describes a clear concept on budgeting, saving, investing, or changing one’s attitude toward money.

Here is some of his advice he shares in his book about why you need to be willing to challenge conventional wisdom in order to build wealth.

Don’t Follow the Crowd. The crowd lives paycheck to paycheck because that is just the way you do it. The crowd accepts their fate because they see no way to escape it. The crowd accepts the belief that they are victims. None of these thoughts or actions will serve a person well, that I can promise you.

Stop Trying to Be Cool. If you insist on being cool in everything you do and everything you own, you may very well fall down the same deep well of debt into which many people have ended up over the years. Do not allow advertising campaigns to manipulate you on the cool factor. Instead of working so hard on being cool on the outside, I encourage you to be cool on the inside.

Live in the Gap. The way to get ahead financially is to widen the gap between your income and your spending as much as you can for as long as you can. Far too many people have no gap at all.

What will happen if you apply the gap over a matter of months and years? Some will resent you. You will make them feel uncomfortable because of your self-discipline and courage. Some will criticize you. Your level of sacrifice will distinguish you from the crowd of stressed out debtors, and that makes you crazy in their minds. Go figure.

Today, Finley is retired but working as hard as ever to share his message. In addition to writing the book, he started the UNI Financial Literacy Club at the University of Northern Iowa, where he teaches students, faculty members, professors and members of the local community about the world of money and how to become efficient investors. He also volunteers with programs like Junior Achievement, and he works with the State of Iowa and the Iowa National Guard to help educate veterans and as well as those who are currently serving. He is helping to train young officers so they can, in turn, train young soldiers.

“We are trying to develop a culture of financial literacy,” he says.

And as further proof of his unconventional approach, he is planning to give away $100,000 next year in a financial literacy contest. Some may think he’s a little nuts, but in this case he really is laughing all the way to the bank.

More on Managing Debt:

- The Credit.com Debt Management Learning Center

- How to Pay Off Credit Card Debt

- 5 Tips for Consolidating Credit Card Debt

- Understanding Your Debt Collection Rights

- The Best Way to Loan Money to Friends & Family

- Top 10 Debt Collection Rights

Main image: NinaMalyna; second image courtesy Michael Finley

You Might Also Like

Learn more about what a judgment is, how it works, and what the d... Read More

May 30, 2023

Managing Debt

Medical bills can be daunting. Around 67% of bankruptcies in the ... Read More

September 7, 2021

Managing Debt

Debt can feel like a terrible thing, but paying off your debts is... Read More

December 23, 2020

Managing Debt