The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Information on this website may not be current. This website may contain links to other third-party websites. Such links are only for the convenience of the reader, user or browser; we do not recommend or endorse the contents of any third-party sites. Readers of this website should contact their attorney, accountant or credit counselor to obtain advice with respect to their particular situation. No reader, user, or browser of this site should act or not act on the basis of information on this site. Always seek personal legal, financial or credit advice for your relevant jurisdiction. Only your individual attorney or advisor can provide assurances that the information contained herein – and your interpretation of it – is applicable or appropriate to your particular situation. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, contributors, contributing firms, or their respective employers.

Credit.com receives compensation for the financial products and services advertised on this site if our users apply for and sign up for any of them. Compensation is not a factor in the substantive evaluation of any product.

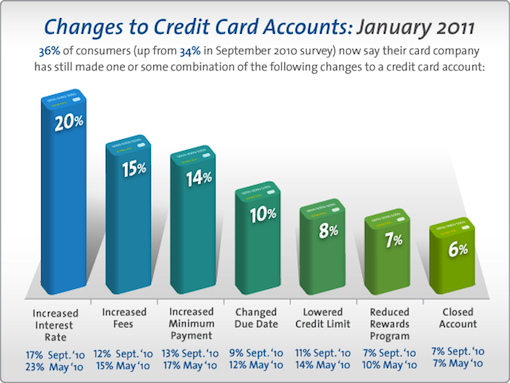

The Credit CARD Act of 2009 brought some much-needed protection to consumers. But along with all the good stuff, we also got a few not-so-good things. These things, also known as the dreaded “unintended consequences,” ranged from APR increases to credit card account closures.

In February 2010, Credit.com did a survey to find out what changes, if any, consumers had experienced. This survey showed that 43 percent of consumers had experienced changes—and not the good kind—to their credit card accounts. In Credit.com’s most recent survey, the number of consumers who had experienced negative changes to their accounts fell to 36.5 percent. This still seems a little high, but at least the percent who experienced a bit of unpleasantness is down from a year ago.

[Consumer Guide: How the Credit CARD Act of 2009 Affects You]

Here’s a list of the changes we asked consumers about. The responses from our current survey are listed as well as responses from a year ago. You can see the differences—or, in a few cases, lack thereof—between the most recent results to those from a year ago.

Compared to a year ago, consumers appear to be experiencing fewer negative changes to their accounts, with the exception of minimum payment increases and changes in due dates. Still, the best thing for you to do is to keep an eye on your accounts. Be on the alert for increases in your minimum payment or increases in your APR. And remember if you see changes to your accounts, you can call the issuer and negotiate, whether it’s a changed due date or a crazy new fee that shows up.

What about you? Have you experienced any of these changes to your credit card accounts recently?

[Featured products: Shop for a credit card]

This national RDD Probability Sample telephone poll was conducted for Credit.com by GfK Custom Research North America from January 14-16, 2011. A total of 1,004 interviews were completed, with roughly 531 female adults and 473 male adults. The margin of error is +/- 3 percentage points for the full sample.

April 9, 2024

Credit Cards

October 21, 2020

Credit Cards

August 3, 2020

Credit Cards

{kind=link}