The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Information on this website may not be current. This website may contain links to other third-party websites. Such links are only for the convenience of the reader, user or browser; we do not recommend or endorse the contents of any third-party sites. Readers of this website should contact their attorney, accountant or credit counselor to obtain advice with respect to their particular situation. No reader, user, or browser of this site should act or not act on the basis of information on this site. Always seek personal legal, financial or credit advice for your relevant jurisdiction. Only your individual attorney or advisor can provide assurances that the information contained herein – and your interpretation of it – is applicable or appropriate to your particular situation. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, contributors, contributing firms, or their respective employers.

Credit.com receives compensation for the financial products and services advertised on this site if our users apply for and sign up for any of them. Compensation is not a factor in the substantive evaluation of any product.

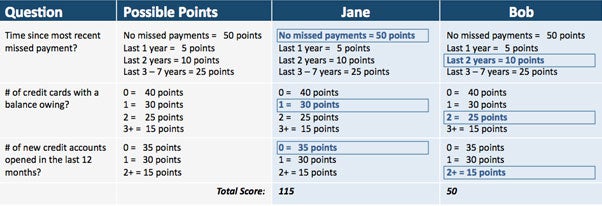

When a credit score is generated, there are a series of credit related questions being asked by the scoring model, and the answers for each question will depend on the information (or data) being reported in your credit report. Points for each answer to each question are assigned and the sum of these points is generated to create your credit score.

Let’s take a look at the made up example scorecard below and the associated scores for Jane and Bob. The information highlighted in blue represents the points assigned for each credit question based on information reported in their credit reports:

After the score is calculated, score reason codes are generated along with the score – both of which are provided to the lender who requested the credit report. If the lender denies the request for credit, they will often incorporate these reason codes into the adverse action letter they are obligated to provide to you in order to help explain why the credit request was denied. These reason codes are also frequently included within the score explanation section when you purchase access to your personal credit report and score.

[Featured Tool: Get your free Credit Report Card from Credit.com]

These reason codes indicate the main reasons why your credit score was not higher and are returned with the score in order of importance–with the first code indicating where the consumer lost the most points, or the primary reason why the score wasn’t higher, the second being the secondary reason, and so on.

Now, let’s calculate the top reasons why Bob’s score wasn’t higher. We do this by simply subtracting the total number of points Bob received from the maximum number of points available for each “question” in the scorecard:

These are then sorted in order of impact of where the greatest number of points were lost. For Bob, the following credit score and score reason codes would be returned as:

Bob’s Credit Score = 50

Top reasons why Bob’s score was not higher:

With this information, Bob is able to understand what credit behaviors had the most substantial impact on his score and where he needs to currently focus his efforts in order to improve his score.

[Related Article: The Politics of the Credit Score]

Up to four reason codes are returned with each score generated by the credit reporting agency. In some cases, a fifth reason code is provided, but only if the # of credit inquiries is a factor that affected your score—but was not already in the top four reasons. Even people with really high scores—say a 790 or higher—may return reason codes with their score. This simply represents areas where the high scoring person just missed earning the maximum number of points available for that particular data element.

Now that we’ve determined Bob’s reason codes, how many reason codes would Jane’s score produce? Know the answer? Share them in the comments section below.

Image by Stewf, via Flickr

March 7, 2023

Credit Score

January 4, 2021

Credit Score

September 29, 2020

Credit Score

{kind=link}

{kind=link}

{kind=link}