The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Information on this website may not be current. This website may contain links to other third-party websites. Such links are only for the convenience of the reader, user or browser; we do not recommend or endorse the contents of any third-party sites. Readers of this website should contact their attorney, accountant or credit counselor to obtain advice with respect to their particular situation. No reader, user, or browser of this site should act or not act on the basis of information on this site. Always seek personal legal, financial or credit advice for your relevant jurisdiction. Only your individual attorney or advisor can provide assurances that the information contained herein – and your interpretation of it – is applicable or appropriate to your particular situation. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, contributors, contributing firms, or their respective employers.

Credit.com receives compensation for the financial products and services advertised on this site if our users apply for and sign up for any of them. Compensation is not a factor in the substantive evaluation of any product.

You take your money and your credit rating seriously. You probably know a thing or two about credit and how it works too. You may think that the savings of your finances—like your savings account, your certificate of deposit (CD) and your other assets—doesn’t affect your credit. For the most part, you’re right. But, does opening a CD affect your credit? The answer is that it actually might.

Your credit score and your credit file are based on how you handle debt. Credit bureaus, such as Experian, TransUnion and Equifax, keep a file on your debt activities. The information on that file is used to calculate your credit score by analyzing how you repay money you borrow, including installment loans and revolving lines of credits, AKA credit cards.

The credit reporting agencies to give you a score by using credit scoring models that look at your payment history, credit utilization ratio (how much of your available credit limit you’ve used), your credit age or credit history, your mix of accounts and how many credit inquiries you have on your file. Lenders and credit card issuers look at that score and sometimes your entire file to determine whether to give you a loan or credit card.

If you miss multiple credit card payments, your credit rating goes down. On the other hand, when you diligently pay bills on time, your credit rating goes up or at least stays the same.

Assets, such as real estate, CDs and savings accounts, don’t affect your credit score. You could regularly put money in savings, and it won’t affect your credit rating. And you can have a million dollars in savings and still have a bad credit score if you regularly make late payments on your credit card, have maxed out your credit cards or have too many hard inquiries on your file.

Granted, a mortgage lender might give borrower A, who has a million in savings and a 600 credit score, a home loan and not borrower B, who has $100 in savings and a score of 600. But, borrower A and B still have the same credit rating of 600.

There’s one time when assets can creep in and affect your credit score—when you open a new CD or another deposit account. For some reason, some banks and credit unions—not all—do a hard inquiry on your credit when you open a new account.

To put that into perspective, a hard inquiry really isn’t a big deal. Hard credit inquiries only account for about 10% of your credit score. Their cousins—soft inquiries—don’t affect your score at all. A single hard inquiry—also called a hard pull—can stay on your credit file for up to 2 years. It will drop your score by less than five points.

You have the right to ask if the bank, credit union or other financial institution does a hard pull on your credit when you open a CD. So, before opening the CD:

If you’re in a situation with your credit rating where that hard pull will hurt, consider opening your CD elsewhere.

Depending on your current score, the few points that a hard inquiry put on your credit file is probably minimal. The few times the impact might matter include:

Opening a CD might affect your credit rating if:

But, that hard pull should only really hurt your credit if:

Now that you know that opening a new CD might affect your credit rating, you can find out if your chosen institution will do a hard pull if that will hurt your credit.

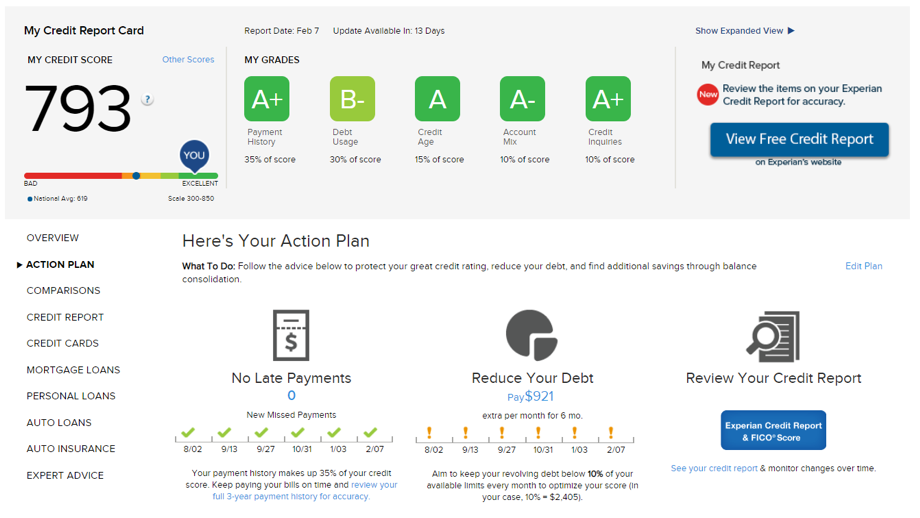

To keep a regular pulse on your credit rating you can also get your free Experian credit score and free credit report card here on Credit.com. Your score and your report card—sample shown below—let you keep an eye on your credit regularly. Along with how you are doing with payment history, debt usage, credit age and account mix, your report also shows how many credit inquiries you’ve had and how they’re affecting your score.

April 11, 2023

Uncategorized

September 13, 2021

Uncategorized

August 4, 2021

Uncategorized

{kind=link}