The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Information on this website may not be current. This website may contain links to other third-party websites. Such links are only for the convenience of the reader, user or browser; we do not recommend or endorse the contents of any third-party sites. Readers of this website should contact their attorney, accountant or credit counselor to obtain advice with respect to their particular situation. No reader, user, or browser of this site should act or not act on the basis of information on this site. Always seek personal legal, financial or credit advice for your relevant jurisdiction. Only your individual attorney or advisor can provide assurances that the information contained herein – and your interpretation of it – is applicable or appropriate to your particular situation. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, contributors, contributing firms, or their respective employers.

Credit.com receives compensation for the financial products and services advertised on this site if our users apply for and sign up for any of them. Compensation is not a factor in the substantive evaluation of any product.

If you’re saving for retirement, you’re probably already aware of the need to factor in inflation (and, if you aren’t already saving, here are some tips). While you’re on the right track by doing so, it’s also important to think about adjusting your annual budget for inflation.

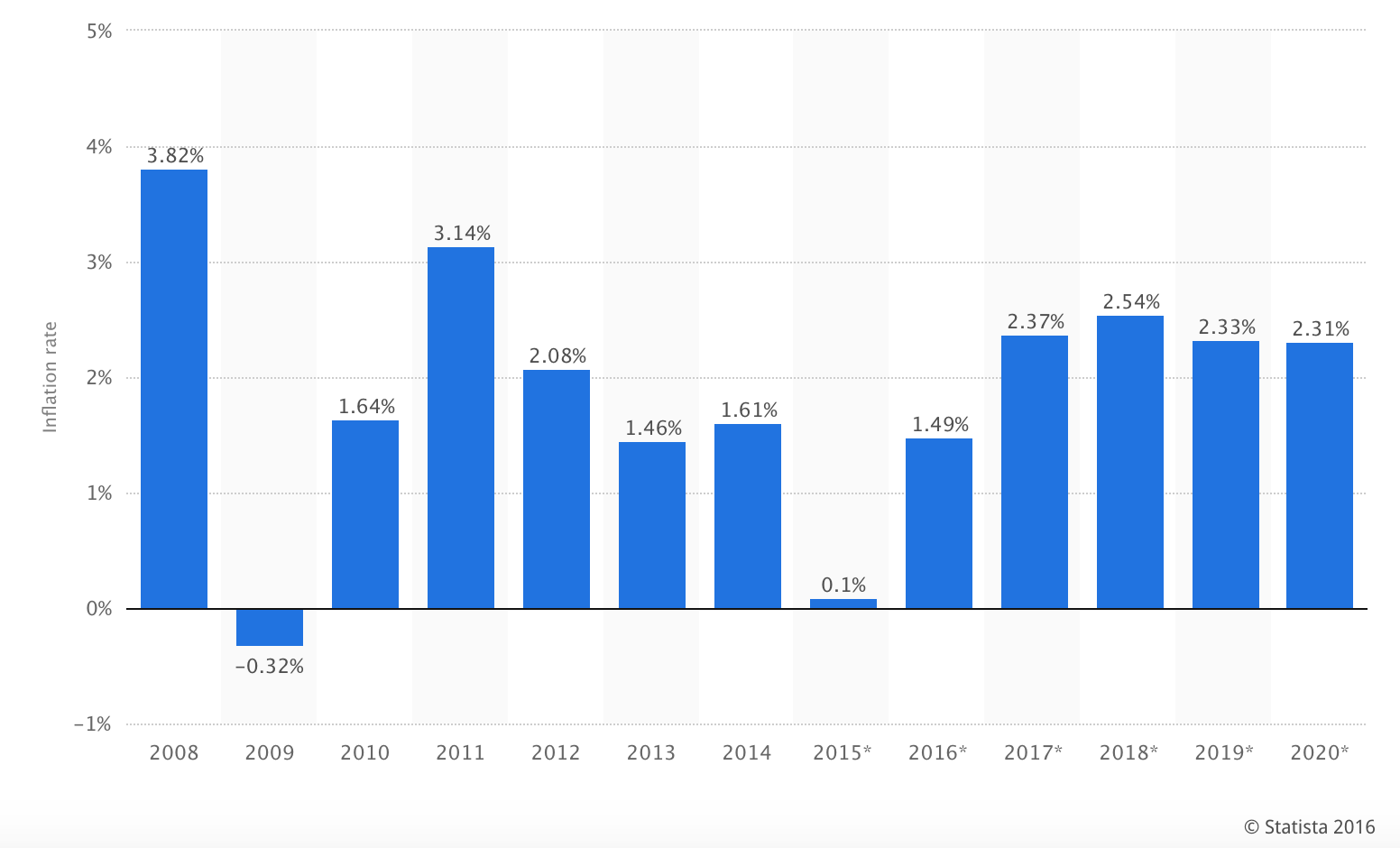

Even when inflation rates are low, like they have been the last several years (experts report 2015 will have just a 0.1% inflation rate), if your budget doesn’t account for cost increases, you’re more likely to miss your savings and spending goals.

How? Simply put, your money becomes less valuable when inflation rates increase. As this happens, you’ll pay higher prices for goods and services, even if you’re among those lucky enough to get salary increases every year. For example, let’s say you got a 2% raise in 2011. If you didn’t adjust your spending for the 3.1% inflation rate that year, you experienced an overall loss. With the rate of inflation expected to increase the next few years, now is a good time to start considering the impact inflation might have on your monthly spending.

How do you budget for inflation, particularly when you won’t know until well into the following year exactly what the true rate of inflation even was?

“Tracking your actual expenses will help you build a budget that reflects incremental changes in the cost of goods and services,” Toni Husbands, a financial coach and co-founder of Debt Free Divas, advised. “While you make a plan for spending ahead of time, reconciling actual expenses will allow you to adjust as needed. A rise in cost on essential items, like gas or insurance, must be offset by either additional sources of income or an adjustment in fun categories like entertainment or clothing.”

Another helpful way to avoid the fallbacks that can come with inflation is to pay off high-interest credit card debt as quickly as possible, Husbands said.

“Paying interest rates on balances carried month over month magnifies the impact of inflation as it rises,” she said. “In this case, compound interest is working harder against you. With the extra cash available after repaying all credit card debt, you can take advantage of more aggressive saving and investing strategies to build wealth at a rate that outpaces inflation.”

You can also minimize the effects of inflation by keeping your credit score in tip-top shape. This will allow you to take advantage of the lowest interest rates on everything from credit cards to auto loans and mortgages. You can see how your credit score is faring by getting your two free credit scores each month on Credit.com. And while you’re at it, you can also check for any errors on your credit report.

Image: iStock

April 17, 2023

Budgeting and Saving Money

April 3, 2023

Budgeting and Saving Money

March 8, 2023

Budgeting and Saving Money

{kind=link}