It's Financial Literacy Month: Here's What Your Credit Score Wants You to Know

Learn how to improve your credit score with essential tips on payment history, credit utilization, and more this Financial Literacy Month.

Published December 4, 2023

Many or all of the products featured here are from our partners who compensate us. This may influence which products we write about and where and how the product appears on a page. However, this does not influence our evaluations.

If you’re interested in investing in a new vehicle, it’s not always easy to know what’s in your price range. Understanding your options and learning how to calculate your budget can determine what you can afford.

Discover how auto loans can enhance your ability to afford a range of vehicles, from brand-new cars to those with some mileage.

Calculating how much you can afford for your new car is a helpful step in saving money when you’re ready to make the purchase. Follow the next steps to calculate your budget effectively.

There are two main expenses to consider when calculating your car payment budget: your down payment and your monthly payment.

Above is an example of how to calculate your monthly payment calculation. Let’s say you have a net monthly income of $4,500. Multiply your income by 0.10, or take 10% of your income. This number will be your estimated monthly payment. In this example, it would be $450.

You now have a better idea of how much you can potentially borrow based on your budget.

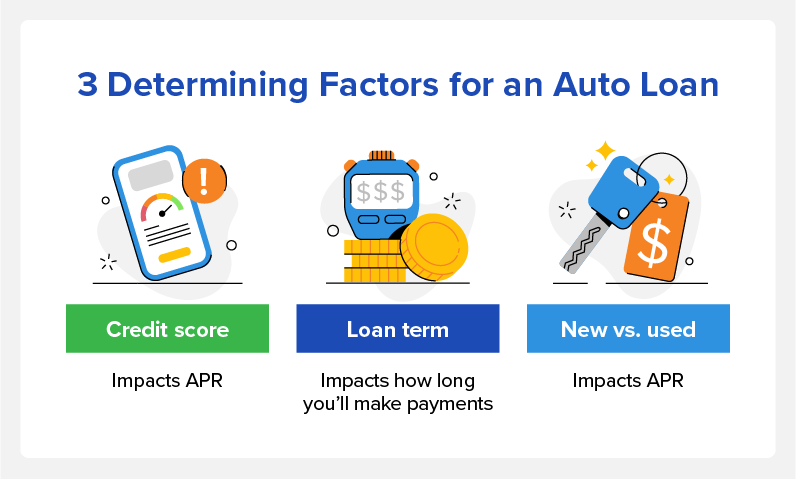

Several determining factors affect how much you can borrow, including:

If you already have an auto loan, you can refinance and customize your loan with Credit.com. Try out our Auto Loan Calculator to simulate your current payment and find out what savings you can earn today.

You should also factor in car insurance when considering purchasing a new vehicle. Factors like the make and model of the car, your driving history, and where you live can impact your insurance costs. Reach out to several insurance companies for quotes and get a clearer picture of what you’ll likely need to budget for insurance.

It’s important to note your auto loan isn’t the total price you’re going to pay for your vehicle. There are other hidden costs you should be aware of beyond the number on the price sticker. Take note of these common additional costs:

You never want to put yourself in a financially vulnerable position if you can avoid it. That’s why it’s important to consider all of your purchasing options. Keep reading to understand how buying versus leasing can help you afford a car.

Everyone wants a shiny new car, but it’s not always affordable. If there’s a particular type of vehicle you want, do some research to determine the vehicle’s current market value. That way, you’ll know exactly how much that car is worth and avoid purchasing a vehicle with an inflated price tag.

Purchasing a used vehicle can be the best route for those with a lower budget. Used vehicles tend to have considerably reduced prices compared to brand-new cars, leading to more affordable monthly payments. Additionally, used cars typically have lower car insurance costs.

Leasing a car can be a great option for those who want a brand-new car, but would prefer lower monthly payments. There are drawbacks to this option, however, as the payments that go toward the vehicle don’t provide value and there are mileage limits. But if you don’t mind those drawbacks and like to try out different cars every couple of years, leasing is worth considering.

Here are answers to some frequently asked questions about car affordability and monthly payments.

Determining your car affordability based on your net income is one way of estimating how much car you can afford. You should put 10% or less of your monthly income toward your car payments.

| Annual Income |

Monthly Car Payment Maximum |

|

|---|---|---|

| $30,000 |

$250 |

|

| $40,000 |

$334 |

|

| $50,000 |

$416 |

|

| $60,000 |

$500 |

|

| $70,000 |

$584 |

|

| $80,000 |

$667 |

|

| $90,000 |

$750 |

|

| $100,000 |

$833 |

However, this doesn’t include costs such as fuel, parking, and maintenance. You can plan on dedicating about 15% of your monthly income to total vehicle expenses.

Your monthly car payment will depend on a few factors, such as your auto loan interest rate, loan term, and how much you put toward your down payment. Your choice of vehicle and where you purchase it can also affect interest rates.

However, your monthly car payment should be around 10% or less of your monthly take-home pay. You can always choose to pay more every month to pay your auto loan quicker and save money on interest.

Take your first step toward vehicle ownership by learning more about credit scores with Credit.com. Get your free credit report card today.

Learn how to improve your credit score with essential tips on payment history, credit utilization, and more this Financial Literacy Month.

Learn how to use your tax refund to improve your credit score with these strategic financial tips. Boost your financial health and achieve your credit goals.

Take control of your financial health and strengthen your money relationship with practical tips to improve your credit score and set financial goals today.