It's Financial Literacy Month: Here's What Your Credit Score Wants You to Know

Learn how to improve your credit score with essential tips on payment history, credit utilization, and more this Financial Literacy Month.

Published March 25, 2024

Generally, it helps to save up to 20-25% of a house’s sales price. However, factors like geographical location, economic climate, real estate interest rates, and global events will influence how much money you’ll need to buy a house.

Key Takeaways:

How much money do you need to buy a house? That cost depends on numerous factors like inflation and real estate trends. According to the Census, homes sold for a median price of $420,700 in January 2024.

Thankfully, you don’t need to pay off that amount all at once. A down payment that’s 20% to 25% of a home’s value can help you secure a property. Even if you don’t have the funds to make a sizeable down payment, low and no-down-payment mortgage options are available.

Below, we’ll share our expertise to help you learn all about loans and mortgage options. We’ll also answer several common questions and share helpful tools, like Credit.com’s mortgage calculator.

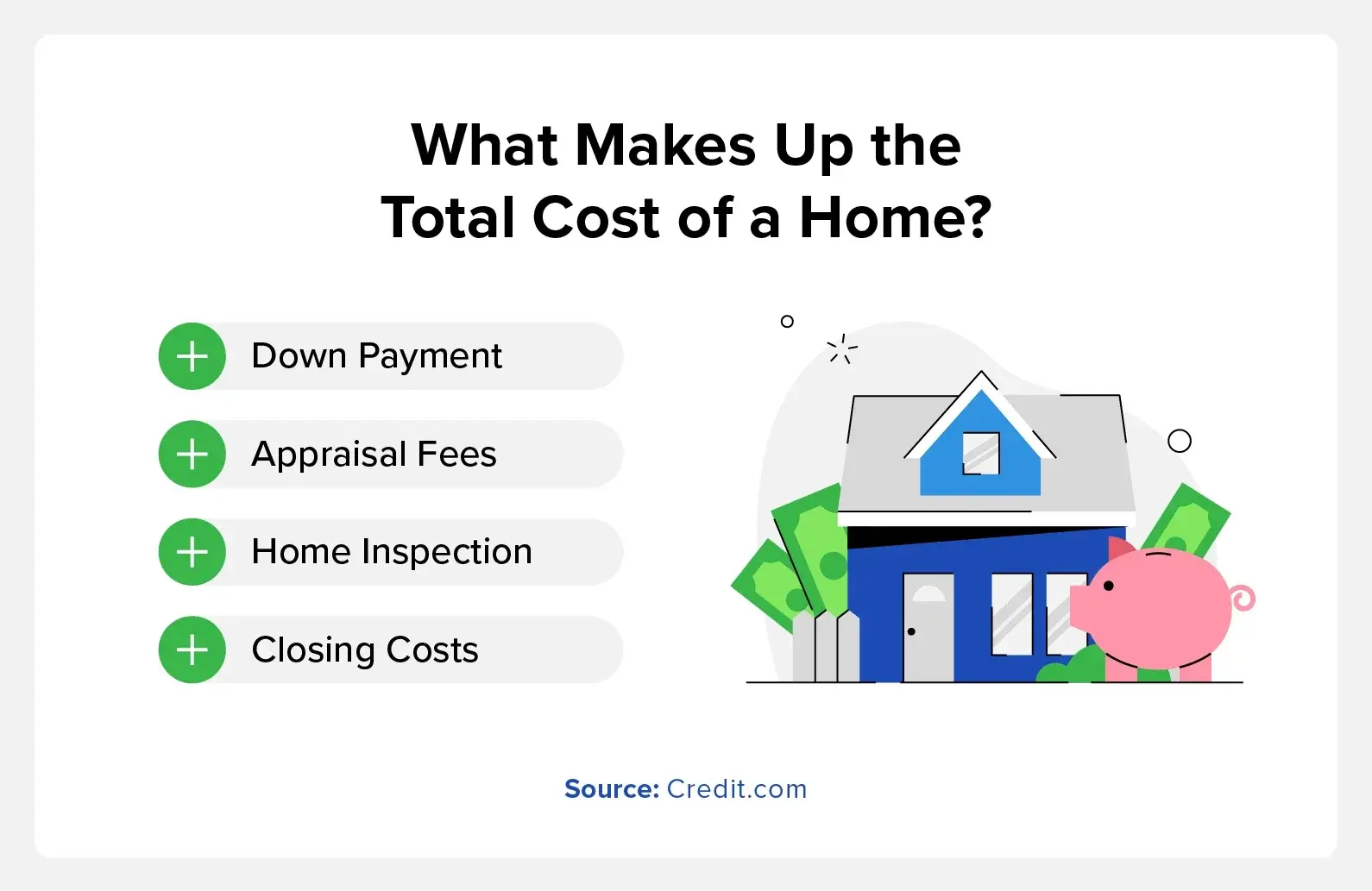

Spend enough time shopping around for houses, and you’ll learn very quickly that a property’s sales price isn’t the only expense you’ll have to pay. Below, we’ll cover down payments, earnest money deposits, and other factors that determine the real cost of a home.

According to the United States Census Bureau, 661,000 new homes were sold in January 2023. Most homebuyers don’t pay off their properties in full from the get-go. Instead, they cover a portion of the home’s cost with a down payment, then gradually pay off the remaining value via monthly mortgage payments.

“How do home mortgage rates work?” and “What types of mortgages am I eligible for?” are common questions for first-time homebuyers.

Below, we’ll discuss four mortgage options and break down how each of them works.

1. Conventional Mortgage

A conventional loan is a mortgage option that’s offered by a private lender instead of the government. Mortgage companies, credit unions, and banks offer conventional loans, though they might require a down payment between 20% and 25% of a property’s sales price.

Lenders might request that you purchase private mortgage insurance (PMI) if your down payment is less than 20%. PMI reimburses lenders if you don’t make your mortgage payments, and borrowers will have to pay for coverage annually.

2. USDA Mortgage

The United States Department of Agriculture (USDA) offers this unique mortgage to borrowers who live in rural areas. A USDA mortgage has no down payment requirement, and its interest rate is very competitive.

To qualify for a USDA loan, you need to:

You’ll also need to meet the lender’s credit requirements. On average, a credit score of 620 or more will qualify you for a government-backed USDA loan.

3. FHA Mortgage

The Federal Housing Administration (FHA) offers this distinct government-backed mortgage. Borrowers can secure an FHA mortgage with a down payment as low as 3.5%.

Borrowers with very low credit scores might be eligible for an FHA loan, at the expense of having more strict loan limits and higher up-front costs.

To get an FHA loan, you need to meet the following requirements:

4. VA Home Loans

Veterans Affairs (VA) loans offer low credit requirements and come with no down payment restrictions.

Certain people qualify for VA loans, including:

An earnest money deposit is a payment that buyers can place to demonstrate how serious they are about obtaining a property. Earnest money deposits are normally between 1% and 3% of a property’s sales price. This deposit is not the same as a down payment.

When you make an earnest money deposit, those funds are put into an escrow account. If the seller of a property closes on a deal with you, your earnest money deposit is then added to your down payment. If the seller doesn’t close on the deal with you, it’s possible to regain your earnest money deposit if contingencies are set in place.

Several common contingencies include:

Closing costs include taxes, appraisals, home inspection costs, title costs, and attorney fees. They’re generally between 3% and 6% of your mortgage principal. Your mortgage principal is the amount you borrow—so the bigger your down payment, the less you’ll pay in closing costs.

Let’s use the $200,000 home above as an example. Consider these three 4% closing cost scenarios:

Next, we’ll show you how to determine your down payment on a home with the previous loans as examples. Let’s imagine your dream home is on the market for $200,000.

USDA and VA home loan mortgage options have the lowest up-front costs for eligible borrowers. An FHA mortgage is less costly than a conventional loan, but interest rates will affect your total payments in the long term.

Making a down payment can be challenging because you need a paper trail of your purchases. In most cases, you can’t use borrowed money for a down payment.

Conversely, we know several creative ways to come up with a down payment:

You can roll other funds, like your tax return or a security deposit refund, into your down payment, too.

It’s important to look at the big picture when buying a house. You’ll need to pull together a down payment and closing costs, but you’ll also need to budget for removal costs, inspections, and repair fees.

A tool like a monthly budget template can put your common expenses into perspective and help you better understand how much house you can afford with your current income.

“What happens if I miss a mortgage payment?” is another concern for new and long-time homeowners. First, know that your home won’t immediately be foreclosed on if you miss a payment. Foreclosure usually isn’t imminent unless you’ve missed two or three payments.

If your mortgage payments aren’t within reach, you can contact your lender and explain your specific situation. Seeking forbearance, which is a temporary pause on your payments, can also help you regain your bearings.

Knowing your credit score and understanding the elements that affect it can help you know what you need to do to prepare for loan opportunities.

Sign up for Credit.com’s ExtraCredit® subscription to check out 28 of your FICO® scores. Afterward, visit our mortgage rates page to get additional information.

Learn how to improve your credit score with essential tips on payment history, credit utilization, and more this Financial Literacy Month.

Learn how to use your tax refund to improve your credit score with these strategic financial tips. Boost your financial health and achieve your credit goals.

Take control of your financial health and strengthen your money relationship with practical tips to improve your credit score and set financial goals today.