Setting aside savings can be difficult, particularly if you’re trying to raise a family — and that includes saving for your kids’ college educations. Only two out of five families have a savings plan for higher education prior to their student’s enrollment, and just 16% of families are using 529 college savings vehicles to pay for college expenses.

That’s according to the annual survey report “How America Pays For College” from Sallie Mae and market research firm Ipsos. The report reflects the results of telephone interviews conducted between March 16 and April 18, 2016, with 799 parents with children ages 18 to 24 who are enrolled as undergraduate students and 799 undergraduate students, ages 18 to 24.

The number of families using savings from 529 college savings plans or other college savings vehicles fell slightly from 17% in 2015 to 16% in 2016, the survey found. The average amount used from these accounts also dropped slightly, from $9,129 in 2015 to $8,315 this year.

Much like a Roth IRA, 529 savings plans have several tax advantages that can make them useful when saving for college. Contributions to the account are taxed but any earnings made on interest accrue federal tax-free. And withdrawals from the account are also tax-free so long as they’re put towards college expenses.

Families With a Plan Spend Less

The survey also found that families who did not have a college savings plan in general prior to their student’s enrollment reported spending more than twice their savings and income on college expenses over those families who did. Also, those families who had a plan reported a full one-third less borrowing by the student than those from families without a plan.

“It’s clear that having a plan for college really does pay off,” Rick Castellano, a Sallie Mae spokesperson, said in an email. “Those families with a plan are, as you might expect, more informed, but they are also saving more for college and borrowing less.”

Chart courtesy of Sallie Mae

Families with a plan also reported greater peace of mind in regard to paying for college. The survey showed:

- 61% of families with a plan felt completely confident they had made the right financial decisions about paying for college, compared to 41% of families without a plan.

- 45% of planners reported never or rarely being stressed over education expenses, compared to 32% of non-planners.

- Parents who planned were less likely to be very worried than non-planners about the possibility of loan rates rising (12% vs 29%) or tuition increasing (17% vs. 28%).

Scholarships, Grants Still Largest Resource

Of the average amount families reported paying for college — $23,688 — scholarships and grants funded an average of $8,059, or 34%, the report said. That’s an increase of four percentage points over 2014-15 and represents the largest proportion of any resource used to pay for college in the past five years, according to Sallie Mae.

Parental income and savings averaging $6,867, or 29% of total spending on college, came in as the second largest funding resource. That’s slightly lower than last year’s high of 32%, the report said.

Chart courtesy of Sallie Mae

Student borrowing was the third most-used resource to pay for college, averaging $3,176, and money borrowed by students paid 13% of all college costs, the survey found — slightly less than the prior year’s 16%.

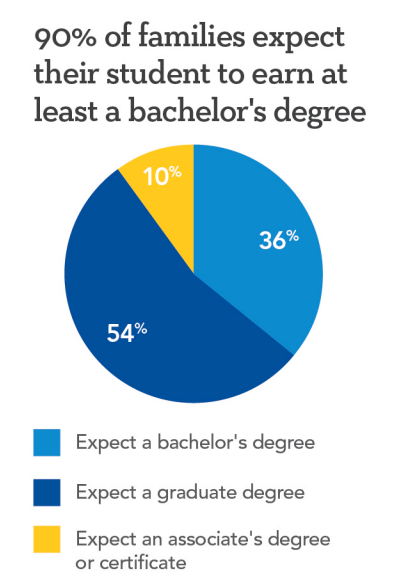

The survey also found that 90% of families expect their college student to earn at least a bachelor’s degree, including one-third of those students attending community college, and more than half (54%) expected their student to get a graduate degree.

If you’re ready to start saving for your child’s college education, it’s a good idea to educate yourself on the various forms of student loans and the federal aid options that might be available to you and your family — and how those options might impact your finances and your credit. (You can see a summary of your credit report for free on Credit.com to get an idea of where you stand.) The more informed you are, the less worried you may be about affording college expenses.

More on Student Loans:

- A Credit Guide for College Graduates

- How to Pay for College Without Building a Mountain of Debt

- Strategies for Paying Off Student Loan Debt

Image: Kali Nine LLC

You Might Also Like

Find out if your rent and utility payments are reported on your c... Read More

April 11, 2023

Uncategorized

Becoming an authorized user is a common tip for individuals tryin... Read More

September 13, 2021

Uncategorized

Long-term unemployment can really hurt—and not just financially... Read More

August 4, 2021

Uncategorized