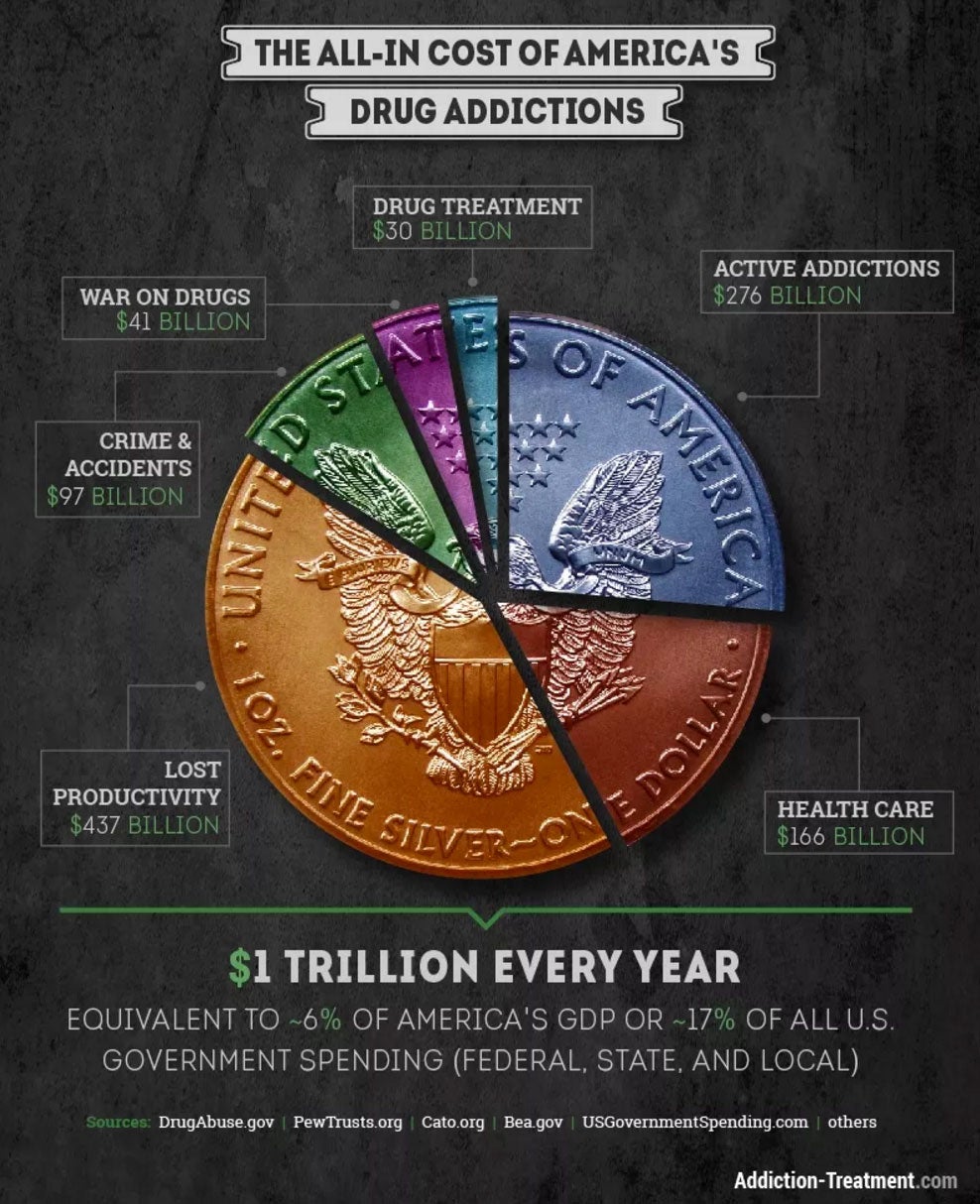

Americans spend an estimated $276 billion every year drinking, smoking and taking drugs, according to a recent analysis. To give that huge figure some perspective, that’s more than the federal government spent in 2015 on education and veterans’ benefits combined.

About half of the spending goes toward alcohol and nicotine, according to the analysis by Addiction-Treatment.com, a Santa Monica, California-based organization that helps connect people with substance abuse disorders with treatment providers. The organization looked at a wide range of sources to compile their estimates, including published government figures, data analysis and news reports.

Legal drugs nicotine and alcohol accounted for more than half of the total $276 billion spent, or roughly $140 billion. Broken down, nicotine made up around 52% of the money spent while alcohol made up 48%. The analysis broke the cost of alcohol abuse into two categories: binge drinkers (who consume six drinks over a short period, once or twice per week) comprising nearly 25% of money spent on abusing alcohol, and heavy drinkers (who consume about 21 drinks spread over a week) about 23%, the analysis showed.

Non-medical prescription drugs — including pain relievers, tranquilizers and stimulants — made up almost 22% of the total drug use cost; and marijuana, cocaine, heroin and meth accounted for nearly 28% of the total. (Though marijuana is legal in some form in 23 states and Washington, D.C., it was grouped under illegal drugs for the purpose of this study.)

Even more staggering than the estimated $276 billion spent, when the costs of active addictions are combined with the costs for treatment, enforcement actions against illegal sale and use, drug-related crime, accidents and lost productivity, addiction ends up costing Americans $1 trillion a year, the analysis found. That’s enough to, among other things, give every American over the age of 18 a check for $4,000 (see graphic below), the analysis concluded.

Protect Yourself Against the Costs of Addiction

If you or someone you know is struggling with addiction, you likely already realize the costs are more than just emotional and physical. Addiction can also push people into financial ruin. If you’re an addict, consider talking to someone you trust who can help you seek the resources you need to get sober.

If you aren’t an addict, but you share accounts with someone you suspect is an alcoholic or drug addict and is not interested in recovery, it could be wise for you to consider closing your joint accounts. It’s also crucial to monitor your credit, because an addict may not be in the right mindset to feel remorse about “borrowing” your information to open new accounts or even use your your health insurance or medical information to get prescription medications. (Medical identity theft is a huge and growing problem).

You can help protect yourself by getting your free credit reports from all three bureaus annually, and you can use a service such as Credit.com to get your two free credit scores, updated every 14 days. If it appears your information has been used fraudulently, consider placing a fraud alert or credit freeze on your reports.

Even if you or someone you love isn’t struggling with addiction but is just a casual drinker, smoker or drug user, it’s good to keep in mind that the money spent on these habits could potentially instead be used for paying off debt, saving for a mortgage or even for retirement.

That isn’t to say people without addictions should stop drinking (though there are health reasons to consider stopping smoking, and legal reasons to stop taking illegal drugs); it’s more of a reminder to track your spending. Blowing your budget on excessive social outings will push you into debt if you maintain the behavior long enough, and it doesn’t make sense to jeopardize your credit rating and financial future for a few extra pints of beer (or those extra packs of cigarettes or purchases of drugs). Enjoy what you enjoy, but do it responsibly, and keep track of how it fits into the big picture, both for your budget and your health.

Image: skynesher

You Might Also Like

Find out if your rent and utility payments are reported on your c... Read More

April 11, 2023

Uncategorized

Becoming an authorized user is a common tip for individuals tryin... Read More

September 13, 2021

Uncategorized

Long-term unemployment can really hurt—and not just financially... Read More

August 4, 2021

Uncategorized