The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Information on this website may not be current. This website may contain links to other third-party websites. Such links are only for the convenience of the reader, user or browser; we do not recommend or endorse the contents of any third-party sites. Readers of this website should contact their attorney, accountant or credit counselor to obtain advice with respect to their particular situation. No reader, user, or browser of this site should act or not act on the basis of information on this site. Always seek personal legal, financial or credit advice for your relevant jurisdiction. Only your individual attorney or advisor can provide assurances that the information contained herein – and your interpretation of it – is applicable or appropriate to your particular situation. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, contributors, contributing firms, or their respective employers.

Credit.com receives compensation for the financial products and services advertised on this site if our users apply for and sign up for any of them. Compensation is not a factor in the substantive evaluation of any product.

My friend – let’s call him Brad – doesn’t have many good choices. He and his wife – let’s call her Angelina – could hold on to the place and hope the market rebounds. But they need more space, so that’s not ideal. They could sell it at a loss, but they’d lose their entire down payment and still be out of pocket. That obviously doesn’t appeal. They could try to rent it out and rent something bigger, but the math doesn’t quite work for that option, either.

I told Brad about a third option… called strategic default.

A strategic default occurs when someone simply decides to stop paying their mortgage and property taxes, and chooses to let their house fall into foreclosure. The bank that holds the note on the house takes possession of the property and eventually sells it. It also gets to keep the down payment and everything that’s been paid on the mortgage up to that time. Meanwhile, the homeowner gets to live in the house without paying a dime until the foreclosure goes through and the bank takes possession.

[Related: Why the Home Loan Mod Program is Failing]

The average homeowner facing foreclosure hasn’t made a payment in 507 days, which means that by the time they are forced to vacate, they can live rent-free for as long as two years, and maybe longer, according to a recent report. Ideally, this affords them a chance to recoup a sizeable chunk of the money they put down on the house. And though the stain of foreclosure on their credit report will likely prevent them from buying a house for the better part of the next decade, they will have saved up enough to rent a pretty nice place in the interim. They also should be able to save lots of money toward the down payment on a future house.

Sounds like a no-brainer, right? Well, when Brad told Angelina about strategic default, she said it was simply not an option…and she barred Brad from talking to me about real estate ever again.

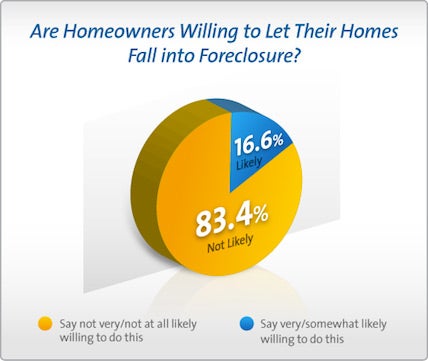

Angelina’s aversion to strategic default is hardly unique. A recent Credit.com-GFK survey indicates that most Americans oppose the idea. We asked participants if they’d do a strategic default if their homes were underwater. We explained that it could mean living for up to two years rent-free, in return for a seven-year stain on their credit reports.

This national RDD Probability Sample telephone poll was conducted for Credit.com by GfK Custom Research North America from January 14-16, 2011. A total of 1,004 interviews were completed, with roughly 531 female adults and 473 male adults. The margin of error is +/- 3 percentage points for the full sample.

The results couldn’t have been clearer. More than 83 percent of respondents say they were either ‘not very’ or ‘not at all’ likely to do a strategic default.

Photo: Linus Bohman, via Flickr.com; Graph: Credit.com

Foreclosed homes in Columbus, OH

I suspect there are two reasons behind our survey results. First, the idea of seven years of bad credit just plain scares people. That’s understandable. But it’s worth noting that while foreclosure restricts a consumer’s access to credit and makes borrowing more expensive, it does not cut people off from credit entirely. And don’t forget: living rent-free for two years means plenty of cash in the bank.

Second, I think the crux of the matter is that people feel that walking away from a mortgage is morally wrong. Recent studies back me up. One study by Professors Luigi Guiso, Paolo Sapienza and Luigi Zingales found that 81 percent of respondents believe it’s immoral to default on a mortgage when you can afford to pay it. The key part of this finding is “when you can afford to pay it.”

That’s an emotional or moral judgment – not, strictly speaking, a rational one.

[Resource: Misconceptions May Keep Homeowners From Getting Low-rate Refi’s]

University of Arizona law professor Brent T. White last year published a paper on the influence of emotion on the decision to strategically default. He reports, “if rationality was the driving force, most strategic defaulters would walk away much sooner than they actually do. Instead, most strategic defaulters don’t walk away until they are more than 50% underwater.”

Professors White and Zingales (of the University of Chicago) have been debating this morality question back and forth.

White argues that a mortgage is a contract like any other and the bank makes provisions for defaults, strategic or otherwise. When a borrower defaults, the bank gets to keep the house, the down payment, and everything that’s been paid on the mortgage up until then. He likens it to breaking a cell phone contract to save hundreds of dollars by switching to a different carrier: “Would it be immoral for you to break your contractual ‘promise’… and elect instead to pay the early termination fee?” White asks. “Of course not.”

But Zingales suggests that if strategic default became commonplace, it would devastate the entire housing market.

He writes: “If the underwater homeowners who currently refuse to default changed their minds and decided to abandon their mortgage commitments, the results could be catastrophic. The more people walk away, the more houses get auctioned off, further depressing real-estate prices. This additional decline would push more homeowners into negative territory, leading to still more defaults. Adding to the deadliness of this cycle would be the fact that as more strategic defaults occurred, the social stigma associated with them would lessen.”

The role of the banks … and an alternative »

Image: Louisa Thomson, via Flickr.com

On one issue, Zingales and White almost agree. White points out that in many cases, debtors who initially resist strategic default are ultimately pushed to do it because their lenders have been unresponsive when it comes to renegotiating the terms of their loan. Zingales, for his part, has proposed that as an alternative to strategic default, an amendment be made to the bankruptcy code that allows banks to reset mortgages to the current market value, and then split any future appreciation in value with the debtor.

These arguments recognize the central role banks played in creating the mortgage mess. Originally, mortgages were designed so that both the debtor and the lender share the loan’s risk and potential reward. It was in both sides’ interests to make sure that properties were realistically appraised and the borrower could afford the monthly payments. That’s supposedly why banks run credit checks on borrowers and inspect properties to assess their value… because they knew that if the borrower ran into trouble, they could end up owning the house.

[Featured products: Monitor your credit reports and scores]

But during the housing bubble, the relationship between banks and lenders changed.

Instead of holding onto mortgages for 30 years, banks sold them within days of closing and packaged them into securities for investors to buy. Now banks no longer had financial incentive to care about the long-term performance of those loans. Instead they simply needed volume to keep the sales and securitization fees rolling in. So they started lending to just about anybody, using sketchy investment vehicles like stated income loans (also called “liar loans”) to get the job done.

In some states, banks have lessened their risk even further through a process called recourse. That’s when a bank can sue defaulters for the difference between what the property sells for at auction, and what is owed on the place. Though banks rarely exercise this right because of the legal costs and the likelihood of bad PR.

People can argue the morality of strategic default until the cows come home, but I suppose the more important issue is how to resolve the issue. 2011 will be a telling year for that question. This year we’ll see a large number of option ARM mortgages reset (these are mortgages that start with a low teaser rate, for five years or so, and then get bumped up to a higher rate). As a result, and many borrowers will see their monthly payments increase.

Will this lead to a new wave of strategic defaults? Will the threat of a wave of defaults encourage banks to renegotiate the terms of these loans, and forgive a portion of the principal? Only time will tell, but I wonder whether you think either party is morally obligated to do one thing or another in these situations. Please tell us what you think in the comments section below.

December 13, 2023

Mortgages

{kind=link}