The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Information on this website may not be current. This website may contain links to other third-party websites. Such links are only for the convenience of the reader, user or browser; we do not recommend or endorse the contents of any third-party sites. Readers of this website should contact their attorney, accountant or credit counselor to obtain advice with respect to their particular situation. No reader, user, or browser of this site should act or not act on the basis of information on this site. Always seek personal legal, financial or credit advice for your relevant jurisdiction. Only your individual attorney or advisor can provide assurances that the information contained herein – and your interpretation of it – is applicable or appropriate to your particular situation. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, contributors, contributing firms, or their respective employers.

Credit.com receives compensation for the financial products and services advertised on this site if our users apply for and sign up for any of them. Compensation is not a factor in the substantive evaluation of any product.

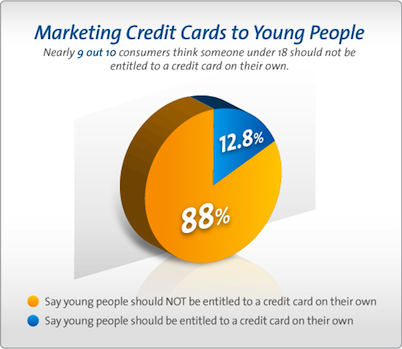

A majority of the public agrees. We asked 1,000 people in a new Credit.com survey whether someone under the age of 18 should be entitled to a credit card on their own. Eighty-eight percent of respondents said no, absolutely not.

Stay tuned for more of our quarterly survey findings. Find out what consumers have to say about employer credit checks, marketing credit cards to teenagers, strategic default, online data privacy and more.

The current law goes even further to say that banks and card issuers cannot grant credit cards to anyone under the age of 21 without sufficient proof of income or a cosigner. I’m not saying that young adults are more likely to rack up debt than their parents. It’s more that I just don’t see the point in introducing them to a financial product that offers them little to no benefits. Sure, you can establish credit history at an exceptionally young age, which helps your credit score in the long run. But let’s be real: how many 17 year-olds even know what a credit score is? According to the JumpStart Coalition, a D.C.-based non-profit focused on improving financial education among students, the financial literacy of high school students has fallen to its lowest level ever, with a score of just 48.3 percent. On the exam most students answered many credit card-related questions incorrectly.

[Related: How the Credit CARD Act of 2009 Affects You?]

On a personal note – I opened my first credit card at age 19, only to abuse it for the next three years. I graduated from college with about $4,000 in debt and that’s WITH having very strict parents who told me only to use it for emergencies. I can just tell you from experience that having the ability to eat your pizza now and pay for it later is all-too irresistible when you’re a teen.

This national RDD Probability Sample telephone poll was conducted for Credit.com by GfK Custom Research North America from January 14-16, 2011. A total of 1,004 interviews were completed, with roughly 531 female adults and 473 male adults. The margin of error is +/- 3 percentage points for the full sample.

Image by kilcolman, via Flickr

August 26, 2020

Student Loans

August 4, 2020

Student Loans

July 31, 2020

Student Loans

{kind=link}

{kind=link}