It can take years to get out of debt, especially with personal debt of hovering around $38,000 for the average America, if you don’t count mortgages, reports CNBC.1 Repairing your credit can involve paying back creditors, declaring bankruptcy or just getting control of bad financial habits. It takes time to get to improve your credit score and get the good credit score you need to qualify for better loans, credit cards and interest rates.

Repairing your credit though isn’t the end of your journey. It’s really just a new beginning. Once your credit is repaired how do you maintain and continue improving your credit score? That’s where standard credit best practices come in.

Continue to Course Correct

Your credit repair process—whether with a credit repair lawyer, a credit repair service or on your own—started you on a path to course correct whatever hurt your credit to begin with. That may have been the result of bad luck and unavoidable life circumstances or bad habits. Whatever it was that got you into a bad credit space to begin with, your first course of action on continuing to improve your credit is to stay on the right course.

If bad habits got you into your previous situation, it’s critical to avoid falling into those habits again. It’s also important to follow some basic credit maintenance and improvement tactics.

Avoid Applying for Too Many New Cards

Once you have a good credit score again, it’s tempting to apply for the many offers for credit card accounts you receive. The cards may come with awesome perks or no interest for a set period of time.

The problem with applying for more than one card is that each application adds a hard inquiry to your credit report. Each inquiry can affect your credit and lower your score about five points, so one won’t hurt you much, but several can lower your score. And that reduction says on your report for about a year.

Granted, you may need a new credit card to help to continue rebuilding your credit. If you do need a new card, find one you’re likely to get approved for and apply only for that one. That way, you can keep hard inquiries to a minimum—preferably a minimum of only one!

On the flip side, you don’t want to close accounts either. A closed account affects your credit history, which is about 15% of your score. It’s actually a good thing for your score to have had accounts for a long time. So, even if you don’t use an account, keep it open. Granted, if you can’t avoid the temptation to use your card, closing it may be better in the long run. But if you can store the card out of reach, it’s better to have an unused card than a closed account.

Control Your Credit Utilization Ratio

The ratio of your credit debt to limit determines your credit utilization ratio. Say you’ve accumulated $1,000 in debt on a card that has a $4,000 limit, our utilization is 25%—1,000 ÷4,000 = 0.25 or 25%.

Credit utilization makes up 30% of your credit score. Keeping your credit utilization under 30% is good but 10% is ideal.

Your utilization shows creditors that you don’t carry a lot of card debt and can use credit responsibly.

A hint: more cards—including keeping the aforementioned accounts open and not closing them—improves your credit utilization if you don’t charge any more than you would without the cards. A higher line of credit lowers your credit utilization rate when you don’t charge more. For example, an old account with a credit line of $1,000 left open, but unused or used very little, in addition to a credit card account with a $4,000 limit with that $1,000 balance, gives you a total credit limit of $5,000. $1,000 divided by $5,000 is a credit utilization of just 20% rather than 25%.

Make Payments on Time and in Full

A simple but effective plan for how to maintain and improve your credit score is making your payments on time. Late payments hurt your credit the most. They increase your outstanding balance and lead to fines and interest charges. And credit card issuers report your late payments to the major credit bureaus. Payment history makes up 35% of your credit score.

If you find yourself unable to make your payments on time, try to adjust your spending. Otherwise, you may find yourself going down the same rabbit hole you just got yourself out of.

Diversify Your Credit Portfolio

Is the only credit account you have plastic, known as or revolving credit? If so, you may be limiting your credit score. Creditors want to know you can handle not only revolving accounts but also installment accounts, such as a car loan that has a fixed monthly payment over the term of the loan.

By no means should you get a car or house just to add variety to your credit history, but don’t be afraid to make the leap to the other side of credit if the need is there and the time is right. Say, for instance, you still have more credit card debt that you like. You could consider a personal loan to pay down the card. Personal loans often have lower interest rates than some credit cards, so you’d benefit both by lowering your credit card payments and interest as well as improving your credit accounts mix, which makes up 10% of your credit score.

Another but less-common type of credit is open credit that falls between revolving and installment. Like revolving credit, you rack up a different balance each month, but like installment, you have to pay it in full by the due date. The bill for your cell phone is one example, though you can also find credit cards that work this way.

Continue to Monitor Your Credit Report and Score

During your credit repair process, you likely worked on your credit report a lot—ensuring it was accurate and maybe even disputing incorrect items. But even now that your credit is repaired, don’t take your eyes of your report. Get your free annual reports from the credit reporting bureaus—Equifax, Experian, and TransUnion—through AnnualCreditReport.com.

Think this step is unnecessary? Well, 37% of the 329,000 complaints consumers made to the Consumer Financial Protection Bureau (CFPB) from October 2017 to September 2018 were about credit or consumer reporting.2 And 93% of the companies responded to issues submitted to them by the CFPB.2

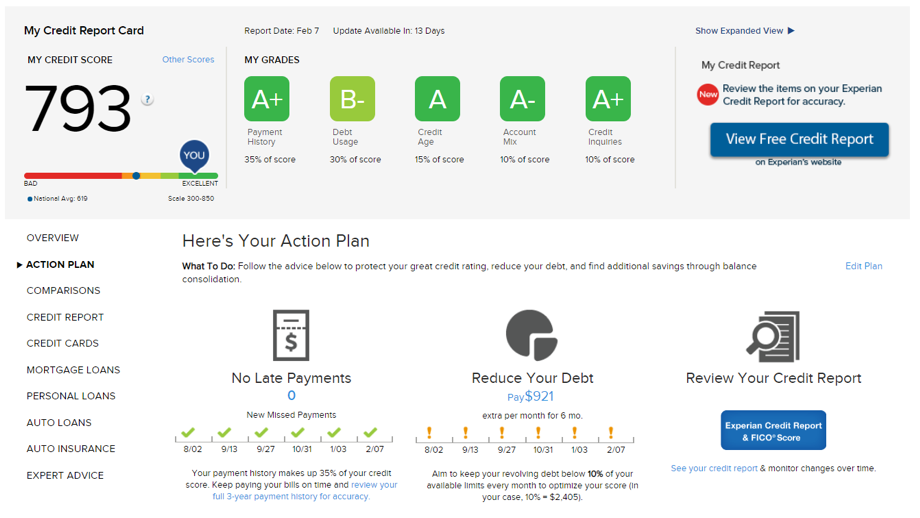

Outside of your annual free credit reports, consider monitoring your credit score. There are a variety of ways you can monitor our score—many for free—including right here at Credit.com. When you get your Experian VantageScore credit score at Credit.com, you get a free credit report card too. That report card show you how you’re doing in the five areas that make up your score—payment history, credit utilization, credit age, account mix and credit inquiries. And your score and report card are updated every two weeks. If you see a sudden change, it can be an early warning system that something is up with your credit—something like identity theft.

Protect Your Information

An easy way for your credit score to plummet again is for a criminal to steal your personal information, whether it’s credit card numbers or your full identity. In fact, identity theft that involves opening new accounts is more common than theft of existing credit card numbers, according to the Insurance Information Institute.3 But data breaches in 2017 still exposed 14.2 million credit card numbers, which was 88% more than the previous year according to Experian.4

There are simple steps you can take toward identity-theft protection. If you worry you may be at risk, you can place an initial fraud alert on your credit report. If you know you’ve been a victim, you can also place an extended fraud alert on your reports. Learn more in “How Is a Fraud Alert Different from a Credit Freeze or Lock?”

You can strengthen your passwords and:

- Never use the same one for multiple sites

- Choose two-factor authentication for higher security

- Never access financial accounts on public Wi-Fi

- Be careful with the personal information you share on social media

A Quick Review

Here’s a summary of things you can do to maintain and improve your credit score now that you’ve repaired your credit.

Do’s

- Do keep old credit cards active.

- Do keep your credit utilization below 30%.

- Do make your monthly payments on time.

- Do maintain different types of credit, not just credit cards.

- Do check your credit report annually to make sure it’s accurate.

- Do protect yourself from identity theft.

- Do get your free credit score and report card from Credit.com.

Don’ts

- Don’t accept every credit card offer you get.

- Don’t max out your credit cards.

- Don’t continually carry a large credit card balance over to the next month.

- Don’t overlook errors on your credit report.

- Don’t underestimate the likelihood of identity theft.

Congratulations on having repaired your credit and going from poor credit to good credit. Best of luck as you maintain and continue to improve your score.

1 https://www.cnbc.com/2018/08/20/how-much-debt-americans-have-at-every-age.html

2 https://files.consumerfinance.gov/f/documents/cfpb_semi-annual-report-to-congress_fall-2018.pdf

3 https://www.iii.org/fact-statistic/facts-statistics-identity-theft-and-cybercrime

4 https://www.experian.com/blogs/ask-experian/identity-theft-statistics/

You Might Also Like

Find out if your rent and utility payments are reported on your c... Read More

April 11, 2023

Uncategorized

Becoming an authorized user is a common tip for individuals tryin... Read More

September 13, 2021

Uncategorized

Long-term unemployment can really hurt—and not just financially... Read More

August 4, 2021

Uncategorized