It's Financial Literacy Month: Here's What Your Credit Score Wants You to Know

Learn how to improve your credit score with essential tips on payment history, credit utilization, and more this Financial Literacy Month.

Published November 27, 2023

Many or all of the products featured here are from our partners who compensate us. This may influence which products we write about and where and how the product appears on a page. However, this does not influence our evaluations.

Generally, you should aim to spend under 30% of your gross monthly income on rent.

Table of Contents

If you’re looking for a new place to live, odds are you’ve browsed hundreds of rental listings and apartment complexes in your area. While searching for a rental can be overwhelming, there are steps you can take to narrow down your search. The first step—setting your budget. Read on to discover how much to spend on rent.

While there isn’t a clear-cut answer for how much money to spend on rent, financial experts have created multiple guidelines to help you create your monthly budget. Here are a few options to consider:

The most popular method for determining how much of your income to spend on rent is the 30% rule. According to this rule, you should allocate no more than 30% of your monthly gross income to your rent. If you’re using only 30% of your income on rent, you have the other 70% to allocate to your other living expenses, debt repayment and savings.

To calculate your rent budget based on this rule, take your yearly income and multiply it by 0.3, then divide by 12. For example, if your yearly salary is $60,000, you should aim to spend $1,500 a month on rent.

Reference the chart below for an overview of the 30% rule at different income levels.

| Gross Annual Salary |

Estimated Maximum Monthly Rent |

|||

|---|---|---|---|---|

| $25,000 |

$625 per month |

|||

| $50,000 |

$1,250 per month |

|||

| $75,000 |

$1,875 per month |

|||

| $100,000 |

$2,500 per month |

|||

| $125,000 |

$3,125 per month |

|||

| $150,000 |

$3,750 per month |

Keep in mind that this method might not be feasible for everyone to follow, especially in places like New York City, San Francisco, and Boston where rent is extremely high. For example, the average monthly rent in New York City is $5,600, meaning you would need an annual salary of at least $224,000 to follow the 30% rule.

If you live in a high-cost city and find this rule unrealistic for your scenario, you may want to consider following a different budgeting technique.

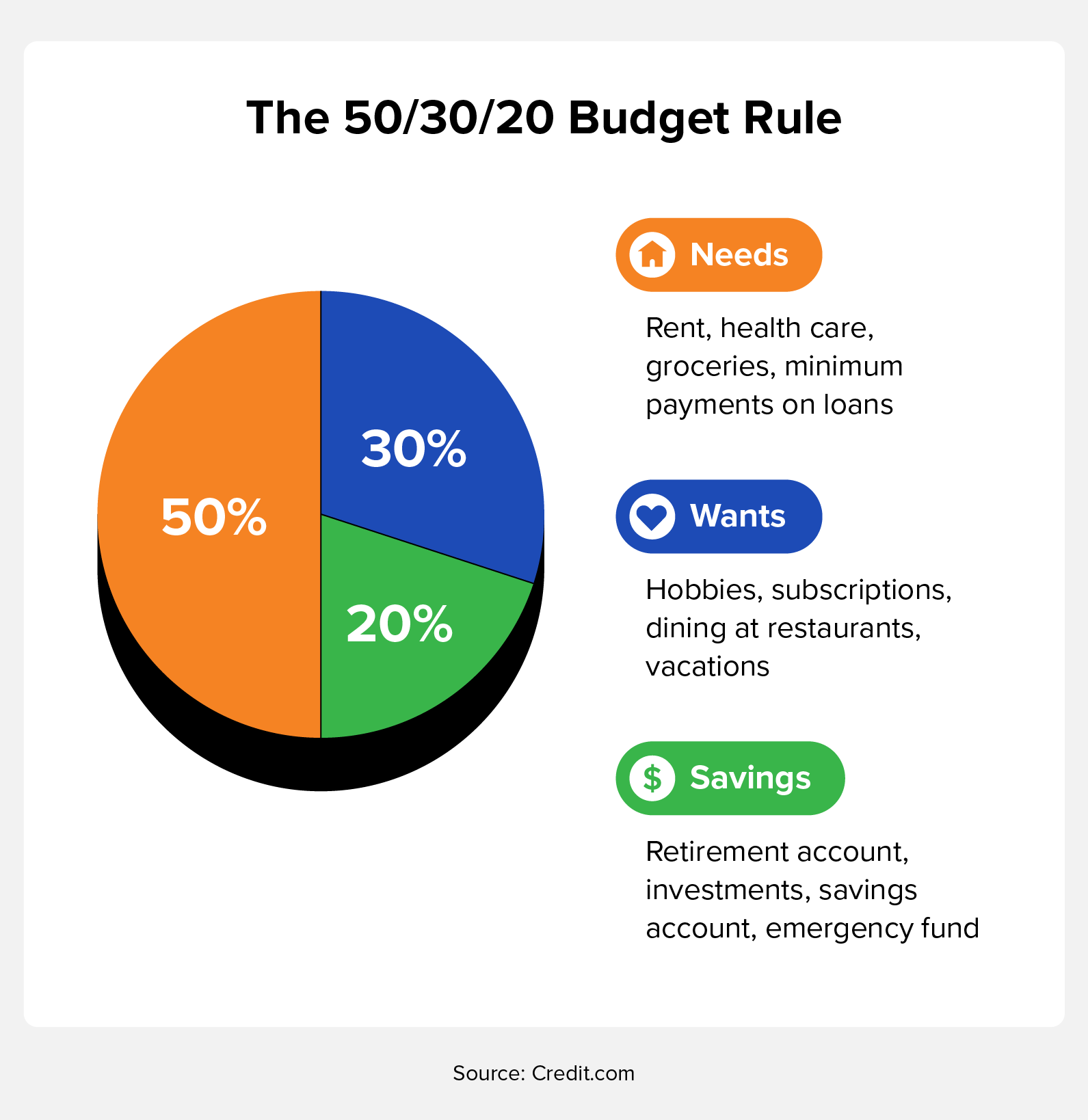

The 50/30/20 rule is a technique that divides your after-tax income into three categories—50% toward needs, 30% toward wants and 20% toward savings. This method isn’t as straightforward since rent is a part of the broader “need” category.

Let’s walk through a step-by-step example to determine your rent budget according to the 50/30/20 rule:

If, after using this template, you find that your rent budget is lower than you’d prefer, you can lower your other “needs” expenses to allot more money toward your rent budget. For example, you could get a more modest vehicle, shop at a more affordable grocery store, or take steps to lower your utility bill.

Similarly to the 50/30/20 rule, the 70/20/10 rule divides your post-tax income into three different categories. With this technique, 70% goes to spending, 20% to saving and investing and 10% to debt repayment and donations. With this rule, rent is a part of the “monthly spending” category.

Here’s how to calculate your monthly rent budget according to the 70/20/10 rule:

With this rule, you may have more wiggle room to increase your rent budget by cutting down spending on your wants. For example, you could reduce the frequency of eating out or spend less money on clothes to grow your rent budget.

Remember that there isn’t a one-size-fits-all approach to how much to spend on rent. When deciding between different rental options, consider how the following factors may add additional costs or offer savings opportunities:

Due to rising rent costs across the U.S., staying within your rental budget can be a challenging task. Consider the following tips to save money on rent:

Budgeting techniques like the 30% rule, the 50/30/20 rule, or the 70/20/10 rule can provide you with a guideline of how much of your income to spend on rent. Additionally, looking for ways to save on rent can help you reach your other financial goals.

Now that you’ve determined your rent budget, credit score is another factor to consider when apartment searching. Landlords and property managers will likely perform a credit check to help determine your ability to pay rent. Generally, your credit score should be in the “good” range (670 or above) to improve the odds of your applications getting approved. While you can get an apartment with bad credit, you might have to jump through additional hoops.

Unsure what your credit score is? Check your credit score for free today to make sure you’re ready to sign a lease.

Learn how to improve your credit score with essential tips on payment history, credit utilization, and more this Financial Literacy Month.

Learn how to use your tax refund to improve your credit score with these strategic financial tips. Boost your financial health and achieve your credit goals.

Take control of your financial health and strengthen your money relationship with practical tips to improve your credit score and set financial goals today.